Fredun Pharmaceuticals was started in the 90’s and was originally a contract manufacturing company , it has grown and come a long way and now contract manufacturing is only about 2% of the sales of the company which have frown at:

FINANCIALS

|10 Years:|37.73%|5 Years:|35.45%||3 Years:|31.93%||TTM:|39.54%|

Compounded Profit Growth

10 Years: 53.86%-5 Years: 79.40%-3 Years: 58.98%-TTM: -31.14%

the Product portfolio Anti-diabetic ingredients contribute 25% of its total sales, anti-cardiac 18%, NSAID 24% and others 33%

The company has expanded production capacity by 530% in last few years. It has been systematically investing in its productive infrastructure by installing additional granulation departments, high-speed tableting and blister packing machines. The current capacity utilisation is at 50% and it is projected to go up to 80% by mid-2020.

Read more at:

Risk Analysis qualitative and quantitative ( As far as my capability allows)

Getting at the numbers , the company looks interesting and reminds me a bit of caplinpoint Labs, its targeting non US markets like Vietnam, Thailand,Turkey,Shri Lanka, Tunisania,Myanamar,Malaysia ,Combodia,Phillipenes,Mauritus to name a few and a lot of countries within Africa.

So I’m looking into the fact that does India have a structural advantage in Pharma over these countries , be a labour cost , Know how , and where exactly in the value chain does the generic Pharma company in India separate itself from those in other countries. The fact that we are one of the biggest generic players globally we can assume that there is an innate competitive advantage we have, that being said the African Market looks like a very good opportunity gives the fact that Fredun is targeting niche markets with niche verticals and has a good mix of high volume and margin products ( I have a pet dog and taking him to the vet I noticed one of their products that if I recall have seen pretty often, its in their vet nary vertical) .

Coming to the numbers the market cap is 65cr and if I average out the cash from operating actives after working capital enough to maintain current sales level giving a no growth outlook, the cash yield (Operating profit-( maintenance working capital+mainiance capex-tax)) yield comes to about 6 cr, with the current market cap of 65cr the yield is about 6/65= 9.25 yield , so if we can look at it like a callable bond , its a company assuming it does not grow anymore and decides to start paying out the money it generates now its a 9.2% yield(assuming current status co), but if someone can help me dive deeper into it and answer the following questions maybe we can get a better idea about the probability oft he future growth and margins, so far the management seems to suggest a 20-30% cagr. If that comes true its like bond yielding 9% growing at 20% cagr, the downside seems very protected if the company can even maintain status quo and not grow, but the growth I feel if it comes can generate very good returns considering we are barely paying anything for growth .

The only key risk I see that may drive the current 9% yield is 1) if sales de grow and the company must still pay its fixed costs on the unutilised capacities 2) No pricing power in the situation raw material costs go up, though so far margins have mostly improved.

Answers to the below questions will be very welcome, but points made supported by evidence would be really helpful and not inferred opinions, I’m trying to get facts here so everyone can gauge and infer the data presented as they need to and then we can debate the rest.

If we can see what is the estimated market size in each of the verticals they operate in , in the respective countries they are present in and what are the local and other competitors in those markets.

There is not much information from the management perspective , but if we can try and see if there is a moat something that distinguishes them since its a semi commoditized space ( some verticals not all) and where in the value chain that is present, cheaper working capital, faster inventory turnover? Processing efficiency due to automaton , cheaper sourcing of raw material any other things pls feel free to write, though I’m a lone wolf , Pharma is not my best sector so I though of writing about Frendun here since it does remind me allot of caplin in its early days given the target market and seeing the larger picture , they have also developed some medicines for the Indian market and bidding for government tenders ,and the big health care push coming from the government that is another space they are already preparing themselves for. Saying all this if we can figure out the odds and what the likely hood of the growth going ahead could be a very rewarding , also they have enough capacity to do a top line of 230 cr without further need for capex , current revenue is about 120 cr ttm

Disclosure : No holdings yet, but tracking carefully.

Established by Mr. Madhusudan Bagla, a first generation entrepreneur, pioneered self-adhesive water based Carton Sealing Tape manufacturing in India when he set up Hindustan Adhesives Limited in 1988. Currently his son, Nakul Bagla(CFO) is the driving force behind the company

Company operate 3 plants in UP, Uttarakhand and Gujarat respectively and employs around 300 employees

Promoter & family owns around 70% stake in the company

Company is manufacturer of Acrylic Packaging Tapes which is suitable for all type of Carton Sealing applications. The product range includes various tapes like heavy-duty tape, tear tape, low noise tape, printed tape, coloured tapes, jumbo tapes, freezer tapes etc.

It also manufactures Polyolefin Shrink Film which is fully recyclable way of packing FMCG goods

It is catering big brands like Unilever, PepsiCo, Coca Cola, P&G, Reckitt Benckiser, Cadbury, Nestle, ITC, Amway, Colgate, Dabur etc. since a decade

Co. has over 500 total customers

Industry Scenario

BOPP Tape market size in India is estimated around Rs.100 crore/Month. This market is divided primarily into two parts – Organized sector and unorganized sector.

The organized sector contributes around 40% of the demand while the remaining demand is fulfilled by organized sector.

Growth Visibility

Company operated via 2 legacy manufacturing units in U.P and Uttarakhand each with combined capacity of 62 Million square meters and catered to the domestic market

In 2017 co. planned on expanding its adhesive tapes manufacturing capacity substantially by adding 216 Million square meter plant, taking total capacity to 278 Million square meter at total cost of 35 Crores

By April’18 the new plant(imported from Italy) was commissioned near Special Economic Zone (SEZ), Mundra (Gujarat). It is an Export Oriented Unit (EOU) and management aims to cater the export market via it

The plant was set up near port to mainly cater export markets as there was demand visibility and higher volume offtake in export business compared to smaller order size in domestic markets which it caters through older plants

Mundra plant is also vertically integrated as it manufactures Adhesive solution which gives stickiness to the tapes and corrugated boxes wherein the finished products are packed and shipped

Co. also set up one marketing unit in the US with branches in various parts of Europe under the name Bagla Films LLC for catering to foreign units of its Indian customers and subsequently new clients in foreign geographies

Co’s Realizations are around Rs.13-14/ square meter. At optimum utilization (85%), Co. has the potential to achieve top-line of around 300 Crore of topline without incremental investment vs the FY19 Sales of 140 Crores & 75 Crores in FY18

Financials:

Annual revenue was around 75 Crores until FY18 which was constituted- 50 Cr sales of adhesive tapes and 25 Crores sales from POF shrink films FY19 Could see clear growth in numbers wherein the top-line increased to 140 Crores due to commencement of the Mundra plant vs 75 Crores YoY

FY19 export sales stand at 77 crores vs 10 crores in FY18. Exports also fetch export incentive of around 3 crores in FY19

Currently debt stands at 53 Crores. The overall gearing remained stable to 1.29x as on March 31, 2019 as compared with 1.30x as on March 31, 2018

The operating cycle of the company improved to 59 days in FY19 vs 100 days.

The improvement in operating cycle is on account of improvement in collection period to 50 days in FY19 from 72 days in FY18 due to increase in export revenue. The improved collection period and more export demand led to improved inventory holding period to 58 days in FY19

Despite almost double top-line YoY, the OPM largely suffered mainly due to commencement of new plant at Mundra, Gujarat and FY19 being the first year of operations.

Volatility in EBITDA % suggests that company’s margins depends on the volatility in the RM prices- crude derived which needs to be monitored

Cumulatively past 10 year EBITDA is 100 Crores vs cumulative adjusted cashflows of 76 Crores which signifies that the reported profits is converted into cash and it is not only accrual based earnings

Weakness

Co. operates under single brand- Bagla group wherein they also operate their private entity- Bagla Polifilms Ltd which is involved in POFF Shrink film manufacturing.

However, their product profile is different from Hindustan Adhesives Ltd because proportion of POFF shrink film to top-line is around 18%

Raw-material susceptibility: As the core raw material are crude derive, any fluctuations in the crude affects the realizations of the co and impacts the profitability and EBITDA %

Valuations

Currently the stock is trading at lucrative forward valuations of 2.8x EV/EBITDA

If co. successfully ramps up the production from Mundra plant at optimum utilization, it could generate EBITDA of 30 Crores (300 Crores Topline * 10% OPM) whereas current market-cap is only 35 Crores

Sources: AGM, Website, Credit Reports.

Disclosure: Invested but no transaction since past 3 months

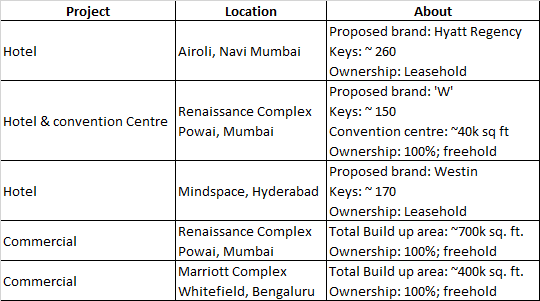

Hoteling company from the stable of K Raheja group, Chalet Hotels Limited (CHL) is an owner, developer and asset manager of high-end hotels in key metro cities in India.

