Innovative Tyres and Tubes Limited (ITTL) is part of the reputed Innovative Group, one of the leading manufacturers and exporters of Bias Tyres in India, with experience of 20 years in manufacturing field. ITTL offers a wide range of products in the Truck / Bus, Agricultural & OTR and Motorcycle / 3-wheeler segments. The company has two manufacturing units- Innovative tyre plant and innovative tube plant- which are located very close to each other. Innovative Group is a diversified business house catering to the automotive market. The group comprises of three companies- Innovative Tyres and Tubes Limited, Future Tyres Pvt. Ltd.and Gaia Batteries Pvt.Ltd.- spread over 4 manufacturing units located near to each other. The group is set to welcome two entrants- Green Batteries Private Limited and Green Tyres Private Limited, both part of a joint venture with Greenfield Inc., part of Nepal-based Vishal Group to cater to the dynamic Nepal market for tyres as well as batteries. Based in Kathmandu, Vishal Group is a business house with interests in a plethora of market sectors-FMCG, education, insurance, hospitality and cement and steel, to name a few.

BUSINESS

Incorporated in the year 1995, we are a tyre and tube manufacturing Company, manufacturing & marketing our products under flagship brand ―Innovative. We started our journey with the acquisition of a greenfield project situated at Halol in auction from Gujarat State FinancialCorporation and State Bank of Bikaner & Jaipur vide agreement dated December 15, 1995. There after we revamped the closed company to our tube manufacturing facility at this property and started manufacturing of tubes in the year 1996. Within a short time after our inception, we were able to successfully get our facility approved by CEAT Limited for carrying out job work activities for them.

As a result of strong business relationship with CEAT Limited, taking the relationship to the nextlevel we set up a greenfield tyre project as a major outsourcing unit in 2003 in a close vicinity of the existing first tube plant in Halol only. While our tube manufacturing facility is spread over 11,200 sq.mtrs, our tyre manufacturing facility occupies an area of approximately 27,833 sq. mtrs. We have an installed production capacity of 12,000 MT of tubes and tyres. We also have a factory outlet for display of our products at Vadodara. The product wise quantity sold during FY 2016-17 is :- Two Wheeler: 3718 MT, Light Commercial: 2343 MT, Truck Segment: 3013 MT and Agriculture & ORT: 669MT.* *includes quantity manufactured on jobwork basis from our group company Future Tyres PrivateLimited. Company has planned a capex of Rs. 21 cr (Rs. 17 cr from IPO and Rs. 4 cr. from bank) on existing land for manufacturing of OTR, Radial Agricultural Tyres and Tubes. Company plans to start commercial operation from this capex by June 2018. Company intends to expand it’s manufacturing capacity by 8000 MT p.a.

Company has done some interesting work in the past 3-4 years. In 2015 company became the first Indian tyre manufacturer to achieve the PNS Quality certification from DOT, Philippines. In FY17 sales to Philippines were Rs. 21 cr. (15.99% of total sales). In 2016 company entered into an agreement with Gabriel India Ltd. and became the sole manufacturer for their tyres. In 2014 company started manufacturing OTR and tubeless tyres.

MANAGEMENT

Company is promoted by Mukesh Desai and Pradeep Kothari. While Mukesh Desaihas been associated with the Company since its inception, Promoter Pradeep Kothari became a par ot of Company in 2014.Mr. Pradeep Kothari and his family holds 20.51% shares in the company. He invested in the company in 2014 and was then appointed the additional director. He is the driving force of the company in past 3-4 years and is guiding the company in it’s latest expansion and export sales. Mr. Mukesh Desai is responsible for overall management and Mr. Nitinbhai Mankad looks after government work, legal work and new business development.

FINANCIALS & VALUATIONS

After the IPO the outstanding equity share capital of the company is Rs. 17.99 cr (17991561 shares of Rs. 10 each), Net Profit for F.Y. 2017 is Rs. 4.08 cr. Diluted EPS for FY17 is Rs. 2.26. From FY14 to FY17 company has not shown any growth in sales but operating profits has grown from Rs. 9 cr. to Rs. 14.02 cr at 14.99% cagr. With the coming capex management in it’s prospectus has guided for Rs. 200 cr. sales in FY19. At current price of Rs. 50.30 the MCAP of company is Rs. 90 cr.

Company has shown good sales growth in the domestic market in recent years.

With little sales growth in past three years and low ROE of 11% in FY17 valuations are in line with the peers. Shift from bias-ply to radial tyres with the upcoming expansion and management guidance of sales growth will have to be watched carefully for future earnings growth.

IPO

Company raised Rs. 28.33 cr from the market through issue of 6297000 shares at Rs. 45 each in September 2017. Utilisation of Proceeds:-

Expansion Rs. 17 cr, WC requirement Rs. 4 cr., General Corporate Purpose Rs. 4.83 cr and IPO expenses Rs. 2.50 cr.

Risk

Shift in Indian tyre market from bias-ply tyres to radial tyres pose a threat to company’s performance as company manufactures bias-ply tyres only. Though the company is making new capex in radial tyres.

Promoter Holding is low at 24.32%.

Job Works constitutes 24.62% of total sales, it may not be able to pass on the increase in prices of raw material.

Other Points

Out of the total revenue for the FY 2016-17, revenue from CEAT Limited contributes 11.37%.

Company has entered into various transactions with Promoters, Promoter Group,Directors and their Relatives and Group Company. Further, purchases from Group company/Promoter Group Raman Enterprises and Future Tyres Private Limited was 8% and 5%of our total raw material purchases for the year ended March 31, 2017, 17% and 2% of our totalraw material purchases for the year ended March 31, 2016 and 28% and 3% of total purchases for the year ended March 31, 2015.

We also outsource manufacturing of two/threewheeler tyres to our group company Future Tyres Private Limited and job work charges paid tothem on such account was Rs. 177.64 Lakhs, Rs. 329.17 Lakhs and Rs. 102.91 Lakhs for the yearended 2017, 2016 and 2015 respectively.

Export order book as on date of prospectus is of 3359.49 MT to be completed by June 2018.

The question in your mind: What do I get by paying up 1600 crores?

Well, what you get is a business generating 70 crores of free cash flow every year, needing no capital investment to grow, operates at 25% EBIT margins and generating a return on capital greater than 90% even when it is an operating at a capacity utilization of only 50%.

Before you start thinking about the valuation, let me add a mall worth Rs 1100 crores as an additional incentive.

That’s not all. The company will have cash of 130 crores by end of FY 18.

Feel the dopamine rush yet?

Well,let’s get down to business.

The company we are talking about is Grauer and Weil Limited (established 1957), dealing in surface treatment chemicals, industrial paints, engineering services and lubricants. Led by the father son duo of Umesh and Nirajkumar More, this family run company has done wonders over the last couple of decades.

Let us talk about each of the divisions:

Chemicals-

Grauer is the market leader in the segment of surface treatment chemicals, intermediates and specialty electroplating chemicals and has manufacturing facilities in Dadra, Vapi & Jammu. The operations of the company are fully backward integrated making it very difficult for any new players to enter this segment. (Strong entry barriers, this is evidenced by the fact that there are only 3 players in the country in this business making it an effective oligopoly).

The revenues from this business are 300 crores (FY17), EBIT is 77 crores ( margins exceeding 25% ) and capital employed only 85 crores. (ROCE of 90%). The most important point amidst all these figures is that this is at a capacity utilization of only 45-50%,thus company could effectively double its revenues without incremental capital investment.

The market size in India is 750 crores (giving Grauer a 40% market share), which is growing at 8-10% (in line with nominal GDP). As for breakup between price and volume growth, price hikes are roughly 5-6% per annum. The domestic market is largely saturated. With regards to exports, this being a service oriented industry, the company would need to establish service centres in every country it wishes to enter.

Aviation business (read attached Business India article for further details) will be small in terms of revenues, but a high margin business since these are specialised components.

Competitors include Atotech and Artek Ltd (this company is spearheaded by Goenka family who were erstwhile partners of Grauer and Weil Ltd). Grauer is one of only four companies in the world which have the capability to provide such service (as claimed by the management). This is thus one of the few businesses possessing high asset turnover and high margins.

The total investments in plant and machinery are only Rs 42 crores, on which company generates Rs 300 crores of revenue.

