Vasa Retail ( Vasa ), is a small company that is listed on the NSE SME platform. Mcap of 22cr. CMP INR37. Company recently came up with an IPO in February 2018 raising funds aggregating to INR4.80cr. IPO price INR30 (4000 lot size). It is a company into stationery distribution, offers everything that a person might need in terms of stationery.

* Screener link: https://www.screener.in/company/VASA/

* Company website: https://vasagroup.in/

* Background: Vasa began business from the Gulf in 1967 by Late Bhupendra Vasa, the original promoter. Middle East as a business has thrived since 1970s after the oil surge. Hardik Bhupendra Vasa, the current CMD, joined business in 1997-1998. Hardik Vasa is 42, an engineer who has done the IIM-A accelerated management program. Company was incorporated in October 2017 as a conversion from partnership firm to public limited company. Business was done under partnership firm mode since 1994. Branded stationery products (not paper) as a segment has been started recently in last 7-8 years.

* Branded products: Co has the most prestigious and recognized brand in global education…‘University of Oxford’.

* Oxford association: Vasa has exclusive license agreements to make, market, sell, distribute and promote various stationery products under the brand ‘University of Oxford’ in 26 countries including India, SAARC nations, Middle East and North Africa. Agreement is for 10 years, with auto renewal for 5 years and extendable 2044, based on milestone achievements. First agreement was entered on 1 October 2014 only for India and subsequently second one on 10 June 2016 for Middle East and North Africa. Due to commitment to quality and timely delivery, Oxford Limited extended rights to the existing range of stationary products by way of a comfort letter dated 10 March 2016 wherein Oxford has provided comfort to Vasa for renewal of the agreement dated 1 October 2014 for a period of twenty (20) years until December 31, 2044 subject to company achieving milestones as required under the license agreement. This extension of rights till 2044 enables Vasa to further strengthen relationship with Oxford and the brand. This should probably act as a testimony to Oxford’s confidence in Vasa.

* 26 countries: India, Bangladesh, Sri Lanka, Mauritius, Maldives, Nepal, Seychelles, Reunion (South Asia) Saudi Arabia, Kuwait, Qatar, Bahrain, UAE, Oman (Middle East) Egypt, Lebanon, Jordan, Yemen, Iraq, Libya, Tunisia, Algeria, Morocco, Kenya, Nigeria and Tanzania (North Africa). Basically SAARC nations including India, Middle East and North Africa.

* Why Vasa: Unique differentiator is their experience in stationery since 1970s to forecast demand accurately, understand pulse of consumers. Oxford choosing Vasa is a testimony of their experience and skill. Company spends a lot of time on market research, identifying new trends. Last two years, focus of the company has been in developing innovative product range under the brand of Oxford, entering into arrangements with distributors, tie-up with suppliers and recruiting a sales team. The promoter considers stationery business as FMCG without an expiry date.

* Vasta + Oxford: In addition to marketing and selling products under the ‘University of Oxford’ brand, company also intends to promote and market products under its in house brand ‘VASTA’. Company intends to utilize the existing channels for sourcing products and distribution networks for the ‘VASTA’ brand products so as to create a market for products under the in house brand as well. Growth of ‘VASTA’ brand products market shall provide an alternative range of products to the existing range of products sold under the ‘University of Oxford’ brand to the customer. Company intends to leverage the existing distribution platform and implement effective marketing strategies to deepen our reach in domestic markets for both brands, also ensuring that the same can be interchangeably used. Company also does trading in copier paper and uses this as an entry point to build relationships with distributors.

* Reason for IPOs: working capital related requirements - earlier company used to fulfill orders on made to order basis, but given the experience and expertise in stationery, they decided to now work on demand forecasting - working capital, inventory ready business model. Sellers attach a lot of importance to speedy delivery of products.

* Asset light: Company is only into processing and assembling of stationery. No manufacturing, completely asset light. Functions like a master distributor. Vasa has been sourcing stationary products for sales in domestic and overseas markets since the year 1994. It outsources manufacturing of stationery products to various suppliers based out of India, China, Indonesia and Malaysia which enable Company to adhere to the required specifications and stipulated quality standards for stationary products both under ‘University of Oxford’ as well as for ‘VASTA’.