Company has 6 hotels, 1 service apartment, 2 commercial projects and 2 retails projects spread across Mumbai, Pune, Bengaluru & Hyderabad.

Apart from the above, company has 2 residential projects at Madhapur (Hyderabad) and Koramangala (Bengaluru). The residential development project at Bengaluru is on hold as the matter is sub-judice before the Hon’ble Karnataka High Court on account of a dispute on the permissible height of the structure.

CHL have branding and operational tie-up with leading global hospitality chains having strong brand name. (JW Marriott, Westin, Marriott, Marriott Executive Apartments, Renaissance, Four Points by Sheraton and Novotel, which are held by Marriott Group and the Accor Group)

Company has entered into a memorandum of understanding with Marriott Hotels India Private Limited for rebranding w.e.f. April 1, 2020, of the existing hotel viz. Renaissance Mumbai Convention Centre Hotel as ‘Westin Mumbai Powai’.

Company is in the process of developing 3 additional hotels and 2 commercial office spaces. Below are the details:

Company has a subsidiary Chalet Hotels & Properties (Kerala) Pvt. Ltd. Although there is insignificant business in this subsidiary. (Not sure why this subsidiary was started.)

For securing the supply of renewable energy, Company has acquired 20.8% of the Equity Share Capital of Krishna Valley Power Private Limited and 26% of the Equity Share Capital of Sahyadri Renewable Energy Private Limited, being entities engaged in generation of hydro power. (Not sure how much saving does it really accrue and what is the impact on bottomline.)

Some of the down sides as presented in Q3 presentation:

Sluggish consumer spends

General economic slowdown

Lower banquet & MICE revenue (for CHL)

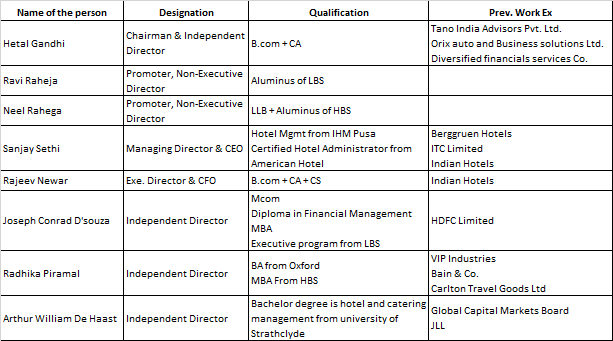

Board of Directors:

Financials:

ADR (Rs.)

FY18

FY19

FY20 9M

MMR

7629

8086

8149

Bengaluru

8620

8756

8995

Hyderabad

7896

8205

8547

Combined

7840

8218

8366

ADR represents revenue from room rentals at the hotel divided by total number of room nights.

Occupancy (%)

FY18

FY19

FY20 9M

MMR

73%

76%

75%

Bengaluru

75%

77%

76%

Hyderabad

72%

76%

74%

Combined

73%

76%

75%

Average occupancy represents the total number of room nights sold divided by the total number of room nights available.

RevPAR

FY18

FY19

FY20 9M

MMR

5543

6178

6075

Bengaluru

6447

6757

6846

Hyderabad

5694

6234

6301

Combined

5716

6283

6245

RevPAR is calculated by multiplying ADR and average occupancy available at the Hotels.

Total revenue mix is:

Total Income Mix

FY19

FY20 9M

Hospitality

88%

87%

Retail & Commercial

4%

10%

Others

8%

3%

Hospitality Revenue Mix is:

Hospitality Revenue Mix

FY19

FY20 9M

Room Revenue

58%

59%

Food & Beverage

33%

32%

Others

9%

9%

Financial:

Particular (Rs. Mn.)

FY18

FY19

FY20 9M

Total Income

8,513

10,348

7,714

EBIDTA

3,005

3,668

2,910

EBIDTA %

35.3%

35.5%

37.7%

PAT

-914

-84

569

Company’s D/E has improved from 5.5 (FY18) to 1.0 (FY19). It stands at 1.0 as on 31st Dec 19.

Reduction in debt is due to equity raising (IPO).

Similarly, Debt / EBIDTA also improved from 9.1 (FY18) to 4.1 (FY19). If we prorate 9 months FY20 EBIDTA to 12 months, this ratio further improves to 3.8.

Q-on-Q movement:

Particular (Rs. Mn.)

FY19 Q1

FY19 Q2

FY19 Q3

FY19 Q4

FY20 Q1

FY20 Q2

FY20 Q3

Total Income

2,456

2,572

2,549

2,771

2,462

2,405

2,847

PAT

-229

-126

141

130

137

101

331

PAT %

-9%

-5%

6%

5%

6%

4%

12%

EPS

-1.3

-0.7

0.8

0.8

0.7

0.5

1.6

FY20 Q3 has been exceptional quarter. Improvement in revenue is directly flowing into PAT. Largely the improvement is from Retail & office business. Q-o-Q there has been more store opening at The Orb and also the improvement at Inorbit Mall Bengaluru.

Particular (Rs. Mn.)

FY19 Q1

FY19 Q2

FY19 Q3

FY19 Q4

FY20 Q1

FY20 Q2

FY20 Q3

Hospitality

2170

2075

2326

2566

2198

2046

2500

Retail & office

65

105

130

91

152

307

281

For TTM EPS of Rs. 3.6, current price of Rs. 340 is trading at PE of 94.4.

Intro:

Diamines and Chemicals Ltd (DACL/Diamines) is a Vadodara-based based speciality chemical player and is the one of few manufacturers of ethyleneamines in India. The company enjoys barriers to entry based on technology and its long existence in the market. However, there are concerns on product concentration and limited visibility on long-term business growth. Though it seems well positioned to benefit from the upcoming growth opportunity.

Diamines can benefit from ethyleneamines’ growing domestic market, Diamines is one of few established player in the domestic ethyleneamines market and holds ~40% share in the domestic piperazine (a sub-segment of ethyleneamines) market. With the Indian ethyleneamines market expected to grow at ~8% CAGR in the next few years and piperazine likely to benefit from domestic pharma growth, Diamines is well positioned to tap this opportunity.

Discovery:

Looking at chemical players (due to continued move of business from China), found the Alkyl Amines to be a promising bet, the company shares the promoter group with DACL, but there was a re-organization of ownership and the concerns were split off about a year ago, with a non-compete agreement. Amit M Mehta, took exclusive control, by relinquishing share in Alkyl Amines.

My understanding is that the Ethyl Amines are higher margin and have better process moat than Methyl Amines. Found the growth trajectory having good momentum and valuation seemed reasonable. The margins have recently become 4x compared to the 2013-2016 period. The company was in focus in 2011 but did not deliver on promised growth, it is a small player and can get crushed by imports by big players, which seems to have occurred then.

Main use of commodity products of the company seem to be deployed in Pharma and the competition seems to be mainly from China.

More details:

AR 2019 page#26 seems to show the company can be challenged due to over-supply, but it seems to have managed quite well since then and the reason might be deploying the unused capacity (of EDC) to make new sets of chemicals in demand. This EDC tech was cutting edge in 2011 but is obsolete now.

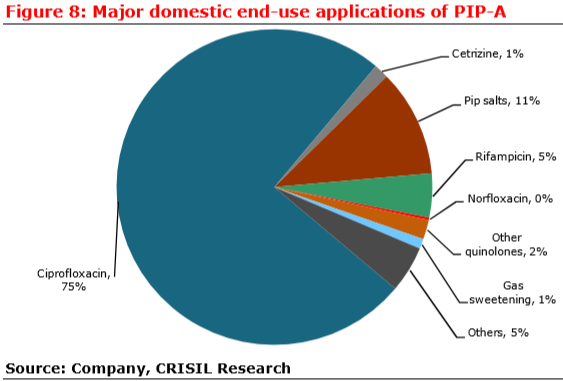

PIP-A is mainly used by Pharma to manufacture Ciprofloxacin. EDA etc. used mainly for Fungicides, and its derivative EDTA in Pharma as chelating agent.

As per CRISIL the company seems to have a very restricted USP due to small size and lack of import restrictions, this may rapidly change if Atma-Nirbhar bharat special focus on Pharma and intermediates really takes off. But something seems to have changed structurally since 2016 to kick the company on a strong performance uptrend.

Hello everyone , hope you are fine and in good health

this is my first post in VP. Over the years i have learnt a lot from this forum as well another kinda predecessor forum (he now runs a famous pms ) and peter lynch .