Paints-

In 2008, promoters merged Bombay Paints Limited with Grauer, which is now a 65 crore business. The company has shifted focus from conventional industrial paints to specialised paints which cater to pipeline coating, underground/underwater pipeline coatings, and so on. There is significant revenue growth potential in this segment and long term operating margins should be between 10-15% (as guided by the management).

The company has shifted operations from Chembur to Dadra (Capex of Rs 8-10 crores).

Capacity at Dadra plant is close to 8700 KL per annum and company plans to operate at 50% capacity utilisation in FY18.This business has now broken even, and management is confident of reaching 200 crores of revenue in the next 3 years. It is the first chemical and paints to receive certification from Rolls Royce and is in process of validation for Boeing for supply of specialized coatings. Rolls Royce has also approved Grow Space Aqueous cleaner.

This business has underperformed so far, behaving more as a capital guzzler as capital employed is Rs 90 crores and operating profits in FY 17 was only Rs 3 crores.

Engineering-

The engineering division offers turnkey solutions for effluent treatment. GWIL has a plant of Alandi, near of Pune that manufactures all types of equipment’s used in surface finishing and allied industries.

Revenue in FY 17 was 32 crores and operating profits were 3 crores. This is an offshoot of the chemicals business and is lumpy in nature. Aviation will be a focus area where significant growth is possible.

This business though not very big, has the advantage of being extremely capital efficient as capital employed is only 9 crores.

Lubricants-

Grauer has ventured into manufacturing specialized lubricants and oils at two plants – one in Vapi and Baroti (Himachal Pradesh) producing industrial lubricants such as rust preventives, cutting oils, hydraulic oils, heart treatment oils etc.

The current size of the business is only 10 crores, operating profits of 2 crores and capital employed of 3.5 crores. The management expects to see good growth going forward.

Real Estate-

The company owns and operates a mall going by the name of Growel’s 101 in Kandivali, Mumbai. The mall has 4,30,000 square feet( 10 acres) of retail development with 90% occupancy. Revenues this year should be in the range of 32 – 35 crores (almost entirely cash profits since unrecovered common area maintainence is only 0.5 crores-As per AS 17 disclosure, operating profits are 13-14 crores due to depreciation on mall building).

Personal visits to the mall have revealed a mall that has been built very well( though utilisation of space could have been done much better in terms of the structure of the mall)

Anchor tenats include PVR(a cinema hall is a must for a successful mall), Croma and central. Others include Mcdonalds and starbucks.

Average rental in mall is Rs 87 per sq ft (exclusive of CAM and property taxes). This includes both fixed rentals and revenue sharing contracts with most lessees.

Now coming to an interesting development- Grauer has utilised FSI of 1.16 as against the currently permitted 1.33 (ex TDR) and 1.85 (Including TDR). This is now expected to go up to 3.5-4 with the announcement of new DC rules, thereby creating an opportunity to further develop 10 lakh square feet. Yes, you read that correct.

Management is cognizant of these expected changes, and has prepared complete business plan for multi use development and has been in discussion with various developers and PE players.

They are most likely planning to develop a hotel or commercial complex where the JV partner would bring in substantial portion of cash investment required and Grauer would contribute land as equity component.

In the nearby area, a little bit of scuttle has revealed that Kalpataru has launched a project with a commanding price of 13,000-15,000 per square foot.

This means that post development, the entire developed complex would sit at 14,00,000 square feet. Do calculate market value of this at 13000 per sq ft. I leave you to draw your own conclusions regarding this

Is that all you might ask?

Well, one final thing. The company has a 99 year lease on 2 acres of prime Chembur land which currently houses only the R & D centre. This can be developed at the appropriate time ( Just as an indicator, current market value would be around 200 crores )

Valuation ( purely my estimates, subject to error)

Chemicals-1500 crores (Great business with low growth (reminds me of See’s candies).

Could be valued at a PE of 25x, considering extraordinary ROCE and sustainable earnings power)

Engineering-50 crores (Considering minimal capital requirements of the business, should trade at a high multiple of earnings. The business should enjoy robust growth over the next few years and hence would probably trade at a high multiple)

Paints This is the business where maximum capital has been deployed and is as yet unproven. Should be valued at slight premium to book value 120 crores

Lubricants Small business, has a large headway of growth in the future,low capital requirements 30 crores

Real Estate Currently rental yields are low and mall is slated to generate about 32-35 crores per annum. The annual growth will be in the range of 7-8%,at cost of capital of 13-14% for this business, valuation should be 32/(14-7)% 450 crores

Cash By FY18 end 130 crores

Total 2280 crores

Please note that this does not take into account a single rupee of upside from the new DC rules, which as discussed above will be substantial.

The promoters come across as conservative capital allocators who are looking at steadily growing the company in the right manner. They have consciously repaid most of the outstanding debt in the last few years and have avoided any value destructive acquisitions. They remain focused on value creation instead of empire building (a favourite for most Indian promoters).

Risk Factors:

Key man risk: As with a lot of promoter run companies, even Grauer faces a key man risk in the event of any misfortune befalling the More family.

Product obsolescence: I will be the first person to admit that my understanding of the business technicals is fuzzy at best and hence will leave you to take a call on this

This is my understanding of the business, could definitely be wrong. In that case, I would request all the distinguished investors to correct me. Would definitely love someone to play devil’s advocate and point out all the apparent flaws in this thesis

Disclosure-Invested

since the NHAI is going digital…

they are slowly handing out NHAI digital tags… which will be stuck on the window shields of the cars. so the amounts will be auto debited…also ppl are slowly travelling more and more by car as the india infra/growth story continues.

i belive in future …the toll collection will be much higher on the books actually shown…less juggling of money (not showing actual revenue which they collected … at the moment they avoid much of it )

so wondering, which companies of toll tax collection will profit from them ? any idea

Anjani Portland is a small cement manufacturer with presence in Andhra Pradesh. It is closely linked to the cement cycle, as is evident from its financials. However, the firm has been able to pay down its debt significantly- from 242 cr in FY 11 to 80 cr now. This makes it far better placed to weather a downturn. For instance, an increase in the price of coal as well as increases in freight charges ate into operating margins in Q2FY18. However, the NPM did not decline as drastically as in FY12 and FY13, since interest costs are far lower now. Like most cement cos in the south, the firm operates at ~70% capacity. EBITDA margins have been at their lowest for the last 4 quarters yet Anjani is valued at just 7.8x EV/EBITDA, which is at a significant discount to many of its peers who have more leverage.

I see this as a mispriced bet. The replacement cost of a 1 MT cement plant is estimated to be USD 135-140 per MT. With 1.15 MT capacity and given that Anjani’s capex still has 80% of its life remaining, this would put its replacement cost at ~ INR 800 cr + another 80 cr for its captive power plant = a total of INR 880 cr. It currently trades at a market cap of INR 600 cr, which provides a 30% margin of safety.

Risks:

Freight costs are up 150% this quarter and the explanantion provided by the management is that the have moved from ex works pricing to FOB. However, other cement cos have not seen such a sharp rise in freight costs

Their presence at a single location may restrict their growth in the future.

This is an undiscovered gem. Let me start with a brief synopsis:

About the industry:

The seed industry lies at the very core of the agro industry and it is becoming an increasing lucrative proposition.

Conventional type of agriculture was where the mother seed was kept by the farmer for the next season and he cultivated the seeds and used it. This practice has been followed from the time agriculture was invented. But with the advent of technology in all fields of life, agriculture too will be impacted. Computers have revolutionized medical research now is the time to change the seed growing methods. Hybrids and GM tech will change the way the seed industry works. Research in seeds will change the way agriculture will be done by 2030.

Using conventional techniques the farmers used to face frequent crop failures due to seeds turning bad. This situation should change with the technological advances in this area.

Farmers were suspicious of hybrid seeds and were misinformed about its benefits. Hence hybrid seeds business did not grow as expected. Now the scenario has changed considerably. As estimated by CIMB in its report, hybrid seed industry is worth Rs.12,000 crores in FY 18. If penetration in rice and other products increase to 60 % by 2030, then the organized seed industry in India would be Rs.1,00,000 crores. Just 8-10 companies as of now are worth mentioning: Kaveri, JK Agri, Monsanto, Rasi seeds, Nuziveedu, Nath bio genes, Ajit seeds and some regional players. If the theme is played well by these companies, they can have a blockbuster 20 year growth run as food will get scare with time.

