Company has emerged as one of the leading PET- recycled RPSF manufacturers in India. We pioneered the manufacture of Recycled Polyester Staple Fibre (RPSF) and Recycled Polyester Spun Yarn (RPSY) from pre and post consumer PET Bottle scrap.

Having its manufacturing units at Kanpur (Uttar Pradesh), Rudrapur (Uttarakhand), and Bilaspur (Uttar Pradesh) Ganesha has a cumulative capacity of 97800 Tonnes per annum(87,600 TPA of RPSF and 7200 TPA of RPSY and 3000 TPA of Dyed and Texturised/ Twisted Filament Yarn) of RPSF and yarn.

Our products find application in the manufacture of textiles (T-Shirts, body warmers etc.), functional textiles (non-woven air filter fabric, geo textiles, carpets, car upholstery) and fillings (for pillows, duvets, toys).

Company Annual report and Research Report highlights

The growth of our topline and bottomline by 4.15% and 20.43% . EBITDA rose by 8.27% on account of improved capacity utilisation, PAT margin improved by 60 bps. Long-term debt-equity ratio of 0.32 and recorded a ROCE of 16.05%.

27% CAGR growth in revenue in last 10 years.Revenues, EBITDA, PAT grew at an average 17%, 16% 6%, respectively, in 2011-16

Recycling will get more importance in days to come from Government and is need of time. So company will not have issues with Raw material.

The products created by company Textile and Non Textile are evergreen segments. The increasing use of Synthetic materials is on rise.So no issues on end product market

It has major presence in North India and have scope of growth in other parts of country

Only listed player in this Niche (as per my finding but I may be wrong). The input raw material collection needs channel so new entrant will face problems competing with this company

SBI Mutual Fund has stake in it. It is still a small cap company so have room to grow.

Key Risks

Promoters have pledged 26.20% of their holding. The Promoter stake has decreased also with time. These two points have hold me to go forward with this company.

The end product of company is used in Textile Industry mainly. So the fortune of company is tied with growth in Textile Industry . Also there are many providers of Synthetic fabrics (yarn) to textile industry.

The Synthetic yarn has market share of around 50% but is very competitive as well (refer the research report for market share). This may hamper or make growth of company difficult in future.

Inviting VP friends to have a look and find loop holes in this one so that we can weigh in pros and cons of this company.

Disclosure - Tracking it and not invested. Planning to buy stakes in small size

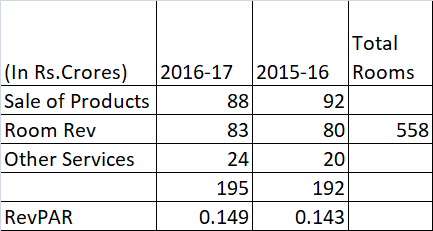

Asian Hotels East owns the Hyatt Regency in Chennai and Kolkata . They have a case going on for allocation of land of 9000+ sq. metres in Juhu in Mumbai and they also own a free hold land in Orissa (Bhubaneshwar) for developing a luxury property there. These are shown at a book value of around 25 Cr but must definitely worth a lot more.

CMP : 280

Market Cap : 330 Cr, Consolidated Debt : ~ 120 Cr

Annual Sales (Consolidated) : ~ 190 cr ( approx 50% each from the Chennai and Kolkata properties)

Total Rooms (5 Star category) - 233 (kolkata)+ 325 (chennai) = 558

Total Revenue - 190 Cr

Occupancy - 69% Image may be NSFW. Clik here to view.

Average cash flow from operating activity is over 35 Cr for last 3 years. Only because of high depreciation (30 Cr), the PAT looks low. One way to look at it is that the money was not well invested in the past - as return on investment is not great. Balance sheet size is ~ 1000 Cr (125 Cr is goodwill on consolidation though) , but market cap is only 330 Cr.

The operating cash flow can explode once the occupancy goes beyond 70% especially in Chennai

Potential triggers : Last Dec quarter there was disruption in the Chennai operations due to floods and last few quarters there was a drop in revenues due to the liquor ban. Inspite of this Revenue from rooms has improved .

I also had a couple of questions –

Does anyone know about current status of the liquor ban?

The room rate at both the hotels is below 7500 on the internet . However the GST rate levied is 28%. Can anyone explain this?

Risks :

Stock is illiquid and it will take time for a large investor to build a meaningful position.

Properties are in only 2 cities Chennai and Kolkata. Kolkata is getting a lot of new hotels starting this FY so prices/ occupancy will be under pressure

I was looking for some contrarian bets.

I have been researching companies for some good picks where I have margin of safety.

to be honest, I didn’t find any with limited time of hard work as I am a full time IT professional…

I am studying IOB and have a tracking position.

This Post is to clear my questions

Life time HIGH is 194 Rs

Face Value : 10

Current price around 23.50

Stock is trading below Book value of 34.

What’s interesting

Bank Recently sold its one of its NPA to Edelweiss

Recent Management interview brings in some confidence.

What are the initiatives taken to address NPAs accounted for by corporates?

About 52 per cent of NPAs are in the corporate segment with majority of them in the consortium accounts. We have an exposure in 10 of the 12 large NPA accounts recently announced by the RBI for resolution under reference to NCLT. The 10 accounts constitute one-fifth (about 20 per cent) of our NPAs. Here we see a timely resolution which is expected to take place — in 180 days or 270 days. Most of these accounts are asset-based. So, we are confident of recovery. Further, having identified these accounts as NPAs, we hold sufficient provisions for their accounts.

on Top of that Recent government announcement on merging PSU or pumping liquidity will be positive for this bank.

This bank is not generating any operational loss…

I have below questions.

Since Government is accelerating the NCLT process and when the bank offloads all the NPA’s

I think this bank should Turn around over the period of 2 years…

Do you agree with me ???

No wonder this bank is a major wealth destroyer but now its provides a margin of Safety as it is trading way below its book value and backed by government.

Do you Agree ??

I haven’t covered any financials here as nothing is much laudable about financials expect the NCLT process which should help the bank to recover the majority of its bad loans

I want to understand from senior boarders if my thought process is correct.

and throw some light on my little analysis.

I am invested in this company and would like to add more after I get more confidence based on my research.

My major questions is when all NPA’s are offloaded to Asset restructuring companies or through NCLT process isn’t this bank should turnaround ? Please provide some thoughts.

Today, the stock idea being shared is of a hotel company. Usually, investors refrain from investing in hotel companies because of cyclicality, concerns about funds being siphoned off from the company, promoter integrity. But, this company is different.