Before i read these forums and peter lynch i actually knew nothing . i would watch tv and buy stocks based on what i saw on business channels , i was that kinda ignoramus

So finally decided to stop mooching off vp(just reading the stock posts ) and actually contribute

so here goes

There are safe no tension bluechip fmcg stocks, they are fast growing midcaps ,exciting smallcaps and then there are the ignored longshots. These undiscovered stocks generally have the right fundamentals in place but for some reason are ignored by the markets for extended periods of time (years and years )

The beauty of these longshots is that when they work out , the stock performance is often way higher than what we investors originally anticipated and will produce extremely pleasing results making us look like a genius. But the problem is we would have sold it off by then due to exhaustion

An example of such an opportunity for me was bombay burmah trading corp many years ago (i had accumulated a sizable position , got sick and tired of waiting and finally sold off at minor profit and then the stock went up more than 10 times

And so i have learnt to be more patient.

Company - Majestic Auto

MARKET CAP - 85 CRORES ( from moneycontrol) as on 14.6.20

CMP - RS 81.7 (listed only on bse )

Promoter holding - 75%

PLEDGING - NO Pledging

Consolidated BV - RS 385.64

Cons Price /book value - 0.21

Consolidated net debt - 171 crore (i have added up long term and short term debt and subtracted them from the current investments ,cash balances and other bank balances, i am ignoring things like other current assets)

Investments - 921000 shares of hero motocorp (as per 2019 annual report)

worth 221 crores as of today

Majestic auto is a part of Mahesh Munjal group (Family of Hero group)

The company which was originally an auto component co has discontinued its automotive components business in 2017-18 and has now transitioned into Leasing of office space and facility management of the office space it currently owns.

The business has 4 parts

a) Leasing business

the company has a subsidiary emirates technologies pvt ltd which owns office space of

6 lac odd(0.6 million) square feet in a building called Majestic knowledge boulvevard located at sector 62 in Noida city.

it has marquee clients like tech mahindra and ericcson (do correct me if i am wrong ).

has 93% occupancy as per the latest annual report (18-19).

this property/company was acquired for 73.2 crore in 2015… Majestic auto acquired 80 percent of emirates technologies pvt ltd while the rest of the 20% was acquired by Group company OK Hosiery Mills .(its a related party). mahesh munjal and renuka munjal are directors in ok hosiery mills private ltd.

we need to study this related party angle a bit more.Future growth can come from acquisition of new commercial properties.

if the link doesnt open search for cnbc majestic auto

in this january 2018 video where the promoter mentions annual rent of 32 crores plus some more income from the facility mgmt . Also mentions that they hold 10 lac(1 million shares) of hero motorcorp.

the news anchor is guessing the property could be worth around 500 to 600 crores .

its also a positive in my opinion that the promoter is not tom toming the company and in infact downplaying the assets that the company holds .

Rental revenue generated has been 29.89 crores until 9 months ended december 2019.

Rental Profit before tax generated has been 18.91 until 9 months ended december 2019(decreased by 65 lacs approx as compared to previous 9 months ).

Rental revenue has increased by 3 crores as compared to previous 9 months ended december 2018

b) Real estate mgmt/Facility Mgmt business

Majestic it services ltd is a subsidiary which is into managing the properties acquired by majestic auto. It manages the planning and mgmt of majestic knowledge boulevard as well as things like

catering, cleaning, , HR, accounting, hospitality.etc

future growth can come from the facility mgmt division taking up other clients besides its parent.

Revenure generated for 9 months ended is 26.76 crore . PBT for 9 months has been 10.96 crores

These figures have reduced by half from the preceding year. .Last year there was additional income from sale of land which is not present this year.

If any of the boarders find other reasons for the revenue drop other than land sale , do give your opinion.

c) Land

the company has shut down its manufacturing locations and is selling the land little by little.

from the annual report 2018- 2019.

“Accordingly Land and Building amounting to 6,414.61 lakhs which was earlier part of Fixed Assets has been re-classified as inventory held for sale. A disclosure in the quarterly results to BSE has also been made to such effect in the Financial statements filed for the quarter ended June 2018 (dated 10 August 2018). A part of such Land and Building valued at 1,407.68 lakhs which has

been re-classified as inventory was sold for ` 5,765.24 lakhs during

the year having a significant impact on revenue and profitability of

the Company”

from the above i understand a portion of the land was sold in financial year 2018 -19 for 57.65 crore

which was valued only at 14.07 crores in balance sheet.

so there is a chance that the rest of 50.06 crore worth of land (as per inventory) can be sold for a substantial sum in the future.But i am not using this aspect for my valuation.

I am yet to understand how much more land is actually available for sale.

and whether this spare land will be sold or used to develop newer real estate to rent out.

The land is probably at the old business location which i think is ludhiana. (again not sure)

9 months ended december 2019 there has been no land sale till now.

d) Investments

The company holds 921000 shares of hero motocorp(latest annual report ) worth 221 crores of today. i dont think any of these shares have been sold till 9 months ending december 2019.

In the above video link it was mentioned as a million shares (10 lac) . in 2017 annual report shares of hero moto corp are at 10.3 lacs which is now 9.21 lacs so the company is definitely not averse to sell the shares.

if i take into account the value of hero shares held then the company has zero debt and a cash surplus of 50 crores as of today

MANAGEMENT

Mgmt compensation seems okay(vp boarders correct me if am wrong )

Both son and daughter of promoter are part of mgmt

Promoter has lent some money to the company and has received an interest of 3.73 lac. for 6 month ending september 2019

Promoter group company OK HOSIERY mills pvt ltd which holds 20% of emirates technologies which inturn owns the it park has been paid 31 lacs by the company as rent for 6 months ended 2019

source - bse disclosure

Future

i feel the cushion of hero motocorp shares might help the company raise more debt to buyout commercial real estate cheaper in the future (covid might change things a lot)

Alternatively company might sell hero motocorp shares as the market recovers and clear off all its debt and be a cash surplus company with a fixed income comprising of rental &others (slowly rising ) every year.

Pros

a company with a promoter holding of 75% , no pledging , rental revenue of around 35 crores from a commercial asset worth (well help me out here ) having zero debt and

effectively with a cash surplus of 50 crores considering hero motocorp shares

is available is at a marketcap of 85 crore. Net Net we are getting this company for 35 crore market cap (almost equal to one year rental revenue) and a price to book of 0.21.

Famous investors hold chunks of the public holding.

ANIL Kumar Goel holds 2 lac shares (0.2 million) which is 1.92 % of the company as on march 31st 2020

Nishit parekh holds 1.44 % of the company

varsha parekh holds 1.16 % of the company

dipak kanyalal shah holds 1.49 % of the company

other triggers like additional income from land sale and hero moto shares sale.

company has been reducing consolidated borrowings

reduced from 207 crore to 187 crore half year ended September 2019 as compared to previous half year.

Debt has been coming down consistently over the past three years

Abhishek basumalick presented this company at the 2019 chintan baithak. link shows his slide on majestic auto.

if a senior vp boarder is interested then its definitely a plus point

Negatives

stock is listed only on bse . its in the x group and you have to take compulsory delivery .

As mentioned in the beginning its an undiscovered and ignored stock and when i say ignored i mean it literally.

Liquidity is really really low . the whole market starts trading at 9 15 am everyday and this stock slowly wakes up with a yawn at around 11 am and then there will be a transaction of shares in single digit volumes

The lack of liquidity would be actually be funny if i was not invested

Volumes are very low most days with less than 5k shares traded often.

the problem with ignored stocks is that they wont move up for years but will crash a lot in a situation like covid. So such stocks can have a lot of price damage as i learnt recently seen in march just because nobody is bothered to buy.

and when such crashes happen i often question myself as to why do i even bother to be a so called value hunter ,instead just go with the herd and buy fmcg stocks and chill in life. So these ignored stocks are definitely high risk and can be a scary roller coaster ride.

there are related party transactions which i have to study and 20% of the material subsidiary is owned the by a group company.

and we dont know how things will pan out in the future with respect to covid. Mgmt communication is very limited.

Conclusion

This is my first post , so seniors do correct me if i am out of line somewhere.

i believe majestic auto is an highly undervalued stock and deserves to be re rated.

Discosure : i am invested in it …

vp boarders do help us all in finding what i am missing . why is the company trading at such a low valuation.

Comments and especially criticisms are welcome . i would love to know the red flags that i have ignored.

Please take my opinions with a sackful of salt

cheers !!

Disclaimer : This is not investment advice and should in now way be construed as one . I am not a registered sebi investment advisor. Please do your due diligence before investing.

Total Transport is listed in NSE Emerge SME platform. Total Transport Systems came with an IPO on July 25, 2017. It offered 3.78 million shares at fixed price of Rs 45 per share of face value of Rs 10 each. Their core business is - Less than a container load (LCL) and cargo consolidation. Most

of the shipping carriers carry their loads on containers, which needs to be full for maximum

efficiency. For export and import (Exim) players who don’t require a big full container, LCL logistics companies provide the best and most cost efficient solution.