• Land productivity in the last 2 decades has gone up by 30-35 % (very less), whereas tech has changed the face of many industries during the same period. Smart phone has 100 times more computational power than a 286 desktop of 1999 make. Strides have taken place in surgeries, designing capabilities, etc. but the neglected child was SEEDS. Hybrid seeds were not easily accepted due to ignorance and illiteracy of farmers around the world. But due to information explosion and proactive attitude of Governments, farmers are adapting to new techniques of farming.

• Feeding a huge population in the next decade has become a headache for the Governments. China has leased millions of acres of land in South America for securing food for its population.

• Consolidation is happening in the seed industry worldwide: Earlier 6-7 major companies were present in seed industry. In last 3 years, DOW has merged with DUPONT, CHEM CHINA (Government co.) has purchased SYGENTA, BAYER has purchased MONSANTO. Now these 3 conglomerates are controlling 70% of the world seed market.

• Technology has to touch the seed industry to increase the per acre productivity. Since the landmass is finite and population is growing, to feed more mouths there is no substitute other than by increasing productivity.

• Research to market journey of one hybrid seed is a 5-6 year period. So if one starts working in 2012 on hybrids, it will be 20 -30 years before the hybrid say rice will give double the productivity. Thus a company having good quality germ plasm of different hybrids can have fabulous valuations going forward (Germ plasm is the IPR here).

• Agriculture is a state prerogative. To acquire seed companies in different countries, permissions are needed. Hence home grown quality seed companies will have fabulous valuations.

• Agriculture will be the biggest job generator in the period 2017-2027. By implementing correct policies, India has the potential to become the FOOD HOUSE OF THE WORLD.

• Thus agriculture can be the next big theme for the next 10 yrs. Fertilizer companies, pesticide companies, farm equipment companies and seed companies will thrive.

• Due to MNEREGA, farm labor has become very costly. Hence ancillary farm equipment companies will have a field day. Manufacturers of farm tillers, automatic pesticide sprayers and combine harvesters will have quantum growth.

• Pesticide companies having research base in India will do very well. As a seed scientist has said ’ You need local police to deal with local goons. CIA of America cannot deal with them.’ - Thus for local pests, you need local pesticide companies doing research and sell effective products. We can expect manifold returns from them in the next 5-10 years.

• Local seed companies having large research base, huge germ plasm, good marketing team can give huge returns in the next 10-15 years for companies like JK AGRI GENETICS, KAVERI SEEDS, NATH BIOGENES, NUZIVEEDU SEEDS, RASI SEEDS (if the last 2 list on the markets).

About the company:

Part of the Lakshmipath Singhania Group. They are the second richest family in Kolkata. They have companies with a combined turnover of close to $ 4 billion. These include JK Tyres, JK Paper, JK Sugar, JK Agri Genetics, Fenner India and JK Lakshmi Cement. JK group derives 95 percent of revenues from Agro based industries.

JK agri genetics (JK seeds) has a wide range of products both Field crops and Vegetables - 3 cotton hybrids, 3 Jowar hybrids, 6 tomato hybrids, and 16 hybrids in all types of gourds.

Why JK Agri is so lucrative:

Huge R&D focus. Spends around 15 crores every year on R&D. Efforts are now coming to bear fruit (or rather vegetables)

Focus is on vegetable seeds segment which has 60% gross margins and where sales peak in Q3 and Q4 the leanest period.

They are focusing big time on Africa where cotton cropping season starts from November. There is no price cap on cotton seeds in Africa unlike in India where it is capped at Rs. 800 per packet. Exports to Africa have already started.

Last year they achieved break even in H2. This year they should be in profits. Operating leverage play. Very low capital base magnifies the EPS figures.

They are paying taxes while Kaveri and Nath Bio are not paying.

Peer set valuation is very lucrative especially if you factor in that they are paying taxes due to which they are losing on EPS front.

JK Pass Pass has been very well accepted in the markets. Since it takes 3 years for a good seed variant to be commercially successful Q1 2018 should be very good for JK Pass Pass as market reports has given it a big thumbs

.

If we go by the trade data of Rasi 659 which is a BT cotton variety:

2015: 8 lakh packets

2016: 15 lakh packets

2017: 45 lakh packets

Jk AGRI’s PASS PASS :

2016: 2 lakh packets

2017: 5-6 lakh packets

2018: 10-15 lakh packets (?)

7. The reputation of many firms has been tarnished for selling Spurious BT cotton seeds

These include Kaveri , Monsanto, Ankur, Nuziveedu and Raasi.

Risks:

The vagaries of the nature:

Poor monsoons and unsupportive commodity prices are the bane of Indian agricultural sector and will continue to be so for the foreseeable future.

Regulatory risks:

This sector is susceptible to regulatory risks. Regulatory changes from the Central and State Governments in respect of prices, distribution, royalties, taxation etc. have a high impact on the sector.

Storage infrastructure:

Since seed is a perishable item, it is subjected to death depending upon its genetic potentiality to remain viable and storage conditions. Storage for longer period shows negative effect on productivity.

Climate pest and disease related problems:

Seed production is a seasonal activity. Variations in temperature, heavy or low rainfall leads to huge losses through crop failure. Flowering in most of the vegetables is highly temperature sensitive. Generally seed production is done over larger area with same variety to avoid contamination, but it is favorable for outbreak of pest and diseases epidemics.

Very low float. Just 36 lakh shares and 90% already cornered.

Tried searching VP forum about Man Infra but suprisingly no thread found, so creating a new one.

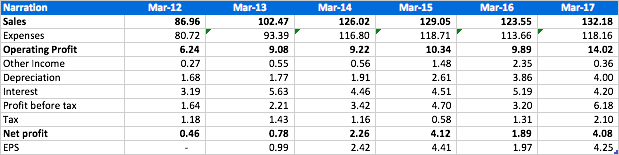

Man Infraconstruction Limited (MIL) is a construction company engaged in the business of civil construction. The Company provides construction services for port infrastructure, such as land reclamation, soil consolidation, and operational services; residential constructions, such as high rise building, townships and luxury villas; commercial and institutional constructions, such as information technology parks, office complexes, shopping malls, schools and hotels; industrial constructions, such as factories, cold storages, heavy engineering and warehouse facilities, and road constructions, such as earthwork and paving, electrification, landscaping, upgradation and drainage. Its residential projects include Blue Ridge, SRA Township, Lifescapes Amber, Signia Sky, Mundra Township and Neelkanth Greens. Its infrastructure projects include Gateway Terminal and Vallarpadam ICTT. Its commercial and industrial projects include Kohinoor Education Complex, Sai Complex and Viraj Profiles Ltd.

Bright future on the back of a strong order book: As on 30th June, 2017 the company’s EPC order book stands at Rs. 7,096mn majority of it contributed from the port infrastructure sector followed by the residential sector and commercial and industrial sector constituting a very negligible portion. The government recently has received the development rights from the urban development department of the government of Maharashtra for 14 buildings in MHADA Layout in Ghatkopar East and 2 buildings in Vikhroli East. In April, 2017 the company also launched their first phase of land redovolopment projects in Ghatkopar East having an estimated value of Rs. 1250mn. Man Projects Limited, a subsidiary of Man Infraconstruction Limited received a prestigious order worth Rs. 7516.9mn from Bharat Mumbai Container Terminals Private Limited for development of the fourth container terminal at Jawaharlal Nehru Port, Mumbai. The project is expected to be completed and executed in FY18.

Asset Light Real Estate Operations: As against the general real estate model of purchasing land with upfront cash payments, Man Infra has built a 50 lakh sq. ft. project pipeline in Mumbai by partnering with existing land owners / redevelopment projects. We think this is the best strategy in Mumbai real estate model where the Land Cost forms a significantly higher proportion of the total cost of project.

Debt Free Cash Surplus Real Estate Company: Man Infra is one of the few companies in the sector with zero debt at standalone level.

Strong Cliental: The company has a strong cliental in both their major business segment i.e Port Infrastructure and Civil Infrastructure. To name a few in the port infrastructure segment the company has clients such DP World, Port Pipavav, Century Ply, MAERSK etc. While in the civil infrastructure segment the company has clients such as Tata Housing, Godrej, DB Realty, Adani, Goddrey Phillip, Bharti Airtel etc. The company also has a history of repeat orders from these marquee clients.

Strong Execution Capabilities: In total the company has executed onshore port infrastructure work for 7 ports in India and completed a total of 3 residential real estate projects. A total of 7.5mn sq. ft of residential projects area are ongoing/upcoming in Mumbai/MMR. The company is also expected to start recognizing revenue for 2 of it’s ongoing real estate projects in FY18.