Sinclairs Hotels is a leading hotel chain with most hotels in East India. It has 7 hotels.

The locations are:

1)Burdwan

2)Siliguri

3)Darjeeling

4)Dooars

5)Ooty

6)Port Blair

7) Kalimpong

This company is promoted by the Suchanti family ( Pressman Advertising). Promoters hold 56.96 percent of the shares. Xander, one of the leading PE firms had invested in Sinclairs but they’ve now exited.

FINANCIALS

The company reported sales of 47 crores for the year ending March,2017. They’ve grown their sales at 26 % for the past 5 years. It’s a consistent dividend paying company. It has been debt free for more than 10 years now. Their net profit margin is upwards of 20 percent. The stock is trading at 19 times its earnings.

Now, more about their hotels:

Their hotels have received very decent reviews on various platforms. Their hotels in Siliguri and Burdwan feature at the top of the hotel lists on various hotel aggregator websites. As tourism increases, there’s no reason to believe that Sinclairs won’t be a beneficiary. Today, they have around 450 rooms and they intend to expand to 600 rooms in the next 3 years. They’ve undertaken a greenfield expansion in Rajarhat, Kolkata on a 1 acre plot. They have 396 employees. Remuneration of a key management personnel, who is part of the promoter group is linked to performance of the company. They’re incentivising performance. Prima facie, it does appear promising. Let’s all try to get a better understanding.

Recent new IPO at Rs603 with Rs8540crs market capitalization

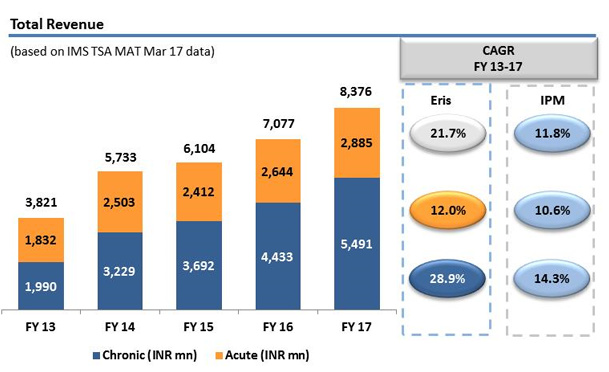

Eris is a pharma company that derives all of its sales from India.

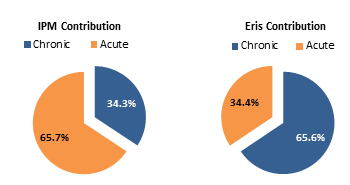

Chronic category contributes to over 65.6% of sales.

Eris has outpaced the Indian Pharmaceutical Market (IPM) growth with a CAGR of 28.9% in Chronic and 12.0% in Acute therapy segment.

Eris is the fastest growing company in Chronic therapy amongst the top 25 companies.

Eris is the 3rd fastest growing company in Cardiovascular and Anti Diabetics therapeutic segments.

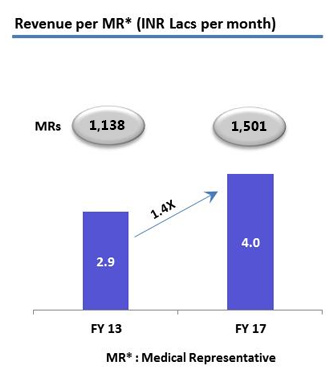

Field force productivity of INR 4 Lac( YPM – Yield per Man per Month) is industry leading and -

Eris is amongst most productive companies in the Industry.

Eris product portfolio is primarily focused on therapeutic areas which are treated by super specialist and specialist doctors such as Diabetologists, Endocrinologists Cardiologists, and Gastroenterologists.

Super specialists and specialists contribute to 96.1% of our total prescriptions as compared to 61.6% for the IPM. We have a prescriber base of 50,282 doctors for Fiscal 2017 as per IMS medical audit. Image may be NSFW. Clik here to view.

Acquires Strides’ India business

Eris has agreed to acquire Strides’ India branded formulations business with 130 brands and Rs181crs sales for Rs500crs.

Key risks as I understand

If products are brought under price control

Business built around strong brands and relationships with specialists/ super specialists, a shift to unbranded generics is a big risk

Net current assets of 2000 lacs++ which includes cash of 105 lacs

What does the co do

Co is mainly manufacturing high end cutting equipment catering to the steel industry

All products are developed inhouse and cater to both domestic as well as overseas markets

Products include Band Saw machines, Circular saw machines, Power Hack Saw machines, Special Purpose machines, Tube mills, Blades and cutters.

These are used by anyone who needs to cut steel

Make machines ranging from 100mm to 3000mm capacity.

Also has trading division (~30% of revenue), selling cutting tools and lubricants for its machines as well as distributing hydraulic components of EATON, USA.

Representative offices in US, Germany, Italy and all across India.

Service network across India.

1 plant in Indore where all divisions are co-located

Did 69.78cr of revenue in FY17… up 24% yoy

Did 7.32cr of EBIT…almost 10.50% margin, up 38%

Did 3.80cr of PAT…almost 5.5% margin, up 72%

Q2 analysis

25% jump in revenue Image may be NSFW. Clik here to view.

44% fall in interest cost✅

117% jump in pbt✅

144% jump in PAT Image may be NSFW. Clik here to view.

190 basis points jump in PAT margin✅Now 4.4%…will slowly move to 10% over next few quarters as operating leverage kicks in

balance sheet also showing all round improvement with reduction in loans, lower days outstanding and better cash position.

What I like about this co

Cos products are unique and have little or no competition in India

1st generation consisting of 2 brothers ran the company conservatively and brought it to this stage. Now 2nd generation, having completes their studies from the best global colleges, is now fully involved and determined to take this to the next level.

In a bad year for industry , the company was able to grow by 24% to almost 70cr last year. I am expecting them to do appx 90cr of sales in FY18, a growth of 28%

If company does 90cr of sales, we could see operating leverage kick in and margins expanding to 15% from 10.50%. PAT margin could see expansion to 8%

By 2020, I expect revenue at 160cr , with 10% net magin

16cr PAT

25 p/e can be given, given high ROCE and negligible debt

400cr target mcap

5x in 30 months

Typically in these small companies…keeping in mind allocations risks…difficult to make a LOT of money.

Disclosure : Own 1% in the company along with many illustrious names…average cost would be around 140…I keep buying intermittently whenever i have some spare cash.

This is NOT a buy recommendation.