Total Transport offers this together with freight forwarding that includes arranging all pre-

shipment activities like export inspection, excise inspection, container survey, cargo pickup

and Cargo Stuffing. Moreover, they offer consolidation for exports and deconsolidation for

imports.

It was incorporated in 1995 by Mr. Makarand Pradhan Prabhakar, Mr. Sanjiv Arvind Potnis

and Late Mr. Prashant Ramkrishna Salvi.

The core business services are provided to customers in two ways:

Booking – The customer books his cargo through us but transportation, custom

clearance etc provided by his designated CHA or custom Broker. They receive the

cargo, consolidate it in container and ship it to destination.

Complete Logistics Solutions – The customer books his cargo and all services

including transportation, custom clearance, consolidation, forwarding etc is done by

them till the point of destination.

Core Business Operations is divided into four parts:

Sea Freight Forwarding

Consolidation & Deconsolidation of cargo

Air Freight Logistic

Warehousing& Transportation

They have branches located in various cities in India like C.B.D. Belapur, Pune, Ahmedabad,

Vadodara, Kolkata, Chennai, Tuticorin, Bengaluru, Kochi and Gandhidham.

They have tie-ups with various shipping lineslike Maersk, MSC, NYK, Hapag Lloyd, Hyundai,

CMA –CGM, Cosco etc.to move their consolidated cargo on time. They are also members

of FIATA i.e. International Federation of Freight Forwarding Association, Bombay Overseas

Freight Brokers Association and Federation of Freight Forwarder’s Associations in India,

Consolidators Association of India and AMTOI. They have also established a wholly owned

subsidiary in Nepal through a joint venture.

Now what makes it a big emerging story-

In last few years, they have entered into two fast growing businesses of B2B E-Commerce

and Last Mile Delivery for big boys of B2C e-commerce players in India.

They have entered in a JV with a big conglomerate to develop and sell the global supply chain product for the Indian market and also to develop, handle, sell and manage the global brand name “SEEDER”

locally in India.

Seedeer is a global supply chain platform built by Eurasia Group.

Founded in 1982, Eurasia Group is currently headquartered in Shanghai with a total

of 2,000 employees and a storage area of 405,000 square meters. With 74 branches

in 34 countries and regions around the world, and nearly 40 years of accumulation, it has

built a comprehensive online and offline networks around the world.

With 35- year of experience as a leading global service provider, Seedeer has resources in

Air Freight, Sea Freight, Warehousing and E-Commerce which offers buyers and vendors

overseas warehousing, international direct lines, transfer shipment and FBA first miles.

Seedeer has successfully done API connection with global supply chain platforms such as

Amazon, eBay, AliExpress, Mercado Libre etc.

Seedeer in India -

Seedeer has not developed any B2B E-commerce website in any country where it is

present, not even in China. It has been working with big e-commerce players worldwide.

Looking at the potential of Indian market, Seedeer has plans to launch its own dedicated

B2B commercial website which will help Indian customers to directly source the material

from China and other countries worldwide.

Web URL for portal in prelaunch:

A company which has clocked 5800Cr topline in China is not coming to India to do a business of 100-500Cr. Launching a full fledge B2B e-Commerce

platform having more than 30 Lacs products is not an outcome of short term thinking.

This platform is the first platform of its own kind in India which will empower Indian customer to arrange doorstep delivery of 30 Lacs Products from worldwide locations without getting involved in custom clearances and duties etc.

‘Last mile delivery’ in ecommerce parlance refers to the last leg of a shipment’s movement

before it reaches consignee’s address or the final destination. The ‘last mile’ for an ecommerce company is ‘the moment that matters’. This last phase of delivery is referred to as the ‘lock in’ period for the customer. For an ecommerce company appointing a logistics unit is indeed a difficult task. In fact, appointing a logistics unit implies outsourcing of deliveries. Here two factors are involved, safety and punctuality. Though Retail Company takes the responsibility of packing material, the safety of the item during transit lies entirely with the logistics company. Further, the

possibility of delayed or wrong deliveries cannot be ruled out. These are few factors which forces an e-commerce company to choose the last mile

delivery partner extremely carefully. The relations once built between e-commerce Company and last mile delivery partner, last for long time.

One World Logistics, which is the subsidiary company of total transport has built such

rapport with Amazon. They are getting repeated business from both big boy of B2C E-Commerce player in India.

Why Last Mile Delivery Business may prove to be a game changer?

Competitive Advantage

E-Commerce companies select the last mile delivery partner after performing a lot

of quality checks. The business transactions with Amazon and Flipkart itself proves

that new World Logistics is not the new kid on the block

Setting up last mile logistics network is not an easy task. It takes years to establish

the channels and establish the image.

The last mile delivery network is largely dependent on the technology platform app

which is used by the delivery agents. One World Logistics has successfully built the

technical platform to perform the seamless business for big ecommerce players in

India.

Huge Valuation Gap between OneWorld and its Peers -

Rivigo is valued at approx. 8500Cr in the latest funding round. In FY 19, revenue for the

company grew by 42 percent to Rs 1,028 crore, even as its losses doubled to Rs 600 crore.

Rivigo does approx. 1 Crore last mile delivery per month. One World Logistics is all set to

to 10 Lacs delivery in by June-July this year. Though it is not possible to do apple to apple comparison of One World Logistics with Rivigo network, but giving 50% weightage to last mile delivery business in Rivigo and calculating on business volumes of OneWorld (which is 1/10th of Rivigo), the valuation of One World alone comes around 450Cr. Even after giving 50% discount on this assuming Rivigo is a big name as compared to OneWorld, the valuation of One World comes out to be 250cr which is still ~4 times bigger than current market cap of Total transport.

Possibility of buyout by Amazon -

Amazon has been consolidating its logistics landscape and been buying the assets in USA.

In 2019, Amazon has been making investments in potential solutions for last-mile delivery,

as well as expanding its Prime Air network, buying more planes and developing its airport

hubs.

Amazon has made several investments in last-mile delivery recently.

It started testing Scout, a robot about the size of a cooler, to deliver packages

autonomously in a suburb north of Seattle.

It participated in a venture capital round to fund Aurora Innovation, an

autonomous-vehicle company.

It’s also in talks to invest in Rivian, an electric-vehicle company.

Listing of One World -

If Total Transport promoter may want to list One World Logistics as a separate entity after

3-4 years. That will unlock huge value for investors.

I strongly believe that the One World Logistics may be valued at a hefty valuations whenever they need funding to expand their tech platform. A similar level of funding which happened in Rivigo is possible.

There will be huge value unlocking if amazon buys out whole business of One World Logistics OR if it gets listed as separate entity.

Total Transport company has approved migration to mainboard and has filed an application with SEBI. I am continuously in contact with Company Secretary Bhavik Trivedi through email. Any update I get will post here.

Cons : Corona has caused temporary delay in the all good factors and also affected its business as it in logistics sector.

Me and my friends have done above research on this company. This is not solely my research. It’s a combined effort.

Hi All - I have recently joined VP and glad to be part of this family. I have been in the stock market for the last 10yrs and love to analyze companies fundamentally and specialize in value investing.

I am here to share my analysis and hopefully hoping to get guidance from experienced members to have healthy discussions and debate on stocks.

My USP is my analysis is I have my own models to value stocks and I have shown details of those in the " Valuation as per different methods:" in the blog. This is not available in any research reports and I have used my last 10yrs experience to modify these formulas and models to come up with a quantitative way of showing upside. I usually only make an investment when I see a decent upside so I would love you to get your feedback.

After spending time analyzing the market and selling my recent holding on GHCL at a decent profit, I have recently made an investment in the J Kumar Infra project. I want to share mine below analysis.

History

1980: Started Business

2008: Listed on NSE and BSE

2012: Awarded with DMRC Project worth Rs. 14,072 MN & UPRNNL Project of Rs. 5,190 MN

2015: Awarded with Ahmedabad Metro Project worth Rs. 2,781 MN and Fund raised through QIP of Rs. 4,093 MN

2016: Awarded With Mumbai Metro Projects worth Rs. 67,174 MN

Segments:

Transportation Engineering i.e Metro rail, flyover, Airport runways, etc.

Civil Construction: Hospital cum Medical college, Railway terminal and Stations, Sports complex, etc

Irrigations: Dams, Canals, etc

Piling: Insitute cast, Precast Piling, etc.

Promoter Holding

Promoter holding has been at 45.32% in March-20

Promoter has kept increasing their holding over the last two quarters. Sep-19 Quater was 44.13% while Dec-19 was 44.66% before they increased to 45.32% as of March-20

Promoters’ latest purchase was on 25th March when the price was ~75 where they purchased 0.4% of the shareholding from the open market.