Robust Project Pipeline: Based on its existing projects, Man Infra along with its partners / JVs have a pipeline of almost 50 lakhs sq. ft. of projects to be executed over next 5-7 years. This provides tremendous visibility of sales and profits for 5-7 years. All its projects are in residential space as follows:

Highlights on Main projects:

a) Mulund Project: ‘Atmosphere’, a real estate project in Mulund, is being developed in joint venture with Wadhwa and Chandak Realtors, with an approximate saleable area of 1.8 million sq. ft. Within a few days of the launch of the project, 40% of phase I was sold indicating strong demand. For this project, 100% contracting work is awarded to Man Infra where it will also earn a contracting (EPC) margin.

b) MHADA Development Project at Ghatkopar, Mumbai: Man Infra has already signed MoU for redeveloping 12 MHADA colony buildings. As a part of the deal, Man has to provide residential accommodation to existing tenants of MHADA and in return it will be able to construct and sell 4.65 lakh sq. ft of residential apartments. This project will be a very rewarding project for Man Infra and should be completed in next 3-4 years.

c) Dahisar Project: Through Man Vastucon LLP (where Man holds 99.9%), Man Infra has obtained development rights to develop 59700 sq. meters plot which will convert into approx 26.4 lakh sq. feet of saleable area at Dahisar. Man Vastucon LLP will undertake the development of the property. The other JV partner will be compensated by sharing 35% of gross sales realization as land cost. This project is in continuation to Man’s asset light policy, where in the company will save huge upfront investment cost and minimize the investment risk.

d) Multiple Other Projects: There are multiple individual building projects like Aaradhya Residency, Aaradhya Saphalya, Aaradhya Nalanda, Aaradhya Signature in and around Central Mumbai. 4. Perfect Project Location: We believe that location of the project for a real estate company is of supreme importance. With respect to Man Infra, all its existing projects are located in popular and densely populated areas of Mumbai – Mulund, Ghatkopar, Sion and Dahisar. Owing to a strong demand in these areas, the price correction (if at all) is very limited. Eventually this should translate in better sales realisation and margins for Man Infra as and when projects start.

Good Reputation as a Builder: Real estate buyers always look for some trusted brand or name on which they can rely upon. Man Infra has lived up to the brand by providing quality construction and timely delivery of its projects. In March 2015, the company completed one of its residential projects at Ghatkopar East in Mumbai where it has also obtained Occupation Certificate ahead of scheduled delivery of the project by 6 months. Its past execution as EPC provider to companies like Godrej, Wadhwa and Tata among others is further testimony to its execution skills. We believe that all of this will help the company to sell better than the competition.

High cash Balance which provides higher Liquidity: The company is sitting on a high cash & bank balance worth Rs. 4,852mn in FY17 and Rs. 5,373mn in Q1FY18 which provides the company with higher liquidity.

Investment Risks

Heavy Dependence on Residential Segment Man Infra is heavily depended on revenues from the Residential Segment. Moreover major part of its order book also consists of orders from the Residential Segment. Such dependence on a single segment may prove to be very dangerous for the company if this segment faces some slowdown in the future.

Competition from New and Existing Players India’s Infrastructure needs have got attention from major national and international players. It is very likely that Man would be facing tough competition particularly in the Port Infrastructure segment from other established companies. Winning of contract bids (both private as well as public) may just become that much more difficult.

Regulatory Delay for Approval of Projects: As the company has a policy of starting projects only after all approvals are in place, any delay in regulatory approvals can lead to subsequent delay in project implementation.

Investor Presentation for H1 FY 2018 can be downloaded from this link:

SUNDARAM MULTI -PAP —branded name in printing and stationary.

Nature of the Business:

The Company designs, manufactures and markets paper stationery products exercise note books, long books, note pads, scrap books, drawing books, graph books – for students of all ages, as well as office/ corporate stationery products and printing, writing & packaging paper. Company has over 190 varieties of paper stationery products under the brand “Sundaram” which are very popular among the student communities and enjoy very high reputation in the market for its superb quality and durability. Sundaram is strong Brand in Education stationary market in western India for almost 3 decades. In Maharashtra it is one of the top two brands with 15% market share.

Business History:

The Company was incorporated on 13th March, 1995 with the Registrar of Companies, Maharashtra, at Mumbai. Shri Amrutbhai P. Shah and Shri Shantilal P. Shah promoted the Company. The Company took over the partnership firm viz. Starline Industries engaged in the manufacture of exercise note books, account books and other paper stationery products, with its assets, bank liabilities and business and the said promoters were the partners of this partnership firm. The purchase consideration was fixed at Rs. 42 lacs and the same was paid by the company through the issue of 4.2 lacs Equity Shares of the company at par. The Company made its maiden public offer of 1.8 million Equity Shares of Rs. 10/- each for cash at par aggregating to Rs. 18 million on 23rdFebruary, 1996 which was fully subscribed and obtained the listing of its Equity Shares on Pune and Ahmedabad Stock Exchanges. In July 2005 the Equity Shares of the Company were also listed on BSE.

At the start of the Company in the year 1995, the Company had a capacity of 5 tons per day of conversion of paper into paper stationery, which was increased to 20 tons per day in 1998 with the addition of two German made machines, to 50 tons per day in 2001 with the addition of one more unit of manufacture, and to 60 tons per day in 2003 with the addition of one more unit of manufacture. The Company’s existing capacity of conversion of paper into various paper stationery product stands at 15,000 tonnes of paper per annum. Current utilisation stands at around 45%.

Company had formed a wholly owned subsidiary, E-Class Education System Ltd in 2010. E-Class Education System is an audio-visual educational content development company focusing on school education. E-class, company’s first product under E-Class Education System ltd is an audio-visual, animated content, exactly as per the syllabus of Maharashtra State Board, Standards 1 to 10, available in English, Marathi and Semi-English Medium. This way each school can have its own digital classroom, and this product can also be used by coaching classes and individual students at home. Maharashtra has around 2 crs students so there is a huge opportunity for this business.

FUTURE PLAN

To Be Debt Free

Management has reduced its debt from Rs. 120 crs to Rs. 37cr as on 07.12.17. Company will be almost debt free by FY18 end. Interest cost will come down by Rs. 5 crs in FY18 i.e. reduction of around 50%.

Company has paid another 7cr recently and total debt is now 37cr—Rs 17cr long time and 20cr working capital.

Reason for losses in past

Due to high debt level of around Rs. 120 crs, management was not able to procure ample amount of papers for production of exercise books and therefore the utilisation level fell down to 50%. Sales fell to Rs. 88 crs in FY16 from Rs. 120 crs in FY13.

High interest cost, lower sales and fixed expenses lead to loss of Rs. 3.6 crs in FY14, Rs. 23 crs in FY15 and Rs. 8 crs in FY16. Accordingly market cap of the company fell from Rs. 500 crs in Oct’13 to Rs. 50 crs in Apr’14.

Post repayment of debt, utilisation of notebooks will ramp up gradually and accordingly topline and profitability.

De-merger of E-Class business (Value unlocking for shareholders, not yet publicly announced)

Management is planning for demerger of its E-class business and to list it on exchanges in FY18. Company may announce the same by April’17 end. This will be a value unlocking for the shareholders. Ebitda margin from E-class business is around 40% i.e. 2x more than Exercise books business which is around 13-18%. Sales from E-class business will be around Rs. 6 crs in FY17. This business was doing sales of around 2 crs in past. Company has won orders under e-class from various municipal corporations in Mumbai such as BMC, TMC, PMC.

Expansion of Exercise Notebooks Business

On the other side management is also planning to sell its 25 acres land (non-core) at Nagpur valuing around Rs. 40-45 crs. The amount will be used to expand exercise notebooks business in South, pay debt etc.

Valuation

During FY16, Company had reported loss of Rs. 8.7 crs after considering loss on sale of non moving inventories of Rs. 10.6 crs (exceptional item). All obsolete inventories have been disposed upto Q1FY17.

Management is expecting topline of Rs. 130 crs from Exercise notebooks business and Rs. 10-15 crs from E-class business in FY18. PAT margin would be around 9% in notebook business and 30% in e-class business. No tax due to carry forward losses.

Profit will be around Rs. 14.2 crs and Eps of Rs. 0.60 in FY18.