Mcap when posted : 60cr

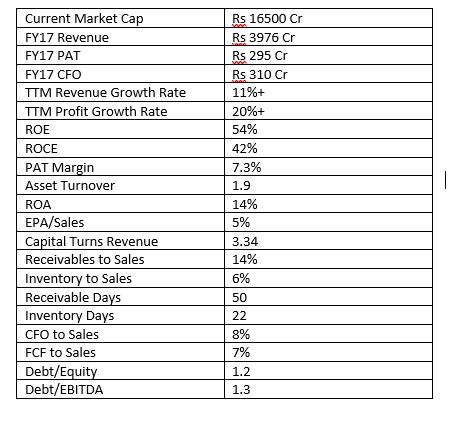

Investment Summary:

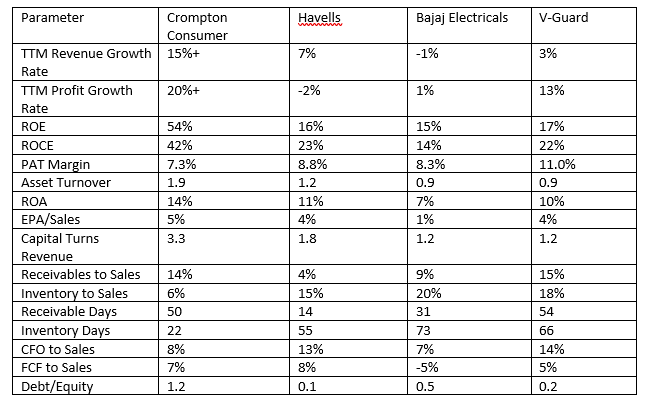

I follow a framework driven approach where I look for companies with strong background, good financial and execution quality reflected through high ROE, ROCE, higher asset turnover, high PAT margin, low debt equity driven businesses with strong management quality available at reasonable valuations. However, sometimes I do break some of the rules if most of the rules are intact and there is genuine case.

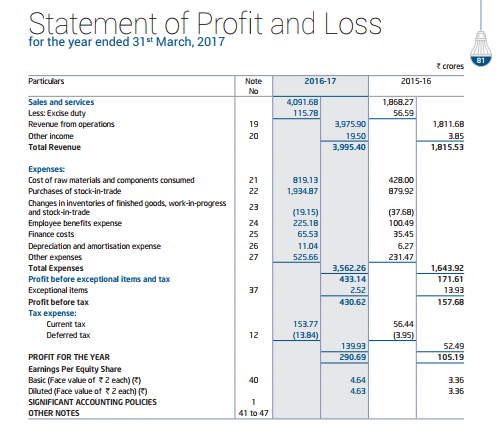

During 2016, while reading an article about the current MD of crompton consumer, Mr. Shantanu Khiosla and subsequently exploring the company, I was impressed by this company during Mar’16 and took a position and have regularly accumulated it. Some of the key numbers are below:

Image may be NSFW. Clik here to view.

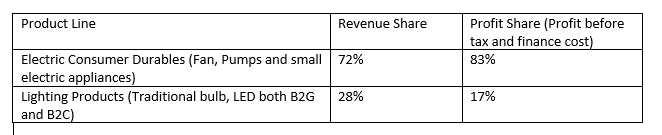

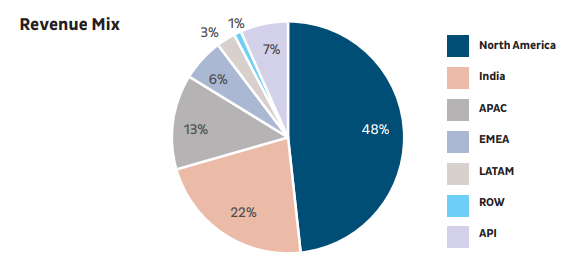

Now coming to business, Crompton Consumer Electric Limited used to be consumer electric business of Crompton greaves present in following businesses:

Fans

LED and traditional bulb and fixtures

Residential Pumps

Other electric goods like iron box etc.

The break up of revenue and profit by product line is as follow:

Image may be NSFW. Clik here to view.

Company history:

This used to be a part of Crompton greaves. However, in 2015, Avanta holdings acquired consumer electric goods business from Crompton greaves and brought Mr. Shantanu Khosla on board.

Now, here is a brief about Mr. Shantanu Khosla:

A P&G veteran for 30 years, Khosla (a graduate of the Indian Institute of Technology, Mumbai, and Indian Institute of Management, Calcutta,) came on board when the world’s largest consumer company acquired Richardson Hindustan Ltd, known for its Vicks brand, in 1983. It was formally rechristened Procter & Gamble India Ltd in 1985. Today, the Cincinnati, US, headquartered P&G has one wholly-owned company in India, Procter & Gamble Home Products Ltd (PGHP), which sells detergents (Ariel and Tide) and shampoos (Head & Shoulders and Pantene), and two listed companies, Gillette India Ltd, which sells razors like Mach 3 and Gillette, and Procter & Gamble Hygiene and Health Care Ltd (PGHH), which sells feminine hygiene products like Whisper.

After several stints abroad over a decade, in places such as Newcastle (the company’s UK headquarters), Kobe (Japan), Singapore and Kuala Lumpur (Malaysia), Khosla, who joined Richardson Hindustan Ltd as a management trainee in 1983, opted to return to India in 2002. “It was my professional desire to come back to live here and make a difference,” he says.

In the driver’s seat for 10 years, Khosla has grown the India business revenue from $110 million (around Rs.592 crore now) in 2002 to close to $1.5 billion as of June, which roughly translates to 13-fold growth, making it one of the fastest growing consumer companies in India. In the last 10 years, rival HUL grew its revenue more than two-fold, to Rs.23,436.33 crore.

The growth came as P&G, a late entrant, took on HUL, which has been in India since 1933. In the detergent space, the two multinationals have engaged at least twice in price wars which led to deteriorating margins for both. In fact, it’s after the losses incurred in one such price war in 2004-05 that the detergent business moved from PGHH, a listed subsidiary, to an unlisted subsidiary in India, in July 2005.

The losses were no deterrent, however. As recently as 2009-10, HUL and P&G were once again warring for supremacy in the detergent space, which is one of the largest and most penetrated segments in India.

Over the last decade, P&G, which operates in 24 categories globally, has increased its presence from six categories to 14 in India and now plans to bring in the parent’s entire portfolio, with the exception of toilet paper, says Khosla.

In the last three years, it has increased its distribution reach by 60% to nearly six million stores, closing in on the gap with HUL, which reaches a little over seven million stores. It is addressing the perception that it’s relevant just to urban consumers. Close to a fourth of its revenue now comes from rural India, compared with 12% three years ago.

