A little bit about the company:

-

Senco gold is largest organized retail jewellery player in the country with a market presence in more than 13 states. They have company owned company operated (coco) stores as well as franchise store model.

-

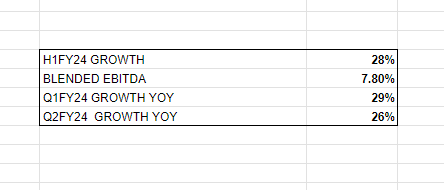

The company has a dominance in the eastern part of India with a volume growth rate of 32% in h1fy24 YoY.

-

Senco has 145 stores which includes 83 coco stores and 62 franchise stores. 57%-43%) .90% of the showrooms are leased.

-

The number grew from 136 stores in fy23. so, a 6.6% growth in 2 quarters as far as store opening is concerned.

-

Out of the 62 franchise stores 49 showrooms are in tier 2 cities.

-

The company has allocated different showrooms for different audience.D’signia being the most premium with an average ticket price of Rs**.76,900** and house of Senco and Everlite being the most economical @ Rs. 37,000.

WORKING CAPITAL REQUIREMENTS FOR A STORE:

A store spends on two things while opening a store:

- Inventory : Inventory requires approximately 10-12 cr. capex requires 1-2cr.

- Capex: The company does no capex for any franchises. the franchises themselves have to pay for their inventory and their capex.

STORE’S ECONOMICS

-

The current stores are open in 55:45 ratio between coco and franchise stores. Franchise growth rate is 15% and the contribution stands at 35%.

-

The inventory turnover for a franchise store from 1st year is 2 and reaches 3 by the third year. blended franchise turnover is 2.

-

The company owned stores have a gross margin profile of 18% and in case of franchise stores, the gross margins are anywhere between 10-12%.

-

Senco keeps 6-7% of the margins with them while leaving 11-12% for the franchise stores.

-

that implies = 2*10cr of inventory = 20crs worth of inventory in a year with 12% gm = 2.4crs approximately, when accounting for inventory. the store pays and get the inventory. the company doesn’t show these inventory levels in their books

HEDGING:

• The company is 80% hedged and have hedged it using two instruments:

1.) Gold metal loan: accounts for 50-55% of their hedging positions:

gold metal loans are taken from the bank for their requirement of gold for their inventory. They take an unfixed loan where gold prices are directly related to the amount they pay to the bank.

•Positions on mcx: They hedge the rest of the positions with futures and options. this is a common practice in the industry.

• the crux is that they have no effect scenario as far as price escalation or de escalation is concerned.

SWOT ANALYSIS

I have done a swot analysis keeping in account the various strengths, weaknesses, opportunities and threats I find in the company. This analysis covers most of the aspects of the space that the company is right now in and might be in the coming future.

STRENGTHS:

-

Their reputation, industry expertise and knowledge: second largest retail jeweler in the country, presence in more than 13 states. have company owned stores as well as franchise stores.

-

Dominance in the eastern region: *East has 110 stores, approximately 76% of total stores. with 49 own stores and 61 franchise stores.

-

gold price escalation and de-escalation does not have any effects: because of proper hedging mechanisms in place.

-

Inventory stock turnover: Churning of stock where required gives them an edge in stock turnover ratio : **higher stock turnover gives them better roe

-

Tech savvy: launched a metaverse which allows customers to view and try on all the designs virtually. giving them a sense of the design and look. have a website names ever lite, targeting gen z by offering modern diamond designs.**

WEAKNESSES

- too much dependence on just gold. 90% of the sales are in gold products.*

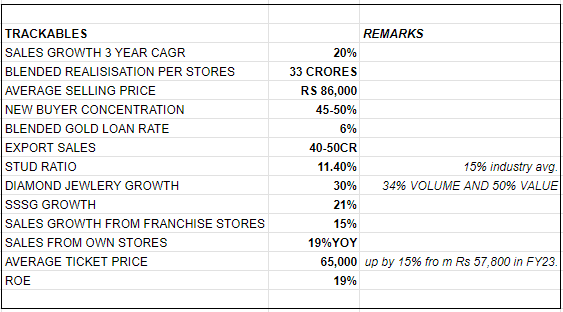

- stud ratio lower than of industry average. 11.8%vs 15%.*

- slight seasonality in sales. h1 is lighter in sales as compared to h2*. The margins also get affected due to this.

- Sectors like exports have negligible margins for them. But with decent growth potential.*

OPPORTUNITIES

-

Male jewelry growing at a 15% rate (gold chains and rings)

-

Replacement market growing because of government policies eg. HUID code : purchase from old jewelry increased to 24% of sales from 19%

-

Sectoral shift from unorganized sector to organized sector: currently stands at 33-38% for organized and 62%-67% for unorganized. expected to reach 42%-47% for organized and 53-58% unorganized by fy26.

-

their average ticket price is rs.65,000, with a revenue of 4,000 cr. number of transactions has been around 5l, this suggests: the light stud jewellery which is sold on their online portals and stores increases the diamond sales. as they grow more in this segment. margins are bound to get better.

-

daily wear jewellery trend. 35-40% people are buying jewellery for them for daily wear purposes.

as their share in diamond jewellery increases which is very insignificant right now profitability increases on an ebitda level and looking at their target audience, their market share is expected to go up. As far as diamond sales are concerned they have doubled their sales in diamond in the last 4 years.*

THREATS

-

Heists: Two stores in the same region were looted, insured but insure repayment takes time.

-

Regulatory developments: Any potential regulatory developments can hinder with the short term , medium term growth eg, Deomotization.

-

Lab made jewelry: has a major effect on diamonds, especially the large studded ones. effect has not yet been seen on the smaller sizes yet.

-

Potential strikes from karigars: Company is heavily dependent on karigars from east.

GUIDANCE AND OBJECTIVES:

-

Better reach in north. to improve on stud ratio: some stores in the north particularly delhi ncr has a stud ratio of 20%*

-

Guidance is to add 20-25 stores every year till FY26: blended realization per store is around 33crs.

-

open coco stores in metro cities for higher diamond sales and better realization.

-

plan of action is to use hub and spoke model and penetrated deeper into tier 2 and tier 3 cities.*Targeting north and east as primarily.

-

maximise inventory turns because better inventory turns, higher roe’s.

-

for fy24 the guidance for the topline growth is at 20%.

Some of the trackables which are important for the industry are as follows:

*This is not a buy or a sell recommendation!

I have created this thread on Senco gold to have better understanding of the company through the wise inventors and learners we have on this forum. Its imperative to keep having discussions on this company through this thread to have a better understanding of how the company performs.

23 posts - 17 participants