. Considering restructuring, future announcements, expansions and improvements in future earnings, stock will move back to its earlier level of Rs. 20-25 in 2 years.

Company has made profit of 2.6cr and top line of 32cr in 1st quarter of 2017-2018.

mIn q2 mad profit of 25 lakhs. But over all made loss of 16cr due to exceptional item.

Prediction of topline for 2019-20120 is around 200cr and profit will be around 24-25 cr.

Equity dilution

Company has allotted 2.6cr share at price of 3.01 to group of investor and collected 7cr rs.

Equity of company is now 24.56cr---- Promoter has 24% and other has 76%.

Company has emerged as one of the leading PET- recycled RPSF manufacturers in India. We pioneered the manufacture of Recycled Polyester Staple Fibre (RPSF) and Recycled Polyester Spun Yarn (RPSY) from pre and post consumer PET Bottle scrap.

Having its manufacturing units at Kanpur (Uttar Pradesh), Rudrapur (Uttarakhand), and Bilaspur (Uttar Pradesh) Ganesha has a cumulative capacity of 97800 Tonnes per annum(87,600 TPA of RPSF and 7200 TPA of RPSY and 3000 TPA of Dyed and Texturised/ Twisted Filament Yarn) of RPSF and yarn.

Our products find application in the manufacture of textiles (T-Shirts, body warmers etc.), functional textiles (non-woven air filter fabric, geo textiles, carpets, car upholstery) and fillings (for pillows, duvets, toys).

Company Annual report and Research Report highlights

The growth of our topline and bottomline by 4.15% and 20.43% . EBITDA rose by 8.27% on account of improved capacity utilisation, PAT margin improved by 60 bps. Long-term debt-equity ratio of 0.32 and recorded a ROCE of 16.05%.

27% CAGR growth in revenue in last 10 years.Revenues, EBITDA, PAT grew at an average 17%, 16% 6%, respectively, in 2011-16

Recycling will get more importance in days to come from Government and is need of time. So company will not have issues with Raw material.

The products created by company Textile and Non Textile are evergreen segments. The increasing use of Synthetic materials is on rise.So no issues on end product market

It has major presence in North India and have scope of growth in other parts of country

Only listed player in this Niche (as per my finding but I may be wrong). The input raw material collection needs channel so new entrant will face problems competing with this company

SBI Mutual Fund has stake in it. It is still a small cap company so have room to grow.

Key Risks

Promoters have pledged 26.20% of their holding. The Promoter stake has decreased also with time. These two points have hold me to go forward with this company.

The end product of company is used in Textile Industry mainly. So the fortune of company is tied with growth in Textile Industry . Also there are many providers of Synthetic fabrics (yarn) to textile industry.

The Synthetic yarn has market share of around 50% but is very competitive as well (refer the research report for market share). This may hamper or make growth of company difficult in future.

Inviting VP friends to have a look and find loop holes in this one so that we can weigh in pros and cons of this company.

Disclosure - Tracking it and not invested. Planning to buy stakes in small size

I opened a thread on Balmer Lawrie company…

Balmer: Logistic business is bottom line driver, Tour and Travel segment is top line driver

BLC’s expansion plans to provide one stop logistics solutions with diversified operations, like setting up satellite branches

at Guntur and Indore, JV with Vizag Port Trust for setting up a Multi Modal Logistics Hub (which is already being approved

by Central Govt.) and setting up three new temperature controlled warehouses at Hyderabad, NCR and Mumbai would

boost high EBIT margin logistics business.

Balmer Lawrie (BL) is a Mini-Ratna I company with a rich history spread over

one and a half centuries of existence. It has a significant presence in industrial

packaging, logistics, travel & vacations, greases & lubricants, leather

chemicals and refinery & oilfield services. BL is the market leader in steel

barrels, greases and oilfield services in India. Its logistics division is the profit

driver of BL with over 3 CFS in Nhava Sheva, Chennai & Kolkata and offers a

wide range of logistics solutions for ocean, air & road freight. Its oils &

lubricants business has a growing retail presence with its Balmerol brand. It is

also one of the oldest IATA accredited travel agencies in India.

Logistics business to continue to drive growth and profitability with

major expansion plans

With capex plans of ~ ₹ 4 bn over the next 2 years, BL is setting up 3 cold chain

facilities in Hyderabad, Delhi NCR and Mumbai and a multimodal logistics park at

Vishakapatnam Port. With various policy initiatives for boosting agriculture & the

rural economy, considerable upside potential in cold storage usage and eventual

passage of GST, we believe this to be a logical move which would help augment

growth for BL. Also, the mobilization of ample cash reserves towards expansion is

expected to further improve ROE and bolster margins.

Increasing contributions from industrial packaging and lubricants

businesses on the back of subdued commodity prices

The industrial packaging and greases & lubricants businesses have witnessed

considerable expansion in margins in spite of a flat growth in sales due to benign

steel and crude oil prices. BL is also looking to widen its retail presence in

automobile lubricants with its Balmerol brand. We expect that the supply glut in

commodities would continue over the medium term and help the India - Centric

businesses of BL contribute even more to its bottom-line.

Other niche businesses to steadily expand

Travel and vacations segment is expected to continue to do well with stable demand

from government & PSUs for its ticketing business and a push to grow its value

added package tours segment. Leather chemicals and refinery & oilfield services

divisions continue to serve niche markets and offer potential upside triggers.

ANY SUGGESTIONS BY MEMBERS WHO ARE TRACKING THIS STOCK.

Hi,

I would like initiate a discussion on 20 Microns Ltd, a specialty inorganic chemical company. It’s a 190 crores Mcap company with annual revenue of 410 crores and has EBITDA margin in the range of 13%-14%. It has seven manufacturing facilities and sizable part of revenue is derived from export market. For more detail about the businesss one can visit the website - http://www.20microns.com/

Competitive Advantage - Niche specialty chemical player with no major competition, good entry barrier given long term mining leases. consistent growth in revenue and profit.

Valuation: EV/EBITDA of less than 6.0x, manageable debt of about 130 crores, translating into healthy debt to EBITDA ratio of 2.4x

I would request views and opinion on the company, thanks!

SecUR Credentials (Securcred), is a small company that is listed on the NSE SME platform. It is a company into background check (BGC) industry. It is India’s first and only listed player in this space. I think the company forms a part of an interesting industry which has a long runway ahead.

Mcap of 120cr. CMP INR238. Company recently came up with an IPO in November 2017 raising funds aggregating to INR30cr. IPO price INR205 (600 lot size).

About SecUR (website + prospectus):

SecUR Credentials is one of India’s largest background check companies with pan-India coverage and operational capabilities in 14 countries. 15 years of management experience and a 300+ workforce has powered our ability to weld innovation with technology and streamline the background screening process. As a result, our services have been integrated into HR systems for over 350 large companies across 30+ industries.

A thought-leader in the background verification space, SecUR verifies half a million resumes each year and that number is only growing. The key to our continued success is in our DNA; which is defined by our passion for business, innovation in products and processes, and customer focus.

Reach: Pan-India reach extending to all 39732 Pin codes

Innovation: Seamless authentication of information across geographies and institutions through innovation in both technology and processes.

Currently, we are an end-to-end screening services provider to various corporates in the country. We are one of the very few India-based BGC companies to be a member of the prestigious US-based National Association of Professional Background Screeners (NAPBS), APAC Chapter, which is the umbrella body of the largest BGC companies around the globe. We can provide background screening services, for organisations not just in India, but across the globe through our NAPBS connections and have provided our service in countries such as US, UK, Philippines, Srilanka to name a few. Our Company is headquartered in Andheri, Mumbai, with branch offices in Mumbai, Delhi, Bengaluru, Hyderabad and Chandigarh. We can cover every PIN code of the country through our intricate hub and spoke model, which multiplies the geographies we cover through the above branch offices.

Prospectus extract on the background of the company:

Our Company was earlier engaged in the business of providing insurance services and human resource solutions provider. During FY 2015 we recorded Nil revenues since our erstwhile promoters were preoccupied in their other ventures. During FY 2016 we received a single order from Reliance Life Insurance Company Limited. They were our single client during FY 2016. On July 26, 2016 our Promoter, Pankaj Vyas, took over the management and control our Company by acquiring then existing 100% paid-up equity share capital of our Company from our erstwhile promoter CRP Risk Management Limited. Post this change our company was transformed into a Company is engaged in the business of Background Screening (also known as BGC - Background Check) and Due Diligence.