* Strategy: Vasa Retail has a very focused business model. In India - Oxford and Vasta (own brand). Overseas (mainly Middle East) - Oxford, Vasta and existing business of functioning like aggregators (consolidation of various stationery products), private labels.

* Aggregators: Consolidation, acting like a one stop shop for all brands (Cello, Kangaroo, etc.) and all products based on demand. The trend in Middle East is that sellers like having private labels, so they get it manufactured and use their own branding to sell.

* Indian industry: Operating in India was extremely difficult prior to GST. Unorganised sector had an unfair advantage since there was large scale evasion of taxes. Duties were close to ~40%, which after GST net off all input credits is now ~10%. This has led to a large shift from unorganised to organised, with many unorganised players being unable to cope up. Significant part of the industry is still unorganised. Stationery industry in India is expected to grow at 5.9% CAGR 2017-2026 from USD1.5b in 2017 to USD2.5b in 2026, with a large shift happening from unorganised to organised. Pens form about 31% of the market, expected to grow from USD460m to USD750m over the same period, adding USD58.6m annually (5.6% CAGR). Mid-range stationery segment is expected to grow from USD718.1m to USD1249.8m over the same period (6.4% CAGR).

* Products: Stationery products (Further classify into (i) school and education products; (ii) fine art and hobby products; and (iii) office products) + paper pulp + bag fabric.

* Stationery products: Artistic materials, hobby colors, scholastic colors, scholastic stationery, office products, drawing instrument, writing instruments, office stationery, adhesives, notebooks, office supplies and writing instruments, books, pens, pencils, erasers, files, copier paper, bags and bottles.

* Paper pulp: Procuring paper pulp and selling the same to paper mills.

* Bag fabric: Procuring bag fabric and supplying it to the other bag manufacturers and also using the same for manufacturing our products (school and office bags). These stationery products are essentially used by school going children and offices as a part of their stationery requirements. On the other hand, paper pulp is the key raw material for the manufacturing of wide variety of paper. Bag fabric is not only supplied to other bag manufacturers but is also used by company for manufacturing its bag products.

* Product portfolio: Products portfolio comprises of a wide range of products which are sold under the brand “University of Oxford” as well as under “VASTA”. Products portfolio includes water colour cakes, water tubes, poster colours, wax crayons, oil pastels, plastic crayons, sketch pens, textured papers, silk laid papers, handmade papers, cards and envelopes, pearl finish papers, scales, sharpeners, colour pencils, erasers, engineering boxes, other technical instruments, note books, adhesive mechanical pencils, hi-polymer leads, fountain pen and its ink, water bottles, pencil cases, primary school bags college bag packs, secondary school bags, geometry boxes, canvas rolls, canvas boards, artist water colours, oil sketching pappers, drawing inks, brushes, painting mediums, glass colours fabric colours, powder colours, fabric glue, artist poster colous, white board markers, permanent markers, peal and seal envelop, diaries and computer labels, organizing divider, highlighters, ball pen, gel pens, stamp pads, refills, paint markers, CD markers, carbon papers, glue sticks, gum, copier paper, paper pulp, bag fabric etc.

* SKUs: Offers around 240 products of Oxford currently, to go to 1500 products in future.

* Huge runway for growth: Currently reached 750 outlets in Mumbai (7 distributors), there are close to 18,000 potential outlets. So as such have just scratched the surface. As of now, no where in modern retail. Modern retail presents a big big opportunity. There are 50,000+ modern retail outlets across India.

* What makes a brand successful: Success of a product depends on three factors equally - 1. Strong brand 2. Acceptability 3. Maintain price/affordability - Oxford would check all the boxes.

* Pricing strategy: Company plans to keep pricing at low or no premium for Oxford, for basic (economy) standard stationery. If a pen is for 10 rupees in the market of other brand, Oxford would sell the same at 10 or 12, since market perceives the value in such a way. Company plans to keep margins higher for unique/niche products, where the market doesn’t attach a specific value (or price cannot be perceived). Designer pouches, special oil pastels colours, highlighters etc.

* Revenue breakup: roughly 60% is stationery, 40% is paper pulp (copier paper). Bag fabric is very very marginal. The revenue mix would change towards higher margin stationery products.