The promoter holding is 23% pledged which is a slight concern but when comparing other companies in this sector this has been a normal trend like incase of Dilip Buildcon and IRB Infrastructure which was a similar pledged percentage.

Order Book

It has an order book close to 11,500cr vs its annual revenue of 3000cr thus almost ~4 times its annual revenue

The Company has already won orders worth Rs 430Cr with ordering activity to pick up largely 1QFY21 onwards.

Please note that Maharashtra accounts for over 70% of JKIL’s order book which exposes it political risks while the Transportation segment accounts for 90% of the order book.

Financials

Financial performance has been quite good. It has increased it sales every yeat at a decent rate and its expected to overall report 10% higher sales as compared to 2019

Net profit like Prior years is expected to be up. The company will have COVID impact to take care of however I believe it should be fine given the strong sales and operating performance of the company.

The company has been able to generate decent cash flow from operation every year and also using this to pay dividends.

(Refer to the blog for the Financials summary)

The company has been a consistent dividend payer and has paid a dividend of Rs 17 in the last 10yrs. Given the Price of stock at 87, it’s trading at an attractive dividend yield of 2.6%

(Refer to the blog for picture)

iquidity

With COVID lockdowns esp on impacted sectors like real estates, airlines, etc, its important to invest in a company where D/E is low while also an entity that has demonstrated good ability to internally generate cash profit to service its obligations.

Among all the peers it has the lowest D/E and yet one of the lowest P/E and good historical growth

In terms of the [Cash conversion cycle]( Given the link of this in case someone wants to learn of this matrix), Cash flow from the operation, the low debt it does stand out, and points enough liquidity in hand. CCC has improved massively from 216 days in FY17 to just 131days in FY 20E.

Valuation as per different methods: : Refer to the blog

You might argue that why not IRB Infra . Well as mentioned earlier that in this industry where Project periods are quite long and esp during COVID times, it’s important for a company to have low D/E than ever before

This has the lowest D/E in the sector and trading at 0.36 P/B times just.

Risk:

Last year SEBI probed JK Infrastructure that it might have fabricated the financials but after detailed problem management and the company was cleared. Although they were cleared, such news always pose risk when it comes to corporate governance.

The high concentration of order book in Maharashtra and Construction sectors make it’s vulnerable to the political and sector-specific risk

High gestation of the construction segment always make things tricky esp due to COVID-19 when it comes to cost control and project execution on time to avoid cancellation and penalty.

The company has got high Capex planned which can impact its “free” cash flow although I believe in spite of COVID, its “operating” cash flow will be positive.

Overall its a company with good historical growth, the strong order book of 3.5 times its current Annual sales, Lowest D/E in the Industry, trading at all-time low P/E, and good dividend payment history.

I have invested in this at the current market price of 86 for long term purposes given the above.

Disclosure:

I have an investment in this stock so my views might be biased. I request you to take your own judgment call before you make any investment in this name.

I am not a SEBI registered analysis so don’t have any recommendation service/Paid service. It’s an educational website that is just meant to share the analysis I do before I invest.

#WELSPUNCORP

Starting a new thread since there was no thread for the Said company. These notes are not mine sharing only for educational discussion :

Crude from a high of $60 in Jan, 20 crashed to $20 in May, 20. As a result, Welspun Corp lost 40% of its FY20 order book.

However the company still has 8-9 months of #revenue visibility and can easily service its #fixedcost & employee expenses for FY21.

In the last month, crude oil has recovered around 50% from the bottom, as a result Welspun Corp won 90KMT #order in its US facility last week indicating normalcy once global trade & economy resets.

However, feel Welspun Corp’s strong cash & investment position in the #balancesheet and very low #longtermdebt will help the company withstand the current turmoil and bounce back stronger.

Interesting Case Study- #MohnishPabrai - effective way of buying distressed companies in bad times, buys at what he calls PE ratios of 1. He looks at unfavourable industries, (car industry in 2012) finds companies that will not go bust & have potential to deliver high earnings

For example, in 2012, he was buying Fiat-Chrysler (FCAU) at an average price of $4. The current EPS is $2.22. If we deduct 40% of the 2012 purchase price as the value gotten from Ferrari, we get to a PE ratio close to 1.

#WelCorp#Valuations- WelCorp is at distressed valuations and won’t go bust. On a steady state and normalized environment post COVID19, the company can do a 1000 cr EBIDTA in FY22 against an EV of 1,600 cr. At an #EVEBIDTA of 1.6 times, Welspun Corp at CMP is priced to extinction

Strong Financials & ability to withstand loss of revenues in FY21- As of Q3FY20, Cash & Cash Equivalent in the balance stands at 920 cr. Welspun Corp has a #debt to equity below 0.5 times, absolute number of debt is around 1,000 cr.

Biggest #COVID19 casualty

Post Jan2020, the #crudeoil prices collapsed 60-70%. The company has major dependence on global oil & gas players for its order book. https://t.co/M4Kgek399p

#Interestcoverageratio for FY20 would be around at 5 times (approx.) which provides huge comfort towards the management’s ability to service the debt. Last 5 years average #CashFlow from Operations is around 600 cr

#ManagementQuality- Zero Pledge by promoters, Consistent dividend payout for last 10 years, No cross holdings in other group companies.

#CashFlow from Operations- Last 10 years, accumulated CFO at 6,000 cr and current market price is at 10years low.

#ROCE- Return on Capital Employed for FY20 at 25% (approx.), vs FY17 at 6.5% indicating a clear turnaround in operations.

Cheap #Valuations - Welspun Corp at FY22 is valued at 1.6 times EV/EBIDTA is giving the company a shutdown valuations.

Therefore, the management of the company took the strategic decision to divest plate and coil mill division & the 43 MW power division.The sale of assets will result in the cashinflow of Rs. 900 crore which will help the mgmt to reach its target of zero netdebt by the end of FY20

Prudent #ManagementStrategies during PreCOVID19 era led to significant turnaround

Turnaround in Saudi’s Joint Venture’s Operations

The Company has a JV in Saudi Arabia. The loss making operations from this geography was weighing down on the bottom line of the company till FY19

However, due to bidding discipline and margin focused orders, the Saudi division witnessed a turnaround from Q4 FY 2019 and it posted positive #operatingprofits. The share #SAUDIJV increased from a loss of Rs. 60 crore in H1FY19 to a operating profit of Rs. 75 crore in H1FY20.

However, due to COVID19 impact on businesses, this decision has been deferred to March, 21 and so far only 20 cr has been received by the management. But the management’s intent focus towards asset light model & focus on core business is clear.

Company Overview

The company is engaged in manufacturing of welded line pipes and has a diversified product portfolio which includes #HSAW line pipes, #LSAW line #pipes, and #ERW/#HFIW line pipes. It is one of the largest players in the global line pipe business

#CrudeOil bounce - However, #brentcrude bounced 40% from lows due to which company recently won projects worth 102KMT, out of which 90KMT is from US.

Focus on Core Business

The management had planned to make the business model of the company into #assetlight model. They identified some assets which were weighing the capital employed, but were not contributing to the company’s profits.

The group has maintained relationships with reputed overseas customers, which include Saudi Aramco, TOTAL, Qatar Petroleum, Exxon Mobil and Kuwait Oil Company. It also supplies line pipes to all major players in domestic market, such as BPCL, IOC, GAIL, RIL, GSPL, and L&T.

#CurrentOutlook

#Orderbook as of Q3FY20 was 1,305KMT. Oil & Gas players globally being main clients, Post COVID19 company lost 40% (approx.) of its order book. Current order book stands at 765KMT valued at 6,200 cr giving the company #revenuevisibility for atleast 8-9 months.

Disclosure : Invested from lower levels. Please, do not take this as an investment advice. Do your own due diligence before taking any discussion. Notes are not mine and credit will be given to said writer. Posted only for discussion and educational purposes.

New member here and also just getting started with investing. Was waiting for a downturn for a while and was mostly invested in debt till now. Slowly converting the debt to equity positions. Also considering levering up a bit eventually if the situations gets really bad.

I look at the intrinsic value of all companies with 3 formulas ; Grahams formula which uses EPS, buffets formula that uses book value/book value growth and then DCF method.

If all 3 look great, I start buying. I do look for low PE ratios, less than 1 PB ration, low debt, good management, earnings growth over the last 5 years and good ROE

Here is my portfolio

Have been slowly buying Sterlite Technologies and Take solutions.

Sterlite : Optical fibre is going to be a mainstay over the new few decades as data consumptions increases. Being one of the few pure full stack solutions for networking, it seems like a steal at current prices. Especially as they are also focused on IP and promoter has given up pledged shares. Debt is a bit high but they have been decreasing it quite a bit and ROE is very high.

