Hi Guys ,

At current market price 195, mufti lis trading at a multiple of 16

Credo brands mufti came to ipo on 28th December , with issue price of 280. It was oversubscribed with lot of interest from institutional investors. With market conditions it is beaten down to 200 levels, which makes to think about market behaviour

Even in 9Mfy24, their PAT margins are at 12 % and at cmp 224.5 its trading at a pe of 17.

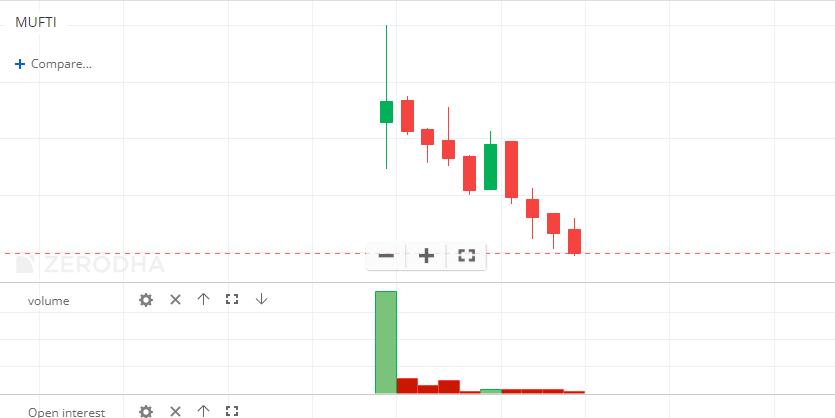

Looking at the chart this looks oversold

The revenue this year , had grown at 19 percent and due to more advertising spend , Pat was down 7 percent.

Fundamentally looking very solid. Also Its peer cantabil retail still quoting at a pe of 31. Company guided for growing at 20 percent yoy . What Am i missing here?

As per management this year expecting revenue of 600 cr and ebitda around 30 percent. Next year growth around 20 percent. They have increased advertising spend in q3 which led to reduction in ebitda

Also since free float is just 15 percent , this took lot of beating . So volatility is expected. No reco, take your call

9 posts - 4 participants