* To sum up: strategy in India - sell Oxford and Vasta, more of Oxford actually. Strategy overseas - continue to be aggregators and sellers, sell Vasta and Oxford - convert gradually everything into Oxford. The Middle East private label business, has a potential to turning to Oxford for higher acceptability, margins, given affordability is not a concern. Vasta largely offers an economy level product. India as well, distribution built for Vasta and Oxford can be interchangeably used. Company also plans to gradually convert all Vasta products to Oxford.

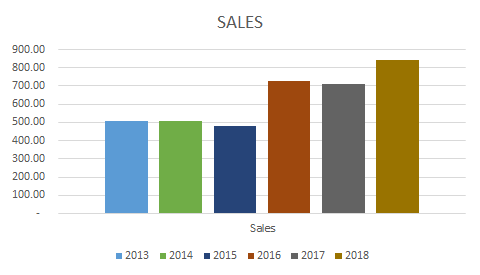

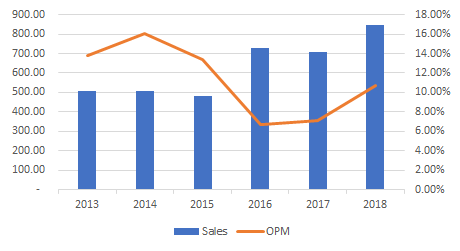

* Numbers: 1HFY18 (YTD October 2017) revenues 18cr, PBT 1.35cr and PAT 1cr. FY17 23.55cr, 1.23cr and 0.92cr. Debt - No term loans, all debt is largely working capital LCs, CCs, etc. No long term debts. Company would largely only require working capital loans.

* FY18 results analysis - Revenues of INR35cr and Profit after Tax (PAT) of INR1.42cr for FY18. Corresponding figures for FY17 - INR23.85cr and INR0.92cr. 46.57% YoY growth in Revenues and 54.34% YoY growth in PAT. EBITDA margins FY18 5.8% and FY17 5.5%. Hardly any long term debt (INR0.33cr) . everything is short term (INR9.36cr) which is rolling, used for working capital. Cash equivalents of INR1.18cr. While analysing, do note that company has recently shifted its business model to inventory based, demand forecasting from made to order. So a lot of IPO money (received only in February 2018, less than 90 days towards year ended March 2018) has gone into keeping stocks ready and ordering, etc. Hence the trade payables (INR9.75cr) and trade receivables (INR11.40cr) are high. Market cap INR22cr.

* My view: I would not want to comment on the valuations, but this definitely looks like a very high risk, unique, asset light, high return ratios play on the branded stationery business. Imo opinion, given the low base, company can easily achieve 30%+ growth YoY, for multiple years ahead.

Risks/Concerns

* Company still small in terms of revenues.

* Close to 40-50% of revenues at the moment of low margin trading paper copier business.

* Oxford and Vasta plans may or may not work out - business risk. A lot of success would depend on Oxford stationery sales and acceptability.

* Typical risks associated with SME companies - liquidity is low, lot size is high and others. Company stock price has had a wild swing from level of 30s to 70s and back to 30s, just to elucidate the kind of price risks SME carry.

All the above details have been taken from public material, largely their prospectus, website and investor presentation during IPO.

Disclaimer: This note is not a research report but assimilation of information available on public domain and it should not be treated as a research report, investment advice or Buy/Hold/Sell recommendation. I am not registered with SEBI under the (Research Analyst) Regulations 2014 and as per clarifications provided by SEBI: “Any person who makes recommendation or offers an opinion concerning securities or public offers only through public media is not required to obtain registration as research analyst under RA Regulations”. It is safe to assume that I might have the company in my portfolio and hence my point of view can be biased. Investors are advised to do their due diligence and consult a qualified financial advisor prior to taking any actual investment or trading decisions.

Disclosure: Invested

compared to others, I could not find much info elsewhere. From reading up on Avanti Feeds and Waterbase, I found the information credible and of OK quality. Rest I trust VPers to add

compared to others, I could not find much info elsewhere. From reading up on Avanti Feeds and Waterbase, I found the information credible and of OK quality. Rest I trust VPers to add