Take Solutions : Have been growing order book really quickly. MD seems very smart and also very synergistic acquisitions. They are one of the few CRO’s from India and I feel as lifesciences expands and more of the work is outsourced Take can be a huge beneficiary. Started building a position last week but will continue over the next few weeks.

Considering - need to review management and business but the numbers look great for the below list :

Elnet technologies

Gujarat Industries Power Limited

Was considering Graphite India, seems like a steal but then seems like China is dumping Graphite in markets so that could affect demand and thats already been reflected in 2020 results

Would love suggestions and criticism if you guys think there are huge red flags in my portfolio

Gujarat Themis Biosyn Limited (GTBL), located at Vapi, Gujarat, was incorporated in 1981 as a joint sector company with GIIC Ltd. and Chemosyn Ltd. (possibly NCL, Pune helped) commencing production in August, 1985 by producing Erythromycin and Erythromycin salts and formulations. The company was subsequently taken over in June 1991 by the Yuhan Group (one of the biggest South Korean pharma cos) and Pharmaceutical Business Group (India) Ltd. (PBG); a unique consortium of five competing drug companies - Themis Medicare Ltd (TML), Kopran Ltd., Anant & Co., Cadila Health Care Ltd. (Zydus) and Lyka Labs Ltd. It is being actively managed by Themis Medicare Ltd. (JV Company of Gedeon Richter Ltd, Hungary) since 2007. The company manufactures active pharmaceutical ingredients on job work basis for Lupin Ltd.

The latest results show that the company has re-classified its business from contract manufacturing to bulk drug seller.

Collectively 3 promotor groups (Themis, Yuhan and PBG) own 75% distributed equally, the rest is public. Somehow they are the only manufacturers of Rifampicin in India. Overall seem to have large fermentation facilities to make such drugs. Now they have added anti-cholesterol Lovastatin to this.

Discovery:

I got this investment idea from @kdjolly who had posted once on valuepickr an analysis of the company. The product is used in TB multi-drug combination therapy so market is big and growing, till some new science changes the treatment.

The technology is from Korean company which has also invested in it, 25% stake. The idea is that they may replace China (whose imports may have caused the problems for this co) as source of more anti-biotics and have started looking beyond Lupin, another investor and collaborator/buyer. CAGR is quite uneven, company had early turnaround from BIFR in FY2016 technically but only acknowledged in FY2018 AR. Now it appears that it is able to deploy a strong growth strategy. How much momentum can be sustained is difficult to say, I cannot find much details on this, hence, took a small position in overall PF.

More details: :

AR 2019 has very less interesting disclosures.

Gujarat Themis, went into BIFR in 2008 under the impact of consistent losses and debt. Under the scheme of re-habilitation a lot of operating and functional changes were brought in the company. The Face Value of each share of the Company was reduced from Rs.10 to Rs. 5 and the reduction in the value of equity shares was utilized to write-off a part of accumulated losses of the Company . Themis Medicare Ltd. was inducted as co-promoter of the Company and issued 2928702 shares of FV rs 5 at 10rs each. The induction of Themis as a co-promoter brought in the much needed sting and zeal in the operations of the company. The new promoters also brought in the sole long term customer in Lupin . Lupin’s deal with GTBL changed the fortunes of the company. The contours of this deal were very lucrative for GTBL. GTBL entered into a contract with lupin to supply Rifa (with the technology know-how brought in with another co-promoter – Yuhan Corporation). Lupin gave GTBL interest-free loan for capex that was required to finish the contract. This loan from Lupin was a returnable non-interest bearing loan and was repayable against 50% of the “Conversion Charges” for each invoice raised. So, this deal was beneficial to GTBL in more than one ways. Needless, to say this contract brought in very good topline and bottomline for the company.

To the credit of GTBL, with each passing quarter the company has been improving its operating efficiency and it now has one of the best operating parameters in the industry. With announcement of the supply agreement with Lupin that started from 1st April 2015 – Mar 2018 the company got solid visibility to its earnings. This had a very positive impact on the fiscal position of the company. Since the company came out of BIFR, the company will expand to newer products. Additionally, the company is also exploring the possibility of “offshoring” some of the manufacturing of its another promoter, Yuhan Corporation. Given the already established operational efficiency of the company any increase in revenue would significantly add to the bottomline too and the company is expected to clock significant revenue and profit growth in the years to come.

From AR FY2018

Themis seem to dominate the overall management and that could be a concern given that they themselves have a chequered track-record.

Investor friendliness may also be an issue due to promoter domination but that may improve(?) as company scales operations. Currently they do not have even latest reports on the company website.

AR 2019 mentions full capacity use, but does not disclose any investments in growth, so current spurt in revenues and huge jump in margins is a mystery.

Financials:

Zero debt with high ROCE of 45% and first dividend announced in latest quarter.

Note: Starting this thread as the previous thread is locked and the mods do not want to open it.

About the company:

“KEI Industries Limited is amongst India’s top three wire and cable manufacturers, with a comprehensive product portfolio ranging from housing wires to Extra High Voltage (EHV) cables. Leveraging our in-house cable production, we have strategically forward integrated into Engineering, Procurement and Construction (EPC) services for power and transmission projects. Our high-quality solutions have made us a trusted and preferred provider in the Retail, Institutional and Export segments.” - 2019 Annual report

Segmental Revenue & profit mix:

70% from cables, 25% from EPC and 5% from wires

54% sales comes from institutional, 33% from retail and 13% from exports

Firm has a long history. Looks like it has been a public company from 1992.

Manufacturing at 5 locations.

Bhiwadi (Rajasthan), Chopanki

(Rajasthan), Pathredi (Rajasthan),

Silvassa and Chinchpada (Dadra

& Nagar Haveli).

Retail segment - Has > 1.4k dealers pan India and focus is on expanding this and improve the brand also.

Institutional segment is dependent on government investment

Key exports market for the company are Australia, Middle East and through EPC contractors to Africa and LatAm.

They are currently running at low utilization as they have expanded capacities planning for future growth… Over the next few years, margins should increase further ideally as utilization improves. They have postponed expansion plans as of now

Raw material - Material costs are key here and form over 70% of costs… Decrease in copper, Al prices is a positive for them

Decline in RM prices and maybe govt investment in infrastructure could be tailwinds

Considering housing cables growth and growth in Power transmission etc in the coming years, the space is big and this company seems to be growing a lot…

Discl:

Researching still. Don’t have a position. Not planning to buy till the market dips a little due to one or the other bad news (which imo should happen considering covid, india-china, results announcements etc)

Prataap Snacks is one of the top players in the Indian snack food companies in terms of revenue and amongst the fastest growing company in the organised snack market. The company sells its product under the brand name “Yellow Diamond” with diversified product portfolio including traditional and western snacks.

Company products has 4 basket of products, Extruded Snacks, Potato Chips, Namkeen and Sweets. Its product portfolio consists of Extruded Snacks including Puffs, Rings and Pellets products, Chips including fried, sliced chips / crisps, and Namkeen including moong dal, masala or fried nuts, sev and bhujia. Sweets including cup cakes.

In a short time span of 12-13 years the company features amongst the top 5 organised players, and has witnessed its market share catapulting 4x from less than 1% in 2010 to 4% plus in 2018 (Market leader with 100+ years in market - Haldiram has a 20% market share). This is commendable as many of its peers, despite being in the business for over 20-30 years, have failed to transcend regional boundaries.

They were the first company in India that was offering different grammage (grams per packet) in different areas. They were offering a 16-gram Rs 5 pack in Delhi, but a 13-gram pack in Guwahati. When Frito-Lay was offering 22 grams in a Rs 5 pack, Prataap Snacks offered 30 grams for the same amount (offering superior value proposition for price conscious middle-class Indian consumers), which has helped the company to make a mark in this high intensely competitive space. Its pricing strategy pushed several bigger companies to also offer value packs in an effort to stay ahead in the market.

Prataap has a pan-India distribution reach via: (a) three-tier distribution structure of stockists, distributors & retailers. Prataap’s products reach 17 lakh retail touch points (almost 60% of PepsiCo’s and 35% of Britannia’s reach) served by 13 manufacturing plants with a combination of owned as well as outsourcing facilities.

Their revenue share from different regions, East with 34%, west with 30%, north with 25%, south with 11%.

In the last 3 years sales has grown at 15% CAGR.

Future Growth Drivers::

Avadh’s acquisition gives entry in large and fast growing Gujarat market.

Avadh is the fourth-largest player in Gujarat, which is highly regional and with no presence of any national player. On the opportunity dynamics front, Gujarat is home to 4% of India’s population, but consumes ~13% of packaged snacks. We believe, this acquisition is a great fit for Prataap, providing breakthrough in this market.

Avadh has a portfolio of , pellets (fryums) and namkeens which complements the overall portfolio of Prataap.Avadh posted a turnover of around INR 140 crore in FY18, with operating profit stood at roughly ₹ 11 crore.