Source: http://www.livemint.com/Leisure/dVM4p9Ib1njpjEFxL0QkBJ/Shantanu-Khosla--The-consumer-captain.html

Key to note is he has led one of the biggest FMCG operations across the world and in India has beaten his peers in and out where in 10 years he grew revenue 13 times in 10 years against 2 times by closest competitor.

Why Khosla joined Crompton consumer?

I do not have that article but I was drawn to this company when I read an article titled “60s is new 30s for these CEOs” where Khosla was one of them rolling his sleeves to revive Crompton brand. As per article, his interest to take board position was that he has done all sorts of job in FMCG but taking an old brand, which was quite popular but had lost its charm kind of looked challenging

So, the demerged business has a history of 2 years approx. How Mr. Khosla has done so far. In order to decode this, let us see what Mr. Khosla had promised to his shareholders. This was a crisp 1-page communication with a clear cut 5-point agenda:

Now let us look at how he has done against this 5-point agenda in last 2 years:

Revival of Crompton brand: Visible in higher brand awareness through campaigns (IPL, Test matches) resulting in robust sales and profitability growth

Innovation:

a. Launch of self-temperature adjusting fan

b. Launch of dustless fans

c. Tie up with an European home automation IoT technology player for home automation

Marketing:

a. Refreshed go to market strategy

b. Channel expansion

c. Higher focus on innovative premium products in fan

The overall result of these initiatives apart from point 4 and 5 related to supply chain optimization etc. has been:

Revenue growth of 11% considering demonetization and GST headwinds

22% of operating profit growth

PAT margin improvement from 5.8% to 7.3%

High double-digit growth in premium fan segment snatching market share from competitors (as per con call reports based on 3rd party data)

Doubling of market share in LED segment (consumer) and now no 2 players in consumer LED segment

Focus on new products with an objective to be either no 1 or no 2 players

Conversion of bank loan into NCDs

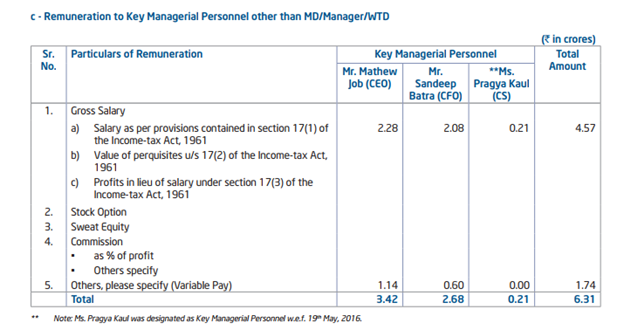

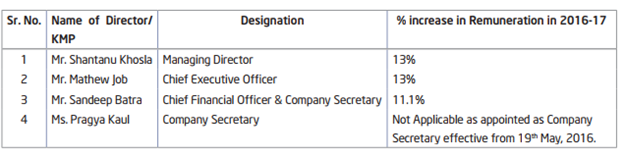

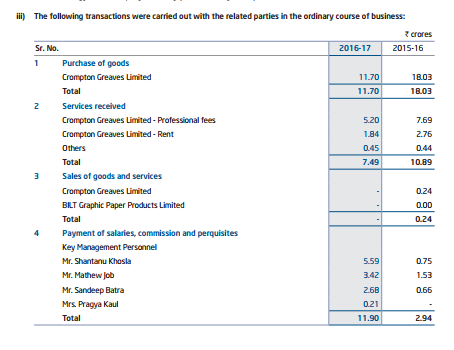

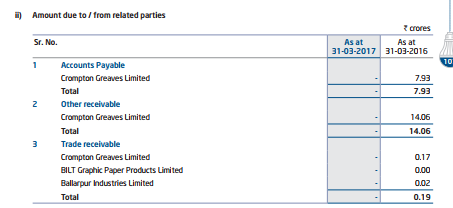

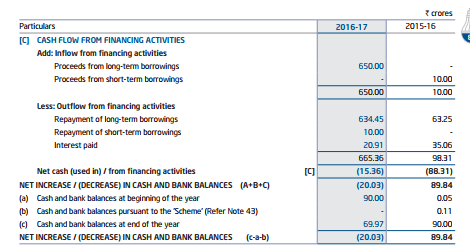

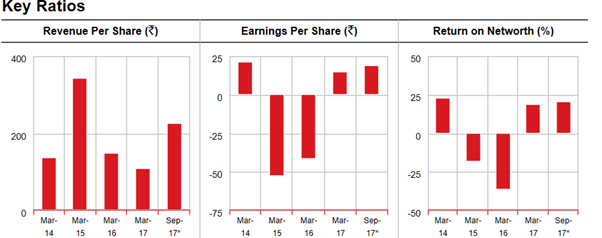

Attaching further numbers about business and management:

Image may be NSFW. Clik here to view.

Image may be NSFW. Clik here to view.

As One can see, management salary is 2.5% of PAT which is reasonable and also increase in management remuneration looks reasonable considering the growth they have achieved in business.

Company is working hard to continue its above market growth rate which means double digit growth

More supply chain optimization, interest cost reduction and higher focus on premium products should further lead to margin expansion

Company trying to get into few new segments like ir purifier (still in pilot test mode) with a mandate to be market leader

Company is active on usage of technology and smart homes and hopefully with a strong management in place, would be able to leverage this opportunity

Pump business has not done that well but with improvement in real estate and rural climate, hopefully will do better

Strengths:

Well proven management in the form of Mr. Shantanu Khosla, walking the talk

Strong performance in topline, bottom line, margin improvement and market share gain

High quality business with double digit revenue and profit growth, 40%+ ROE and ROCE, 7% free cash flow to sales ratio, comfortable debt coverage position, asset light brand driven business model with efficient working capital management

Huge market size opportunity ahead with still more than half market belonging to unorganized player and overall average sector growth (across fan, LED and pumps) growing near 10% highlighting long run way ahead

Concerns:

Debt equity ratio seems a concern at 1.2 but company is generating 300 cr + cash flow from operations and can easily pay 60-70 crores of interest annually on 600 crores of loan and can easily get rid of debt in 4-5 years. This will further improve margins

Less comparable history: Difficult to compare numbers beyond 2,3 years historic basis and one needs to build his conviction based on recent performance and overall trust on management

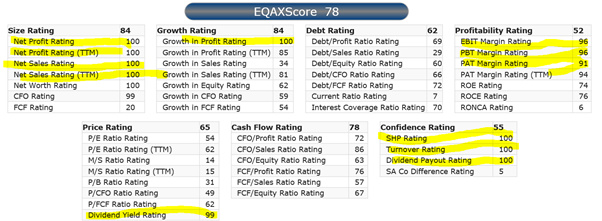

Valuations: I would leave valuations to everyone to pick what is right valuation for them based on their risk appetite, time frame and valuation framework. However, I would throw some data about company and competitors so that one can access its business and competitive strength along with valuation attractiveness:

Image may be NSFW. Clik here to view.