Core focus areas:

BGC Corporates:

Background screening of employees

On-boarding processes

Exit Management

Employee support service

Checks conducted by the company:

Education

Employment

Criminal

Identity

Database and media

Residential

Reference

Credit check

Drug test

Psychometric test

BGC Individual:

India’s first B2C background screening product

Allows individuals to self-certify their CVs

Shifts onus of responsibililty of clean resumes from employer to employee

Due Diligence:

Due diligence for Senior Management hires

Due diligence for partners / suppliers

Due diligence for investments

KYC services

Competitive strengths:

Wide Range of Services

National player, with global footprint

Process: ISO/IEC 27001:2013 certified

Focus on long term revenue stream

Business Strategy:

Extension of target client segments

Expansion of service and geographical offerings

Use of SecUR Number to redefine the market space

Strong Industry vertical based focus

What gives confidence on their abilities is the kind of clientele that they have:

SecUR number - can be a decent opportunity in future, if they scale up big time (website):

'More That 30% Of Candidates Lie On Their Resume’s About Past Employment Details, Salary, Residential Address Or Criminal Record An Inflated CV Causes Damage To Your Bottom Line, Month-On-Month, While The Candidate Is Still In The System One Wrong Hire Can Tarnish The Work-Place, Its Productivity, And The Entire Company’s Reputation

When, on an average, there are 118 candidates applying for one vacancy, a pre-verified resume showcasing the authenticity of the candidate’s claims is a breath of fresh air. Add to that the fact that background screening in India is a trend that is catching on, especially in start-ups for whom valuations mean life or death. Any HR will attest to the value of a pre-verified resume and the ease it brings to the hiring process.The Secur Number is a 10 digit code which enables this benefit by providing a comprehensive verification report that meets industry benchmarks for background checks. Accessible online, this report will aid one in going the extra mile with their prospective employer by showcasing one’s integrity. The employer can then easily access the report with the help of the 10 digit number and download all the authentication proofs in the report.’

Technology - Symphony 3.0 (prospectus):

Currently we are using the software “SYMPHONY 3.0” which is a proprietary integrated workflow software of CRP Risk Management Limited that seamlessly directs, tracks and controls the flow of work at SecUR. It is built on a Java Platform, and offers real-time, online movement of processes, as well as information. Symphony 3.0 has been audited and approved by most of our large IT clients from a n information security perspective. We have entered into a Memorandum of Understanding dated August 28, 2017 with CRP Risk Management Limited for buying the SYMPHONY 3.0 Software along with its database for an aggregate consideration of 797.03 Lakhs. CRP Risk Management Limited had developed in-house workflow software, which is currently in its version 3.0, named Symphony. This JAVA-based plat form is the essential glue which holds together all the operational delivery processes, and ensures that these processes deliver the promised output to the client.

There is a tremendous amount of data which is stored in Symphony 3.0. This is the result of all data being accumulated over a period of close to 10 years, as part of the BGC process being delivered by CRP to its clients. Also, because of the inherent design of the Symphony architecture, the database needs to be acquired in tandem with the software application, as it cannot be extracted from the software.

The key components of this database structure are briefly described below:

Education data accumulated over 10 years: Over the past 10 years, as a systematic and thorough effort, the CRP team had accumulated close to 3 crore education records which have been made part of the Symphony database. These education records include a lot of education record archives from colleges and Universities across the country, which have been acquired and digitized with a lot of effort, and at great expense. On a regular basis, the Operational delivery team accesses this data for conducting education checks, as this process is online (and hence faster), and at no incremental transaction cost. Re-creating this database will not just be cumbersome and expensive.

Symphony 3.0 is also home to another key component of our business IP: All the database of educational institutes – colleges, universities, training institutes, schools – along with the process of verifying education records from them is stored in the form of a Master Database in Symphony. This Master Database extends to all the corporates and employers, who have ever been contacted, along with the detailed process of these employers provide verifications. (Detailed information about the software can be found in the prospectus).

Need for background check (website):

Employee related frauds such as inflated salary slips, exaggerated past designations and misleading academic history can cause damage to the bottom-line month on month while the employee is still in the system. Criminal history, questionable political affiliations and a negative personality can cause severe damage to a company’s reputation and future earning potential. Therefore, it is imperative that companies safeguard themselves by performing background checks on all hires.

Interesting reads:

Emerging trends (prospectus):

While the growth of the background screening industry in India over the past decade has by itself been very exciting, the future holds even more promise. A part from the clear growth drivers of the Indian economic growth story, and the increasing number of sectors adopting it as a good HR practice, we are seeing some clear trends which will give an added impetus to the Indian background check industry.

Expansion across sectors, and organization sizes

Extension to contract and other support staff

Prospective employers asking for a 360 degree view

AADHAAR, and its implications for employee screening

Adoption of employee screening by Government and its affiliated institutions

Ancillary extension, such as Education sector

To summarise:

About the company:

The only listed BGC company

Technology and innovation driven

Good clientele as mentioned above

Serves over 350+ large companies across 30+ industries

Short history but company looks decently placed in an interesting industry.

Low base, size of opportunity large and niche product offering.

1QFY18 revenues have been more than half of FY17 revenues.

At this pace they might conservatively exceed revenues of 15cr and PAT of 3cr for FY18. However, I am looking at this more from a very long term horizon. It is close to 120cr mcap right now.

I believe EBITDA margins on a steady state basis can be 25-30%.

Valuations - very difficult to assess for a small company with such a short history - so will leave it upto you to judge.

Company started operations recently hence has a short history of performance.

Company still small in terms of revenue.

One of the objects of IPO was to buy out Symphony 3.0 software.

Any slowdown, tepid growth in hiring / human capital across industries.

Receivables are high.

Typical risks associated with SME companies - liquidity is low, lot size is high and others.

All the above details have been taken from public material, largely their prospectus, website.

PS: My personal view is given the low base, large opportunity size and niche product offering, it is a play on jobs growth and ever increasing jugaadisation.

Disclaimer: This note is not a research report but assimilation of information available on public domain and it should not be treated as a research report, investment advice or Buy/Hold/Sell recommendation. I am not registered with SEBI under the (Research Analyst) Regulations, 2014 and as per clarifications provided by SEBI: “Any person who makes recommendation or offers an opinion concerning securities or public offers only through public media is not required to obtain registration as research analyst under RA Regulations”. It is safe to assume that I might have the company in my portfolio and hence my point of view can be biased. Investors are advised to do their due diligence and consult a qualified financial advisor prior to taking any actual investment or trading decisions.

Sarda Energy & Minerals Limited (SEML) is one of the lowest cost producers of steel (sponge iron, billets, ingots, TMT bars) and one of the largest manufacturers and exporters of ferro alloys in India.

SEML has become the supplier of choice for many domestic and international customers across more than 60 countries.

Listed on BSE and NSE with Promoters’ holding 71.9%

Manufacturer and exporter of niche grade manganese based ferro alloys.

PRODUCTS OF SARDA ENERGY

Sponge iron (dri)

BILLETS

FERRO ALLOYS (ferro maganise & silico

Maganise)

Eco bricks

MINING

Power

Pellets.

Sarda Energy & Minerals Ltd. is one of the leading integrated steel producers using the direct reduction process for steel making.

SEML’s annual DRI making capacity is 360,000 MT and crude steel making capacity is 240,000 MTPA.

SEML is also one of the largest exporters of ferro alloys from India with an annual production capacity of 75,000 MT.

The captive iron ore and coal mines provide SEML a robust competitive advantage and guarantees continued supply of critical inputs at all times.

SEML commissioned 24MW hydro power plant in Jashpur, Chhattisgarh and entered into PPA for a period of 35 years and a tariff of Rs5.04/KWH. With this operational hydro power capacity stands at 28.8MW. 96MW of hydro power projects in Sikkim, is expected to come on stream in FY19. Besides this, SEML is also working on setting up 53MW of addition hydro capacity in Chhattisgarh.

POSITIVES OF STOCK

1 ) Sponge iron (DRI) prices have appreciated by Rs 7500 per tonne since 13 jan 2017, and now on Rs 22000 rs as on 13 JAN 2018 vs 14500rs on jan 17 (almost more than 50%up).