80% stake in Avadh ws bought for ₹ 148 crore in Aug 2018, remaining 20% stake will be taken after 4 years.Before acquisition, Prataap has no presence in Gujarat,Rajasthan, Maharashtra (big markets for salty snacks), so with Avadh acquisiton, it entered those markets.

This year(FY2020) they made more than 200 crores from Avadh.

Outsourced model to drive higher asset turns and boost ROCE

In the snacks business, particularly chips and extruded snacks, it is imperative for manufacturing facilities to be closer to the market. This is largely to ensure freshness, high fill rate and also control freight cost as chips and snacks being light weight, the transportation cost is high. Hence, a successful pan-India player typically needs several small manufacturing facilities.Hence, Prataap is gearing to expand its manufacturing base via the third-party outsourcing model.Currently, the company has around 13 manufacturing facilities spread across India, of which 5 are owned and balance 8 are outsourced. Contract manufacturing constitutes ~10-12% to total revenue, which is likely to increase to 20-25% over the next 3 years.

Along with lower logistics costs, outsourcing results in lower capex, thus leading to an asset-light model. This yields better margins and asset turns, thereby driving higher ROCE.

Contribution of 3P manufacturing facility in sales increased from 11% in FY’19 to 18% in FY’20.

Key Concerns::

Raw material (key raw materials are palm oil and packaging laminate) forms around 67-68% of the total revenue for a value for money snacks player like Prataap foods. Any continuous upmove in the prices of the key raw materials would lead to impact on the Gross as well as EBITDA margin, impacting the profitability.

This year palm oil prices increased to 90RS/kg, it is why it posted very less margins this year.

Highly competitive space.

Management Commentary::

Aiming for 2000 crores in 3 years. 9 Percent margin in 4 quarters.

Promoters holds 71.5 perc, out of that Sequoia Capital holds close to 48 perc, rest 23 perc is by other promoters.

Malabar fund holds close to 6 perc.

Faering capital holds - 2 perc.

HOW MANY SHARES COMPANY NEED TO ACQUIRE TO REACH 90% THRESHOLD:- 6,60,69,754.

Acquirer History :

Baring PE through its subsidiary, HT Global IT, acquired the stake from Atul Nishar Followed by open public offer at Rs 135/- share in Year 2013. Further stake was acquired in year 2014 at Rs. 195/- share

Reason behind De-listing : HT global IT (promoter) has outstanding Bonds to repay in July 2021, without privatizing it won’t be possible. Financing for privatization will be done through equity infusion by promoter (Baring PE India) in subsidiary HT Gobal IT. Since Hexaware generates free cash it will help promoter to reduce leverage at promoter level.

Risk is that if privatization doesn’t get through the HT Global won’t be able to repay its Bonds in 2021 which HT global won’t like to do. So possibility of delisting is High. The only question is final delisting price.

PS: This is the reason derived from Moody’s and Fitch’s credit reports of HT Global IT and is different from what they disclosed in offer letter.

Recent deals : The promoters sold 7.8% stake of the company at Rs 447.50 in August 2018. The price is 40% above the current market price.

Is Risk reward favorable if delisting get through:

Potential loss if the delisting get through: 10%

Potential gain : looking at the history of successful delisting in India successful bids have generally been higher by 40% to 50% of offer price.

What if the delisting becomes unsuccessful:

The Company is growing sales and profit @ 17-20% since last 10 years consistently.

Net Debt free company.

Generating free cash flows every year since last ten years consistently.

Dividend payout @ 3.5%.

The company is ninth largest IT Company in India. However there is Client and geographical concentration risk. 45 % of the revenue come from top 10 clients. Major Partner includes Microsoft.

The Demand for IT and automation and clouding is at inflection point after COVID-19

Time limit for Investment:

Other things remaining same it takes 3-4 months to get delisting completed.

Conclusion:

The deal is a win win situation for Investors irrespective of Delisting proposal. At least deserve some allocation. @ayushmit

ICICI Lombard is one of the largest general insurance company in India based on Gross Direct Premium Income in FY19. It was founded as a JV between ICICI Bank and Fairfax Financial Holdings in 2000.

For fiscal 2019, ICICI Lombard issued 26.5 million (on GDPI basis) policies, translating into a market share of 8.5% among all non-life insurers in India and 15.6% among private-sector non-life insurers in India.

Key distribution channels are direct sales, individual agents, corporate agents - banks, other corporate agents, MISPs, brokers and digital, through which they service their individual, corporate and government customers.

The company offers a comprehensive and well diversified range of products, including motor (50% of total mix), health, travel & personal accident (25%), fire (12%), marine (3%) and others, through multiple distribution channels. All figures as of 9M 2020 (please see figure below).

Business Model:

Typically how general insurance companies work >> They have short tail i.e. short duration of policies unlike life insurance (where you have term insurance policies even more than 10-15 years). General insurance policies on the other hand are on an average of 1-2 years.

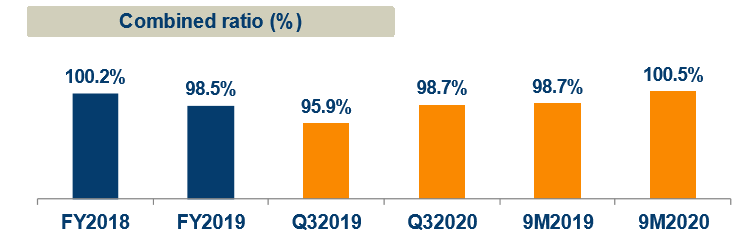

Key metric to track is (a) Combined Ratio (b) Investment Yield

Combined Ratio = Expense Ratio + Loss Ratio

where, expense ratio gives operating expenses as a % of earned premiums

and, Loss ratio gives claims expenses as % of earned premiums

On the top of this insurance company keeps these funds into short term investments, mainly debt securities (typically matching their liabilities). Any money earned on this is an additional income. So, as far as company can operate below combined ratio of 100% they can enjoy this additional income and price their premiums attractively.

Since last few years they have been easily able to maintain combined ratio below 100%. There was spike in between as they incurred heavy losses in crop insurance (and now if you see product mix in 1st figure, they have significantly reduced exposure to crop insurance).

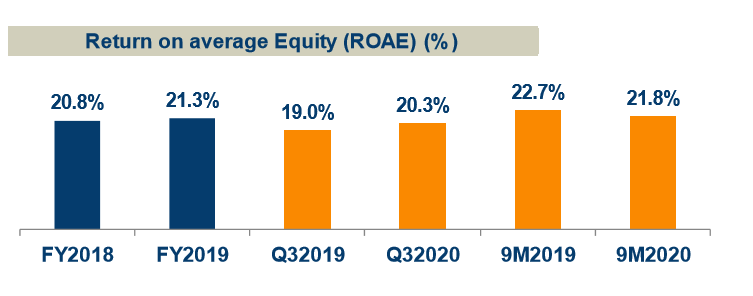

If you multiple realised return with leverage figures, you will get pretty close to RoE figures. So, typically higher interest rate environment without much changes in rates is favourable for higher investment return,(you can say in that sense we are around bottom of cycle).

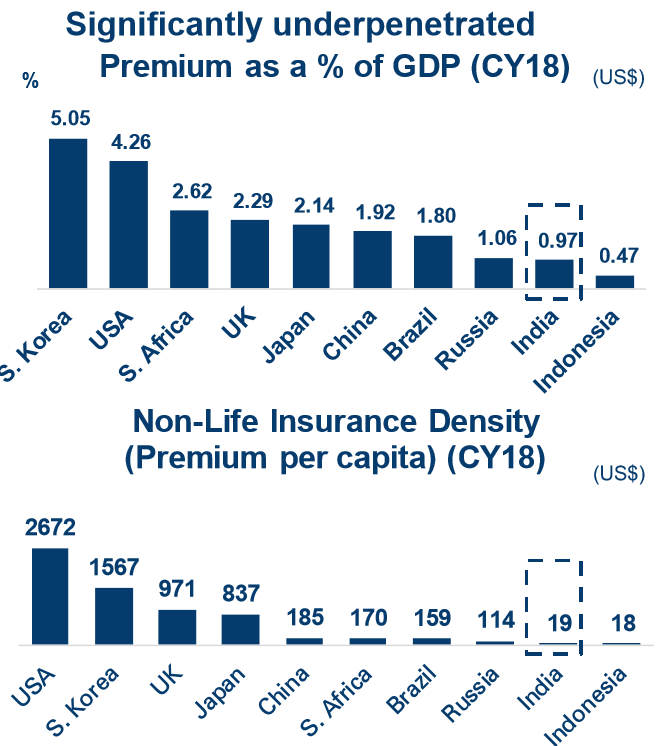

Investment Rationale: Long runway - Some of the products like motor insurance is now compulsory by law. Increased awareness + triggers on corporate travel as well as rail insurance are helping the industry. The penetration levels of general insurance are still very low compared to matured markets.