Valuation as on 31st March 2017

Image may be NSFW. Clik here to view.

Company does face some raw msaterial pricing pressure due to chnge in copper prices but so far has been sable to pass it to consumer due to brand power

List of marque investors:

Avantha Holdings (Promoter): 34.37%

*MacRitchie Investments Pte. Ltd: 12%

LIC of India Child Fortune Plus Balanced Fund: 4.78%

Smallcap World Fund, Inc: 4.73%

Nomura India Investment Fund: 2.19%

Franklin Templeton Investment Funds: 1.99%

Amansa Holdings Private Limited: 1.85%

Note: Concall transcripts are very detailed and available at company website. Serious investors if find company attractive must go through last 8-10 quarters of concall transcripts to understand business in more detail Disc: 6% of portfolio with average price of Rs 173

I did not found any specific topic for LUPIN. Hence opening a new thread. This is my first thread on value picker and I am not an expert in equity analysis (in learning phase). Moderators/Admin please delete the post in case it do not suits the value picker community requirements.

Company Overview :

Lupin Limited is a pharmaceutical company based in Mumbai. It is the seventh-largest company by market capitalization and the 10th-largest generic pharmaceutical company by revenue globally.

US Markets :

US revenues surpassed the USD 1 billion mark, closing at USD 1,207 million. a growth of 37% over FY 2016 revenues of USD 883 million.United States remains Lupin’s largest and most important market with 48% share of total revenues.

The Company filed 37 ANDAs and one 505(b) (2) NDA in the US market during FY 2017 and currently has 154 ANDAs pending approval, addressing a total market size of over USD 74.9 billion. Of these, 28 ANDAs are first-to-file opportunities

addressing a market size exceeding USD 13.1 billion. This includes 14 exclusive first-to-file ANDAs targeting a market size of approximately USD 2.6 billion.

INDIAN Markets

During the year ended March 2017, Lupin’s Revenues reached ` 38,157 million, representing growth of

11% over the previous year and 15% CAGR over five-year period. With 3.3% market share, Lupin is the 6th largest player in the Indian Pharmaceutical Market.

JAPAN market:

Japan is Lupin’s 3rd largest market and contributed 10% to our global revenues during FY 2017.

Image may be NSFW. Clik here to view.

TAX rate:

Company recorded Earnings per Share (EPS) of ` 56.69 during FY 2017. The Company’s effective tax rate for FY 2017 was 27.6%.

Risks : Regulatory Risks : Recently US FDA issues warning letter to Lupin’s manufacturing facilities at Goa and Indore for violation of good manufacturing practices.

Debt approx 7900 crores. However Debt to equity ratio is approx .6

Stock has corrected approx 60% from All time high of 2100 to 830 in last 2-3 years. Whole pharma sector is in trouble from last 1-2 years , but I want to see if this can be a buying opportunity keeping holding period of 10+ years (expecting 12-15% CAGR return) considering managment is v good and they will come out of all troubles in long term.

Requesting for VP seniors and fellow VP’s to look for the value in the stock and help me to find difference between compounder or wealth grower on the aforesaid company for long term horizon of investment .In case there is similar thread please merge with the original as I haven’t found the company in the search. However another company of the Menon Group is Menon bearing is found in the search

Background:

The Company was incorporated on 25.08.1977 as a private limited Company in the name of Menon Pistons Private Limited in the state of Maharashtra. Due to the increase in turnover of the Company, the Company became a deemed public company on 15.06.1988 and the name of the Company was changed to on 25th June, 1988 and on 10/11/1994 the Company was converted into a full fledged public company vide Special Resolution passed on 10th November, 1994.

Products: Manufacturing of pistons, gudgeon pins and plungers which cater to the automobile industry and power generation segment. it manufactures piston rings and pins for various automobile and industrial engine applications.

Capacity: MPL has two manufacturing units located at Kolhapur and Sangli in Maharashtra. Pistons manufacturing at Kolhapur with an installed capacity of 30 lakh pistons per annum. During 1985, MPL installed second unit for manufacturing of gudgeon pins, pistons and plungers at Sangli with an installed capacity of 6 lakh pistons per annum, 36 lakhs gudgeon pins per annum and 1.45 lakh plungers per annum.

Distribution: The Company has over the years developed a countrywide market divided into four zones headed by the Regional Managers located in the four metropolitan cities under the supervision of Associate Vice President-Marketing based in New Delhi, MPL has eighteen depots located across India situated at East (6), West (4), North (5) and South (3) to cater to customer requirements . Further, the Company has its representatives in each of the states and a wide Dealer Net Work. Among its dealers are reputed business houses such as T.V. Sundaram Iyengar & Sons, Sundaram Motors, Chandok Auto Industries

Major Customers : Cummins India Limited, Tata Motors Limited (rated ‘CARE AA+’), Maruti Udyog Limited, TAFE Motors & Tractors Limited, Eicher Tractors Limited TELCO Ltd. Bharat Earth Movers Ltd… Escorts Ltd. Sonalika tractors , Preet industries ,Emerson ,Greaves india .Lombardini , TVS, Hero honda

Colaboration Since April 2006, MPL has signed a technical collaboration with Dong Yang Pistons, South Korea for the latest technology for manufacturing of Alfin piston.

Promotors : :The Company, promoted by Mr.Ram Menon and Late Mr.Chandran Menon, was incorporated in 1977

The Company has got ISO 9002 certification and also the SHIP-TO USE Certification from Kirloskar Cummins Ltd. for whom Menon Pistons is the sole supplier. This vouches for the quality capability of Menon Pistons.

Menon Pistons is the only Company among the top leading piston manufacturers in India who has developed indigenously the piston making technology and it has developed its own inherent strengths in the design and manufacture of any kind of pistons. This enables the company to face any kind of problems that may arise in the process of piston making and to tackle it confidently. The reputation the Company enjoys in the market and the list of prestigious customers it caters to is an ample indication of its technological capabilities and quality standards.

