@Swapnil_gangele wrote:

Company Profile

Aarey Drugs & Pharmaceuticals Limited, promoted by the Ghatalia family, is engaged in active pharmaceutical ingredient (API)/Bulk Drugs manufacturing and offers a range of products for various industrial applications. The Company is engaged in trading and manufacturing activities. The Company is a manufacturer and supplier of pharmaceutical raw materials, chemicals, pharmaceutical ingredients, API's drugs, food colors and flavors. The Company's assortment of pharmaceutical products includes Metronidazole and Metronidazole Benzoate. Its products include Monomethyl Urea (MMU, Dimethyl Urea (DMU), Theobromine (THB), Theophylline (THP). Its other businesses include trading aromatics chemical, chemical acid, chlor alkalis, industrial alcohols, industrial ketones, glycols and glycol ethers, fiber intermediates, industrial amines, acetates and esters, chlorinated solvents, industrial intermediates and industrial chemicalsRecent Capacities

- Company has commenced manufacturing of Mono Methyl Urea & Di Methyl Urea (Dimethylurea is used for synthesis of caffeine, theophylline, pharmachemicals, textile aids, herbicides and others. In the textile processing industry dimethylurea is used as intermediate for the production of formaldehyde-free easy-care finishing agents for textiles) as decided in June 2016 . Company has further added new products i.e. Erithromycin Derivates (Erythromycin is an antibiotic used for the treatment of a number of bacterial infections. This includes respiratory tract infections, skin infections, chlamydia infections, pelvic inflammatory disease, and syphilis) Mafenamic Acid (Mefenamic acid is used for the short-term treatment of mild to moderate pain from various conditions. It is also used to decrease pain and blood loss from menstrual periods. Mefenamic acid is known as a nonsteroidal anti-inflammatory drug) with capacity of 10 m.t. & 25 m.t. respectively in June 2017

- New Upcoming Capacity/Product

Company will start production of new product i.e. Theophylline by March, 2019 Necessary steps has already taken by the management (Theophylline is used to treat lung diseases such as asthma and COPD (bronchitis, emphysema). It must be used regularly to prevent wheezing and shortness of breath. This medication belongs to a class of drugs known as xanthines)Industrial Overview

*Rising Healthcare Spend: Healthcare expenses rose to US$118 per head from US$76.1 per head and it is going to rise only with Govt focus on public healthcare

- Health Insurance: Rising disposable income and government initiative will flourish primary healthcare and disease management

- Indian Pharma Market to expand at a CAGR of 22.4% over 2019–22 to reach US$ 55 billion Indian Generic Market Growth at a CAGR of 16.3% over 2019-22E • India generic export accounts for 30% (by volume) and 10% (by value) in US generic Market • 304 ANDA approvals from USFDA in 2017

Promoters and QFI Interest

The company has alloted 10,00,000 Warrants Convertible into equal number of Equity Shares on preferential basis to Mr. Nimit R Ghatalia, Promoter vide its Extra Ordinary General meeting held on 1st February, 2018, and ii. The company has alloted 33,00,000 Equity shares on preferential basis vide its Extra Ordinary General meeting held on 1st February, 2018 to Qualified Institutional Buyers. Primary liquidity needs have been to finance working capital needs. To fund these, the company relied on internal accruals and borrowings

Note : These allotment made above Rs 50/share on avg shows confidence of promoter and QFIs and so offers lucrative bargain to novice Retail InvestorsPromoter are continuously accumulating since Dec-18 above INR 30/Share and so far bought 1,39,602 Shares from market.

Major Booster Ahead for Next 5Years

It is estimated that drugs worth US$40bn in US and US$25bn in Europe will be going off patent in next 5 years. This is expected to be the major export booster for the generics and API Industries based out of India.

Risk or Red Flags

Couldn’t be identified hence welcome if found by any fellow memberValuation

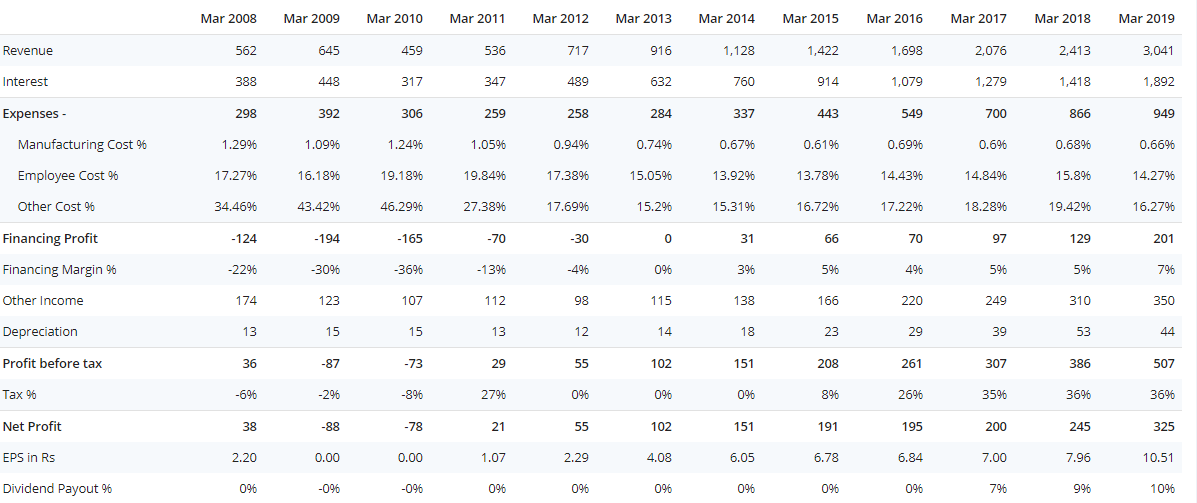

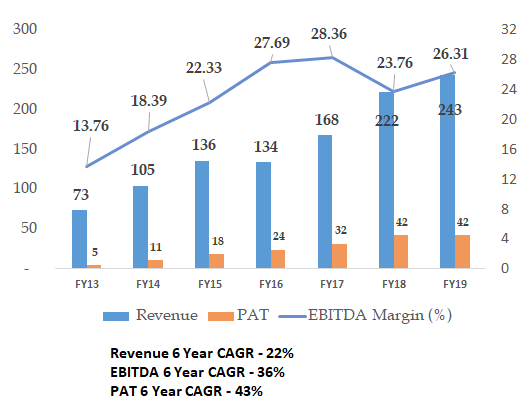

Topline is growing CAGR @ 15% for past 5 yrs and bottom line is expanding CAGR @56.42 %.

Present capacity utilization is below 60% means no major capex required for next 80 % volume expansion and looking at past growth rate this could be achieved in next 3 to 4 yrs which could reflect in the bottom line expansion of more than 200% from here, keeping present macros in mind. In figure terms that could easily translate in EPS of 10.34 Rs/ share 3-4 yrs down the line. At FY 2022-23 FPE of only 3 against avg industrial PE of above 29 this least leverage compounding business looks attractive.

Discl: Already Invested

Posts: 1

Participants: 1