Source: Investor Presentation Brand Name - ICICI is a strong brand name in India and it will help the company grow its business and give more bargaining power with distributors

**Distribution network:**Over the years, ICICI Lombard has grown its multi-channel distribution, including strong digital presence as well as penetration to Tier 3 and Tier 4 towns. Over the years, if digital and direct policies increases, it will boost their profitability and/or increase pricing competitiveness due to lowering of expense ratio. Better understanding of Indian demographics - One needs good understanding of customer base and deep underwriting capabilities. ICICI Lombard has both due to it’s Indian partner + underwriting expertise from world class insurance partner. Diverse customer base: This multi-channel distribution network enables ICICI Lombard to offer its products to a diverse set of customers, including large and mid-sized corporates, small and medium-sized enterprises, central and state governments, and individuals. Over the years, it has moved from a largely corporate focussed business model to a more diversified mix of business. Scarcity Premium - ICCI Lombard is one of the few General insurance companies listed in India. This way it garners scarcity premium

Key Risks

Big catastrophic risk can prove difficult in terms of higher claim outgo. We have seen this playing out almost every year. Underwriting and reinsurance capability is very critical in such cases. Good diversification of portfolio across geographies and product lines also helps in such cases.

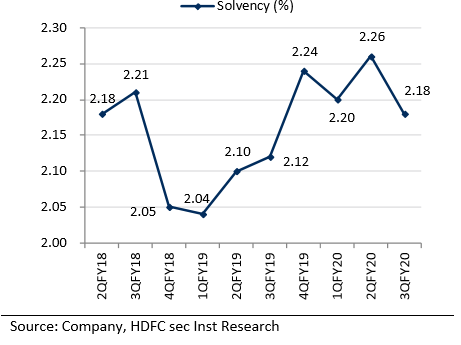

Weakness in solvency ratio or increase in regulatory requirement: This would require further dilution or capital raising. As per current norms, solvency ratios are quite good.

Source: HDFC Research report (link provided in references)

Threat from competition and aggressive pricing: Many single product insurers might have better underwriting capabilities in their product area and could provide better pricing. Also, in highly competitive scenario, premiums can go really competitive and insurers tend to price premiums abnormally low and sacrifice part of their investment income. This can lead to lower RoE and reduced profitability. Also, any regulatory changes that allows life insurance players to come into general insurance can lead to increased competition in future.

Assumptions of underlying reserve requirements: Loss reserves are based on estimates as to future claims liabilities and if they prove inadequate, it could lead to further reserve additions and materially adversely affect the results of operations

Distribution partners: Significant portion of sales is derived from sales to the customers of agents/intermediaries affiliated with motor vehicle manufacturers (“MVMs”) and from channel partners like ICICI Bank. Any material impact in such partnership and significantly reduce competitiveness of ICICI Lombard

Regulatory changes: Any unfavourable regulations around it’s key products can deteriorate its competitiveness

Market and interest rate risks: Investment portfolio and hence premium pricing could be affected in case of adverse market and interest rate movements

Concentration Risks: ICICI Lombard has historically derived and continue to derive a certain portion of its corporate premium from a limited number of large clients. It expects that a certain portion of its corporate premium will continue to be derived from a limited number of clients in the future. If there is any disruption here, it can reduce number of renewals and hence profitability

Disruption from direct players, startups and digital-only players: Business has risk from new players and startups coming into digital-channel and willing to price competitive rates of premium can disrupt the various segments and product lines

Valuation: ICICI Lombard currently trades at ~6x P/B and ~33 PE on trailing basis.

Hello all, this would really be my first post here at VP… would request others to chime in with observations.

Quick summary: This company is growing profits at decent pace of around 15-20% and trading at cheap valuations of about 6.4 times TTM EPS (Market cap. of Rs. 215 cr). Increasing R&D expenses gives some confidence on possibility of venturing in specialized nature of drugs but company has not disclosed anything on that. Balance sheet also looks good with low debt. Some red flags include unrelated investments/loans & advances, promoter compensation and zero dividends. I am not too savvy with the products which they sell but all products look more on the generic side. Exports are ~50% of sales and rising as a % of overall sales.

Final take: Looks decent on fundamentals and attractive on valuations but I am a bit concerned on some of the corporate governance lapses (described below under Red flags). Also, not to sure about their competitive landscape.

Company description

“Bharat Parenterals Ltd. is a Gujarat based pharmaceutical company, established in 1992 by Mr. Ramesh Desai, who started the company with a vision of making world class affordable medicines and to take it to the forefront of contract manufacturing units in Gujarat. Under the chairmanship of Mr. Desai, the company has moved ahead as a research driven and forward looking pharmaceutical company with a dedicated facility for antiretroviral drugs added over time to its already existing facility of general and B-lactum group of drugs. As a fully integrated company we have in-house R&D, business development,manufacturing and regulatory compliance capabilities. Our clients range from small biopharmaceuticals startup to some of the world’s largest pharmaceutical companies.”

Some key highlights

PnL: Profits up CAGR 20% in last 5 years, but no dividends to shareholders. Revenue growth CAGR of 14% in 5 years.

AR 18-19: Management discussion and analysis

“With more than 500 formulations to choose, a strong formulation development base and coveted WHO-cGMP certificate to its credit, Bharat Parenterals Limited has already made an export presence across the globe. The large scale modern production facility at Haripura, Savli is WHO-cGMP certified and abides by its stringent norms. Its processes are ISO 9001:2000 certified as well over years, Bharat Parenterals Limited has sharpened its production expertise, built modern production lines and consolidated manufacturing processes, which conform to international standards.”

“Opportunities and Threats: The Company is looking at different opportunities in untapped markets and also across a value chain. It plans for alliances with business associates in the global market, giving a huge boost to the products that it deals in. We are fully conscious of our responsibility toward our customers. Our efforts are directed toward the fulfillment of customer satisfaction through the quality of products. As the consolidation of this industry gains momentum, the need to develop a dedicated team of skilled manpower assumes urgency and importance. We will continue to focus on training and motivation of manpower so as to develop teams of qualified and skilled personnel to effectively discharge their responsibilities in a number of projects and activities. It is, in this context, which we have been working towards promoting the skills and professionalism of our employees to cope with and focus on the challenges of change and growth.”

“Outlook: The Company is focusing on its core business of manufacturing and marketing of formulations. Research and development has been put on fast track for cost competitiveness and to comply with the regulatory market. Cost rationalization and management control at all levels are practiced to ensure operational efficiency in the sphere of manufacturing and marketing. Armed with strong resources base and a vision to be a leading manufacturer of formulations, the company is poised to unleash its true potentials to meet the challenges and exploit growth opportunities ahead.”

Red Flags

AR 2014-15: Said paid no dividend due to future expansion planning (same language used for all AR’s until 2018-2019)

But no apparent increase in Fixed assets! (Gross block growth is uneven)

Debtors written off in FY18-19

More than 4 fold increase in promoters’ salary and some unusual payments to Shital Shah!

Rain Industries

Procter & Gamble Hygiene

Jubilant Foodworks

PVR

IDFC First Bank

Bharat Rasayan Ltd

HDFC Bank

Bajaj Finserv

Maruti Suzuki

TTK Prestige

Dixon Tech

Reliance Industries

V Mart Retail Ltd

Deepak Nitrite Ltd

Dabur India

Affle India

Atul

Alkyl Amines Chemicals Ltd

Hawkins Cookers

GMM Pfaudler

Garware Wall Ropes Ltd

Sunteck Realty

Tata Motors

DCB Bank Ltd

Dr. Reddy’s Labs

MAS Financial

and many more…

I agree to the fact that, most of my picks are based on past performance and a dip in stock price opportunity.

I will surely welcome your suggestions as i like to learn more. please advice.

There is a small company called Crane Infra from Guntur, Andhra Pradesh where the new capital city of AP- Amaravati is being built. The promoter is the son of the uneducated 1st gen entrepreneur Mr. Grandhi Subba Rao.

Mr. Grandhi Subba Rao is the founder of the Crane Betel Nut Power Works Limited

He pioneered the use of imported “From Fill Seal Machines” for Betel Nut Powder Packing

He is a well-known industry veteran with a dedication to maintainaining stringent quality standards?

Mr. Subba Rao is currently heading the Crane Group within various industry verticles including manufacturing,

IT Development, Pharmaceutical Lab, Finance & Investment and Food Processing.

There is very less public info about the projects, investors, etc… It is closely held by family and extended family, I assume it makes projects in Real estate, buildings, roads and plots. Thats is the nature of the business in AP. Please add value and inputs if anyone is from Telnali, Guntur, Vijayawada and nearby

Hi everyone,