The Company has got a pre-eminent position in the heavy duty segment and it has got 100% supply arrangement to such market leaders as Kirloskar Cummins Ltd. and Bharat Earth Movers Ltd. Moreover, it is having an increasing presence in the car piston segment. The market share in the car segment is continuously increasing. Moreover, the car segment is slated to be the fastest growing segment in the near future. The Company has an annual average cumulative growth rate of 22% during the last ten years.

Company’s export market ;MPS export their piston assembly and other engineering goods to erstwhile U.S.S.R., U.K., Germany, Greece, Arabian Gulf, Middle East, Australia, South East Asia and other countries. They had become the pioneer suppliers for Autolada vehicle in erstwhile U.S.S.R. and supplied 4.0 million pistons for LADA Cars in different types and sizes

Products application;

• Heavy Duty Diesel Engines for Power Generation / Off Highway Vehicles / Gas Engines

• Heavy/Medium/Light Commercial Vehicles with Diesel Engines

• Passenger Car (Diesel & Gasoline) Engines

• Bi-wheeler (4 Stroke) / Small Engine Applications

Technical Collaboration : Dong Yang Piston South Korea

Rational of investment :

• India Piston and Piston Rings Market: The Piston and Piston Ring market has been one of the fastest growing auto component sectors attributing its success primarily to the automobile sector and demand for higher powered engines. The increasing development in infrastructure, a growing domestic market for automobiles backed by new model launches, increasing purchasing power and stabilizing the government framework will draw in major investments both domestically and internationally

• Ability of MPL to improve its scale of operations, profitability margin having value addition on products

• Effective management with long length of engineering background

• Promotor Holding : 74%

• Growth indicators Growing cash reserve / reducing debt / Continue dispersing the dividends /Profit growth 3Years: 54.84%.

• Niche Sector have strong R&D and technical setup Image may be NSFW. Clik here to view.

Achievements/ recognition:

• The First Company in India to develop Ring Carrier Pistons

• Best Vendor Award from Maruti Udyog Ltd in the year 1994–95

• Ship –to – Use Status by Cummins India Ltd since 1995

• Faster Development Award from Kirloskar Oil Engines Ltd

• ISO/TS: 16949 Certified by TUV-S in 2005

• Outstanding Supplier for Excellent Performance award from Cummins Group in July 2006

Concerns:

Fluctuation of raw material cost :vulnerability of operating profitability to volatile raw material prices

High P/E ratio

working capital intensive nature of operations

Cyclic industry demand for the auto components

Questionable financial ethics:

• Mr. Sachin Ram Menon & Mrs. Gayatri Menon (Couple Promoter, Chairman & Managing Director of the Company) has given Immovable property has given on rent to the Company ; i am not able to find the reason

• Vehicles not directly involve in company value addition are being financed from H.D.F. C Bank Ltd. - Vehicle Loans a) Vehicle -I (MH09-EK- 0344) Hyundai-I20 b) Vehicle -II (MH09-EK- 0356) Hyundai-Creta

• SHORT TERM BORROWINGS: Cash Credit against Secured by hypothecation of Raw Material, Work in process and finished goods and equitable mortgage of Land and Building situated at 182, Shiroli, Kolhapur and at H-1, MIDC, Kupwad, Sangli However the company is on rent from promotor

Snip from annual report 2016-17 Image may be NSFW. Clik here to view.

Disc: Having started tracking position with 3% of my portfolio invested in the company may be my views biased , This is not investment proposal do your own research before investing looking forward for the views and arguments to negate my rational of investment and reply to my concerns .

have been a reader to valuepickr since long , recently met Ayush Mittal at an event and after listening to him thought of sharing few of my thoughts on the forum !!

coming to the topic i want to discuss with you all is " fate of adag group " is this an opportunity for wealth creation or threat for further value erosion ??

frankly i dont know !!

but i am trying to anlayse the situation and welcoming view from all to have better clarity .

i have always believed that in investing , best of the opportunity is available in worst of the circumstances . there are many many examples available like sub prime crises , spice jet issue , maruti suzuki plant closure & riots etc.etc… whoever investor have tried to analyse the situation and was able to diffrentiate maruti and spice jet from jp & suzlon have created a tremendous amount of wealth for themselves .

so is adag group a suzlon is making or future spicejet ???

ADAG group mainly have 3 companies rcom , relinfra & rcap .

as we all know

rcom is clearly in trouble and major worry is whether will it be able to pay off debt and liabilities it has created ?? if not , how will it affect other companies ?

relcapital is nbfc and it is a fancy sector of recent bull phase . known liability is around 1200 cr loan being given to rcom and may be holding rcom in some scheme . sector has lots of potetntiial as we can learn from other players in the same industry . how rel capital is doing ??

rel infra is in to power ( former bses ),infra and defence ( recently ) . here also large amount of debt is an issue which is around 35000 cr aproximately.

how adag group will tackle the looming debt problem ( first rpiority ) , growth ( second priority ) and profiltability & visibility of smooth days ahead , a kind of third priority ??

will keep my views in days to come .

i will appreciate to have feedback from other members

My first post here, greatly appreciate the quality of discussion on the forum.

Saw this stock on screener.in while running a few filter. Has good yoy growth, low P/E (14.8), Piotroski score of 7, ROCE is low (10%), Price to Book is 2.26. Listed at around 170, now around 380. Has risen 30 Rs in the last few days.

Established in lat 19th century, Owned by the Royal family of Travancore, so no fly by night operators here, although it may not mean they are the most business savvy. Has a very unique product, they make specialty coffee, the only ones in the world. It is called Monsoon Malabar. Retailed by Nestle and other niche coffee players. Also have a logistics business, have not been able to delve further into it. Am guessing the Company also has significant land holdings, they recently entered into a partnership with DLF to establish a Heritage Hotel in Kochi.

Porinju Veliyath has a 1.5% stake in the company.

Company looks very interesting, early stages though. Would welcome your analysis and possible downsides.

Disc: Invested, will continue to buy and hold for long term

This is my first post, please forgive me for any mistakes or violations. Senior members please share your view on the stock. Alufluoride Limited-conversion o (as PDF).pdf (517.0 KB)

Disclosure : Invested in the stock(2% of portfolio) looking to add on declines.

5 Positive things according to me-

1.McLeod Russel, the world’s largest tea producer, offloaded 9.14 per cent of its stakes in the open market raising over Rs. 200 crore in a day’s trade. The money raised thus, will be used to reduce its current debt burden of Rs. 790.67 crore.