BILLETS prices have appreciated by Rs 7400 per tonne since 13 jan 2017, and TODAY now on Rs 35000 rs as on 13 JAN 2018 vs 27600rs on jan 17 (almost more than 25%up)

SILICO MAGANESE prices have appreciated by Rs 6750 per tonne since 13 jan 2017, and TODAY now on Rs 71750 rs as on 13 JAN 2018 vs 65000rs on jan 17 (10%up)

Manufacturer and exporter of niche grade manganese based ferro alloys.

As per investor presentation in last 5 year export of ferro alloy highest at 45446mt in 2015-2016 fy year.

in this latest investor presentation they mention FERRO ALLOY EXPORT 42066mt till sep 17.means still 6 month of accounting of ferrro alloy export remaining.So we see ever highest Ferro alloy export in this fy.

In view of its long term strategic plan, SEML is very strongly focused on gaining 100% raw material self-sufficiency.

POWER

SEML prides itself in being one of the select companies which is 100% self-sufficient in its energy requirements. Currently smel are operating 81.5 MW thermal power plant at Siltara plant.

Company has planned for future expansion of an Integrated Steel Plant. In this diversified planning, SEML wish to expand its power generation capacity from its present capacity of 81.5 MW. One more 350MW Thermal power plant is under installation at village Kolam, district Raigarh, Chhattisgarh

Pellets

pellets prices now on Rs 6500rs per tonne which is 4250rs 1 year ago on jan 17 almost 50% up

debt to equity ratio

Ther has been significant debt reduction in last 5 year.

In 2012-13 they have 0.54 debt equity ratio and now only 0.16 today

Overall all thing going in fevour of sarda energy.

METAL SECTOR LOOKS VERY GOOD THIS YEAR.

Definitely sarda looks Gd for long term

FINANCIAL DETAIL.

SARDA ENERGY Reserves & Surplus increse continuously from last 5 year.

in march 2013 they have 884 cr Reserves and as on march 2017 they have 1160cr Reservescompany secure loan also decresing in last 5 year.

in march 2013 they have 487cr secure loan and as on march 2017 they have 281cr secure loan.promoter have 71.9% share of the company which is good.

RISK

AS SARDA ENERGY PRODUCT ARE RELATED TO COMMODITY PRODUCT.SO IN GLOBAL MARKET IF COMMODITY PRICE OF FERROY ALLOY AND PELLETS AND BILLETS DOWN THEN IT DIRECTLY AFFECTED TO SARDA ENERGY.IF CHINA OFFICIALS GIVE CLERANCE TO STEEL INDUSTRY TO RESTART ITS PRODUCTION WHICH ONE RIGHT NOW CLOSE DUE TO POLLUTION ISSUE.

This is my first company analysis here and I have much to thank the VP community for enlightening me about companies, sectors etc.

GNA Axles has been listed for around a year (listed in Sept 2016) and much has been publicly written, researched about this company already. So, I am not sure if the company is going to be a multi-bagger in the near term but still I think there is a lot of potential left in this company to outperform (management has guided to doubling of revenues in 3 years).

Company is in the business of manufacturing and selling rear axle shafts and swindles. Axles are an integral part for any kind of vehicle as they aid transmission and mobility. Company has a healthy 50:50 break-up of revenues between domestic and export markets and has a high domestic market share (close to 65%) in supplying axle shafts to tractor OEMs.

Following is historical performance of this company (data taken from the ARs, IPO prospectus and public forums like Moneycontrol):

I. Revenue, Profit and Loss, Margins: FY18 revenue could easily cross 600 crore at current run rate and PAT for FY18 could be 50% higher than last fiscal. Management has said their order run rate is ~60 crore per month.

*FY18E is projected number based on past 3 quarter performance

II. Capacity utilization and expansion: 80 crores fixed investment in Unit 2 planned through IPO proceeds (61 crore has already been done as of Dec’17). Unit 1 had close to 80% capacity utilization in 2017 for real axle shafts and spindles in FY17. Plan is to have 4m pa pieces capacity from current 3m and the new plant to cater to LCV & SUV segment will be ready by end of 2018 CY.

*DNA stands for Data not available

III. Debt analysis: GNA has been repaying debt since 2016 which is good for the bottom line. Target is to be debt free by 2020.

Interest cost for FY18 will be ~7 crore half of FY17 on total debt of ~100 crore.

Key momentum drivers (for the next 3 years):

Capacity expansion – 80 crores fixed investment in Unit 2. Unit 1 has 80% capacity utilization in 2017 for real axle shafts and spindles)

Road construction schemes like Bharatmala and Sagarmala and rules like e-way bill, mandatory fleet renewal (pending) and growing restrictions on overloading will boost CV demand

Paring of debt with IPO proceeds – Company plans to be net debt free in the next 2 years)

Low competitive intensity (only one other major player Talbros Engg.)

Improvement in rural demand (tractors) with rural initiatives like farm loan waiver, doubling of farmer income

Safe from Electric Vehicles disruption

Key positives:

High promoter holding (~65%) & management looks stable and honest

MF holding (14%)-HDFC, Reliance, UTI etc

High domestic market share- ~60-65% in rear axle market for MHCV and tractors

Key risks:

Debt unsustainability – They have consolidated ~100 crore debt, mostly short term, in books as of FY17 (albeit this is reducing)

Appreciating INR

Appreciating steel price (though limited downside as this is passed on to customers with a time lag)

Cyclical demand in MHCV and tractor market domestically and heavy truck demand in key export markets (though the company is trying to enter LCV and SUV market which is less cyclical)

Bad monsoons impacting tractor demand

Rs. 4 crore contingent liability from different tax authorities could materialise and hit PL

Currently the stock is trading at a P/E of 32X FY17 PAT and 21X FY18E PAT.

The key question is can the management execute on its vision of doubling its revenues to 1000 crores by FY20 funded entirely though internal accruals and also be debt-free? I think the answer to that will depend on how successfully company enters into newer markets (South America, Africa), newer product categories (SUV, LCV) and how quickly it expands capacity. Also, it will depend on certain external factors like monsoons, trade headwinds, govt’s rural push. If all goes well, this company could really outperform the broader market.

Till then, I have taken a position in this company with a time horizon of 3 years and will be adding on dips.

went through interview of oakmark pf manager (interview by saurabh )…its an amazing interview

Bill Nygren: “Value Investing Principles and Approach” | Talks at Google

one of the interesting topics was touched that visa/mastercard… both have very strong moats…

do we have in india any stock (which has a payment gateway ) like them ??

Positive points

1- Largest auto ancillary company in India and among the top 10 in the world as regards capacity.

2- Book Value is 5 times present share price.

3- Has a debt of only 12k crores and against the same has nearly 80+ manufacturing facilities in India and abroad.

4- Main supplier of auto components to Maruti & Tata.

5- Also supplies to top auto companies of the world like Mercedes Benz and BMW

6- Equity value of overseas investments more than 13000 crores.

7- 85% of sales are From overseas units

8- Total annual sales in 2015 - 15000 crores with EPS of RS 40 per share

9- About to be resolved in nclt in a couple of weeks

10- Most likely buyer - Liberty House or Deccan value investors

Industry :

Over the last decade, the global textile and apparel trade has been growing at a CAGR (compound annual growth rate) of 5.6 %. In 2014, it stood at US$ 820 billion. Apparel categories had a larger share of 56% while textiles had the remaining share of 44% in the overall trade. The global textile and apparel trade is expected to reach US$ 1,600 billion by 2025. It is projected to grow at a CAGR of 6.3% over the next decade. The Indian textiles industry, currently estimated at around US$ 120 billion, is expected to reach US$ 230 billion by 2020

Textile plays a major role in the Indian economy. It contributes 14% to industrial production and 4% to GDP. With over 45 million people involved, it is one of the largest source of employment generation in the country. The textile industry accounts for nearly 15% of India’s total exports.

Company :

Products – Fibre, Yarn, Sewing threads, fabric, garments.

They have presence in markets like the European Economic Community, Canada, China, Japan, South Korea, Mexico, Brazil, Mauritius and the Middle East. Also emerged as a preferred supplier to global garment makers like Tommy Hilfiger, Esprit, Gap (including brands such as Old Navy), Zara, H&M, Mango, Benetton and Arrow, among others.

Future - Currently, they operate at near 100% utilisation levels in the yarn business, catering to diverse customer requirements. They are also consolidating the fabric business and are focusing on expanding capacity in this space. Going forward, they have a planned capital expenditure of ` 2,500 crore over three-four years towards the ongoing schemes at Baddi, Himachal Pradesh, as well as proposed expansion in Satlapur and Budhni in Madhya Pradesh and modernisation in other units.