2.Sold loss making subsidiary for approx 13.7 Crores.

3.Strategic alliance with Everready to sell Tea packets.

4. Investment of 100 Crores in irrigation project to deal with weather condition.

5. low production of tea in kenya n other african countries.

I am silent member of this group from last 4-5 years. Since most of the stocks / idea covered by the group so there are very few new opportunities available in the market.

I found this company ( pritika auot) worthwhile to dig more.

The earlier name of this company was Shivkrupa Machineries and Engineering Services Ltd. Until last year this was trading company for auto parts.

Last year pritika become the holding company by acquiring 100% stake in following companies. So trading company become the full fledged auto ancillary company.

Both companies were in the business from long time so current trading company become an auto-ancillary company.

As per comoany’s website all major oems be it maruti, suzuki, toyto, mahimdra, escort, swaraj, tafe, ashoka leyland, eicher, sonalika, sml izu are their clients.

Recently there was some good announcement by the company.

Increasing authorised share of capital to rs. 5 crore

Promoter is infusing capital into business by subscribing around 7 lakhs share

Company is issuing 37 lakhs share to some person ( classified as public not known).

On a prima facie things are happening in a positive direction. Company has consolidated debt of rs. 41 cr so new promoters are likely to pay high cost debt by infusing capital or introducing some PE ( 37 lakhs shares are being issued).

On a consolidated level company posted around Rs. 11 Crore ebidta for 6 months with 83.3 Crore revenue. Working capital Cycle seems to be bit stretched WC ( non cash and non debt) to sales is around 50%.

As per the announcement, Company has participated in auto exhibition in Germany and response is very good.

This company’s Head Quarter is Chandigarh and they have factory in HP and Chandigarh as well.

SML Isuzu Limited (SMLI) is a trusted and reliable commercial vehicle manufacturer since 1985. It has over 25 Years of experience in producing Light & Medium commercial vehicles to meet the Indian customer needs. SMLI is a first company to manufacture and supply state of the art fully built Buses, Ambulances and customized vehicles.

Sumitomo Corporation, Japan and Isuzu Motors, Japan respectively holds 44% and 15% shareholding in the Company.

This is very good CV cycle story with added benefit newer Vehicle launch.

Recent Observation:

Company is highly ignored as we have better results coming from other players.

They have faced recent profit growth issue's due to Bharat Stage norms & supply issue.

Newer model & marketing related expense.

Pros for Trigger:

Good vehicle inventory

Expanse of delivery network is going on nicely

Good price points entries & they can complete properly in SUV & HV segment.

Industrial activity demand improvement will be visible.

Good ROE

Good Capital allocation

Good Dividend History

Share holder friendly Management

Vehicle scraping policy will be big boost.

Cons to Consider

Competition from large player

Raw material Spike

Demand for Vehicle can dampen, but highly unlikely

Pick up in CV cycle is not happening at desired pace, keep watch on it.

profit was depressed as sales was depressed due to GST, Demoney & Bharat Stage norms, So once we start seeing good result it will be in Investment radar

Financials:

Image may be NSFW. Clik here to view.

As on 19-Dec-2019 :

Return on capital employed: 21.92%

Return on equity: 16.95%

ROCE3yr avg: 18.71%

Reserves: ₹ 388.04 Cr.

Debt: ₹ 38.64 Cr.

Book value: ₹ 280.52

Net worth: ₹ 402.52 Cr.

Operating cash flow 3years: ₹ 175.02 Cr.

Cash Conversion Cycle: 44.18

Average return on equity 3Years: 15.65%

Market Cap to Sales: 1.1

Wide Range of Products Both in Cargo (5 – 12 ton) and Passenger Categories (13 - 52 seats)

Installed Capacity

18000 Vehicles

4000 Bus Bodies

Disc : Little bit of investment done .

I would be monitoring vehicle sales & if we see it moving north side then keep adding.

Vedanta Limited, formerly known as Sesa Sterlite/Sesa Goa Limited, a Vedanta Group company is one of the world’s largest global diversified natural resource majors, with operations across zinc-lead-silver, oil & gas, iron ore, copper, aluminium and commercial power

Moats: Low cost Producer Heavy capex needed which create barrier to entry Geographic advantage Low Transportation being at Goa Scalability having sound balance sheet Unique natural resources company Diversified risk probably one of its kind

Stock: Cyclic; Mining; Metals; Diversified Natural Resource CMP: 318 P/E: 9 52week+/_ : 205 & 346 Face Value : 1

Risks:Image may be NSFW. Clik here to view.

• On the aluminium side, market has been developing very well and there have been some constraints in supply. Mainly in China, there might be some restrictions because of the environment factors

• Recent coal and pollution measures along with coal availability to not improved

• Vedanta had augmented large capacity through acquisitions and capex, which was largely debt funded

• Contribution of metals, minerals and oil and gas in India’s GDP is only 2 per cent

• Govt regulations and Chinese competition for more risk and opportunities one can refer to IPO in the referenceImage may be NSFW. Clik here to view.

Opportunities:Image may be NSFW. Clik here to view.

• Vedanta have a very strong balance sheet. It gives company an edge for immense opportunities to grow.

• Vedanta has a diversified business risk profile spanning iron ore, copper, zinc, lead, silver, aluminium, power, and oil and gas, and will benefit from long-term growth and business opportunities in each segment.

• Assuming Indian growth at plus or minus 7.5 to 9 percent, in ten years’ time, the demand for metals will grow to about three to four times the current size of the market (company’s version)

• of mining operations in Goa and lower transportation cost,and reducing production cost conversion of 1800-megawatt (MW) to aluminium segment at Vedanta Aluminium, and replacement of old 270 MW power plants with new 600-MW captive power plants at Balco during fiscal 2017

• In the oil and gas sector huge opportunity and as it can scale up with investment to further enhancing its crude production capabilities.

• Geographic advantage: The company has a presence across India, South Africa, Namibia, Australia and Ireland. Vedanta is the Indian subsidiary of Vedanta Resources Plc, a London-listed company

• Future Outperformer: Global investment firm Credit Suisse has initiated coverage with an outperform rating on the stock as it is a leveraged play on aluminium.

Fundamentals Image may be NSFW. Clik here to view.

History :Image may be NSFW. Clik here to view.

Last 10 years at Glance Major events

2006 : Vedanta Resources plc, a diversified metals and mining group, listed on the London Stock Exchange acquires 51% controlling stake in Sesa Goa Limited from Mitsui & Co. Ltd.