Subsidiaries, Joint Ventures and Associate Companies:

VMT Spinning Company Limited (VMT): This subsidiary of the Company is a Joint Venture with Marubeni Corporation and Marubeni Hong Kong and South China Limited of Japan. The Revenue from operations of the company has increased to 19,112.99 lakhs from 15,663.72 lakhs in the last year. The Net Profit of the Company after comprehensive income worked out to 826.11 lakhs as against 738.97 lakhs in the previous year registering an increase of 11.79%

VTL Investments Limited (VTL): This 100% subsidiary of your Company is engaged in the business of investment. The earnings of the company mainly comes from dividend/interest earned on its investments and profits made on sale of investments. During the year, the Company has earned a net profit of 975.12 lakhs as compared to 357.01 lakhs in the previous year.

Vardhman Acrylics Limited (VAL): This subsidiary of the Company is engaged in the business of manufacturing of Acrylic Fibre. Presently, the Company holds 70.74% shares in this subsidiary. During the Financial Year 2016-17, VAL recorded Revenue from operations of 36,842.96 lakhs against 44,759.18 lakhs in the previous year. The net profit of the company after comprehensive income worked out to 4,099.14 lakhs as compared to 4,080.18 lakhs in the previous year

Vardhman Nisshinbo Garments Company Limited (VNGL): This subsidiary of the Company is a Joint Venture partnership of 51:49 with Nisshinbo Textiles Inc., Japan for manufacturing men’s shirts. During the year, the Revenue from Operations of the company was 5,828.84 lakhs as compared to 5,799.22 lakhs in the previous year. The company incurred a Net Loss of 53.88 lakhs as against a net profit of 153.36 lakhs in the previous year.

Vardhman Yarns and Threads Limited (VYTL): Vardhman Yarns and Threads Limited, Joint Venture with American & Efird Global, LLC (A&E), is an Associate Company of the Company. It is engaged in the business of Threads Manufacturing and Distribution. During the year, the Company has sold its 40% stake in VYTL to A&E and is now holding 11% stake in VYTL. A&E is the second largest player in Threads Manufacturing and Distribution across the world. During the year under review, the Revenue from Operations were 77,857.87 lakhs as against 72,863.26 lakhs in the previous year registering an increase of 6.85%. The Net Profit for the year after comprehensive income worked out to 9,909.48 lakhs as compared to 8,991.66 lakhs during last year registering an increase of 10.21%.

Vardhman Special Steels Limited: Vardhman Special Steels Limited (VSSL) is an Associate Company of the Company. The Company holds 31.39% shares of VSSL. During the year, the Revenue from Operations of the Company was 75,312.90 lakhs as compared to 72,551.41 lakhs in the previous year. The Net Profit for the year after comprehensive income worked out to 1,891.01 lakhs as compared to 405.12 lakhs in the previous year. 43 DIRECTORS’ REPORT ANNUAL REPORT 2016-17

Vardhman Spinning & General Mills Limited: Vardhman Spinning & General Mills Limited (VSGM) is an Associate Company of the Company. The Company holds 50% shares of VSGM. It is a trading Company dealing in the business of Cotton and Fibre. During the year, the Company has not traded any goods. So, the Revenue from Operations is Nil for the Financial Year 2016-17. The Company incurred a Net Loss of 6,851 as against a net loss of 27, 292 in the previous Year.

CMP = 1300

M.Cap = 7480 Cr

Enterprise Value = 9610 Cr

Debt to Equity ratio = 0.52

PEG Ratio = 0.29

PB x PE = 19.15

CROIC = 20 %

RoE = 18%

EPS growth last 5 yrs at CAGR of 24%

Sales growth last 5 yrs at CAGR of 4%

I have used Ben Graham’s formula to arrive at the intrinsic value.

The original formula from Security Analysis is :

V = EPS x (8.5 + 2g)

where V is the intrinsic value, EPS is the trailing 12 month EPS, 8.5 is the PE ratio of a stock with 0% growth and g being the growth rate for the next 7-10 years.

V = 109.1 x (8.5 + 2x5)

V = 2018

Management Quality :

Mr. S.P Oswal is the MD. I have googled with the names of Directors and company for any frauds or SEBI notices. No such cases are reflected.

ORIENT GREEN POWER COMPANY LTD

Market cap as on 05.02.2018 on BSE is 803 Crore

The company was incurring the huge losses in the past three four years. The Company came with IPO around 55 somewhere around 2010. The company has created 425 MW capacity in wind energy in 96 MW in the biomass power. Company was incurring huge losses in fast 3-4 years the stock price went down from the ipo price of 55 to Rs. 10.86 on 05.02.2018.

There were three reasons for the losses

The losses from the biomass business

Unavailability of grid in the Tamilnadu for evacuation of wind power. (Availability around 75%)

High interest loans

Now the situation is currently as follows

Company has sold all the loss making biomass power plants

Grid availability in Tamilnadu has improved more the 95% in last six quarters.

Higher interest loans taken for biomass business has been transferred and remaining loans have been restructured. There is still scope for improvement in the interest cost. For remaining details please see the investor presentation

The company has reported the financials for the Q3 2018 on 25.01.2018. In 9 months the company has generated the cash profit from wind business of Rs. 132 crores (94 crores depreciation + 38 crores of profit before tax) (Refer page 18 of Investor presentation)

Now the almost all the biomass assets are sold company will be only left with the wind business.

Company will report the following estimated cash flow from the wind business in FY 18

Rs 152 cr (Rs 132 crores for 9 months and 20 crores assumed for quarter 4)

Company can report the following cash flow from wind business in 2019

Rs 152 cr + 20 crore assumed in interest saving which looks easily feasible 2% on 1000 crore + 25 crores assumed from the newly commissioned wind energy capacity which will go live in April 2018

So total comes to around 197 core

So 197 crore cash flow on market cap of 803 cr, which looks cheaper to me.

There are some other positives which can be found in the investor presentation and con call scripts.

Hey,

I have been tracking this company since few days and it seems interesting to me and the sector also looks at a turnaround.Could not find a post hence starting a new post.

Jet Freight Logistics Ltd (JFLL) is engaged in logistics business having branches located in various cities in India. Company is registered with International air transport association (IATA) agent for Air cargo. JFLL is providing services for Perishable cargo, Time sensitive cargo and also provide Shipment of Hazardous cargo, ODC consignments, pharmaceutical cargo, temperature controlled and general cargo. Its main segment is transport of perishable cargo which includes handling frozen and chilled meat, seafood, vegetables, fruits, cut flowers and pharmaceutical products.

The company has tie ups with various airlines in the world in order to provide tailor made solutions based on customer needs. It offers the best rates along with the best airline options. JFLL has also tied up with various agents across the world who provide services of making the goods reach from international Airport to the respective destinations depending upon the client needs. The company as a freight forwarder take full responsibilities of shipment from the point of receipt to the point of destination .Pricing is based on nature of goods, location, type of service and facility given to the customer. However sector at which the goods are been sent plays a very crucial role in deciding the price of the goods.

Currently Major part of the company’s revenue comes from Air freight and the company does not have its exposure in regards to ocean freight, in the near future it is planning to increase its business verticals and also start operations with regards to ocean freight. The company is also planning for expansion of its branches in tier II and tier III cities as there is increase in flight connectivity in these cities and there is more scope of business operations.

The demand for air freight is limited by cost, typically priced 4–5 times more that of road transport and 12–16 times high that of sea transport. These values differ from country to country, season to season and from product to product and for different volumes also. Cargo shipped by air thus have high values per unit or are very time-sensitive, such as documents, pharmaceuticals, fashion garments, production samples, electronics consumer goods, and perishable agricultural and seafood products. They also include some inputs to meet just-in-time production and emergency shipments of spare parts.

It is listed under NSE SME segment and hence has a minimum lot size is 2000qty. 2012 2013 2014 2015 2016 2017

Sales 28.64 123.44 118.68 142.80 206.57 216.72

Net Profit 0.22 0.18 0.53 0.73 0.96 3.89

Key highlights-

Promoter has 73.3% stake.

Company is growing at around 50% cagr from 5 years.

Companies pat is being grown at 75%+ from 5 years.

Has good ROE @ 37.89.

Company currently operates under niche segment i.e-providing services for Perishable cargo, Time sensitive cargo and also provide Shipment of Hazardous cargo.