2009 : Sesa Goa Limited acquired all the outstanding common shares of VS Dempo & Co. Private Limited, along with its 100% equity shares of Dempo Mining Corporation Pvt. Ltd and 50% equity shares of Goa Maritime Private Limited.

2011: it has acquired the assets of Bellary Steel & Alloys Limited (BSAL)

2012 : - Sesa Goa Limited has completed the acquisition of Goa Energy Private Limited & Sesa Goa Limited announces that it has acquired the remaining 49% of the outstanding common shares of Western Cluster Limited

2014 : -SSL- Kitchen Waste Producing Cooking Gas and Creating Greenery in Lanjigarh & it Announces Development of Gamsberg-Skorpion Integrated Zinc Project

2015 : -Sesa Sterlite arm gets approval for starting power plant& restarts mining in Karnataka : completed the merger of its subsidiary Sterlite Infra with itself and renamed Vedanta Limited

2016 : -Vedanta Successful bidder of Gold Mine : merger of Cairn India Limited

History credit rating Image may be NSFW. Clik here to view.

CSR & Sustainability:Image may be NSFW. Clik here to view.

Football club promoted by this company SESA F.A:soccer:

• in 2016 Vedanta recycled 47% of the fly ash

• in 2016 vedanta recycled 23% of the water utilized during its operations

• It has unique Public-Private-Partnership (PPP), with the Ministry of Women and Child Development, Government of India to start Project Nandghar developing Aanganwadi infrastucture

• Continuous improving the life vide community development programme with regular investments

Quality Mutual funds increasing their stack in the company from last 5 years viz HDFC Mutual Fund ;Aditya Birla Sun Life Mutual Fund ;UTI Mutual Fund ;Reliance Mutual Fund ;SBI Mutual Fund ;ICICI Prudential Mutual Fund ;DSP BlackRock Mutual Fund ;Kotak Mahindra Mutual Fund ;Mirae Asset Mutual Fund ;L&T Mutual Fund

Disc: Currently not invested looking forward for views and need help to find out additional threats and opportunities that I couldn’t documented .It is not investment proposal do your own research before investing looking forward for the views and arguments to negate my rational for investment and reply to my concerns

Simmonds Marshall’s main business is industrial fasteners used in auto and engineering industry. Simmonds was incorporated as a Private Limited Company in technical and financial collaboration with Firth Cleveland Fastenings Ltd., U.K. holding 51% of the equity of the company. This shareholding was diluted progressively and the balance of foreign holding was purchased fully by the current promoters in 1987. The company’s promoters are one of the most reputed and financially strong business houses of pune. The company supplies a range of Specialised Nylon Insert Self Locking Nuts and other Special Fasteners to all the two-wheeler manufacturers in the country and almost all major four-wheeler manufacturers in the country. The company does not focus too much on the CV segment as of now. The company had started focussing on exports some time back and the results have been very encouraging. Now the company plans a major thrust on exports which also gives natural hedge to the company, along with much better margins. The company has also been successful in acquiring new customers and also getting bigger orders from existing clients by wresting away orders from its bigger peers.

Brief Description

Coromandel International Limited is engaged in the manufacture and trading of farm inputs consisting of fertilizers, crop protection, specialty nutrients and organic compost. The Company’s business divisions include Fertilizers, Specialty Nutrients, Crop Protection and Retail. It offers various products in fertilizer segment, including Nitrogen, Phosphatic and Potassic in various grades. Its specialty nutrients consist of water-soluble fertilizer, sulfur products, micronutrients and organic manure. Its crop protection products consist of insecticides, fungicides, and herbicides. Its retail outlets operate as Mana Gromor Centers. It manufactures a range of fertilizers and markets over 3.2 million tons. It operates a network of over 800 rural retail outlets under its retail business across Andhra Pradesh, Telangana, and Karnataka. It has manufacturing facilities in Andhra Pradesh, Tamil Nadu, Karnataka, Maharashtra, Madhya Pradesh, Uttar Pradesh, Rajasthan, Gujarat, and Jammu and Kashmir.

Sector Overview.

UPA Govt introduced Nutrient-based Subsidy Scheme( NBS ) in 2010. It was meant to reduce subsidy burden on the government. While it did not achieve the desired results, it created more problems especially its impact on farming practices and soil health. The immediate outcome of this was a sharp decline in the use of phosphoric and potassic fertilizer mix, with an increase in urea consumption. There is a prescribed usage ratio of fertilizers. Ideally, the NPK usage ratio should be 4:2:1. For the year 2013-14, NPK ratio in Punjab was 61.7:19.2:1; in Haryana, it was 61.4:18.7:1; in Rajasthan, it was 44.9:16.5:1; and in Uttar Pradesh, it was 25.2:8.8:1.

Now the government has decided to fix this issue through Direct Benefit Transfer(DBT) along with soil health cards. Direct Benefit Transfer (DBT) in fertilizers was introduced on a pilot basis, with pan India rollout likely to follow in 2018. DBT has the potential to overcome the distortion of NPK usage as the farmers will now have the choice in deciding the usage. Besides the fertilizer industry has been suffering due to the increasing receivables due to govt subsidy policies. DBT will also address this issue and benefit the companies in this industry. The 2016 Economic Survey estimated that only 35% of the subsidy reached intended beneficiaries, and as much as 41% of urea was redirected to industry or smuggled out of the country. Nearly half the farmers bought urea at above MRP in the black market. DBT will incentivize the industry to create more supply.

Also, the government is hell-bent to reduce the imports of all kinds of fertilizers especially Urea. Source

Company Overview

Coromandel belongs to murugappa group. So it has a very decent management, which is evident from its operating efficiency of previous years. In an industry which is suffering from govt policies, coromandel stands out. Its ROE and ROCE are well above the industry average. This was possible due to its product mix and continually tried to increase revenues from non subsidized fertilizers. In addition, the Company also holds 14% equity stake in Foskor Pty Limited, South Africa, through combined holding of Coromandel and CFLMauritius Limited and a 15% equity stake in TIFERT, a strategic investment of the Company to secure supply of Phosphoric acid which is the raw material for its fertilizer business. Due to this Coromandel is the lowest cost producer of Phospharic fertilizers.

Its also investing into crop protection chemicals and farm mechanization. Its 800 plus GRoMor stores will nicely complement these new ventures.

Its evident from the below graph that the stock almost traded sideways for the last seven years and looks like a strong uptrend has started.

Major risks include

Govt not able to implement the planned reforms.

problems in its subsidiaries especially the ones which are in tunisia, south africa from where it sources its raw materials.