Mcap: 396Cr, CMP: 122

FY2023: Revenue - 145Cr, PAT - 2Cr

History

• It operated close to 130 screens mostly in Western India. In 2012, Cineline sold their entire operations to PVR for 395Cr, making PVR the largest multiplex player in India. Part of the deal also included a lease agreement for 23 screens for a period of 10 years.

• The sale had a non compete clause, barring Cinemax to enter into similar business for 10 years

April 2022

• Term of the non compete clause had come to an end and Cineline decided to venture back into the business of Cinemas. As an initial step, it started with the 23 screens with a seating capacity of around 6000 under the name of MOVIEMAX that was leased out to PVR 10 years back

• It monetised Non core assets for a value of roughly 80Cr including a Eternity Mall in Nagpur (60Cr) and couple of commercial spaces in Mumbai (20Cr)

• It also operates Hyatt Centric Hotel in Candolim, Goa with 160+ rooms contributing to roughly 20-25% of revenues

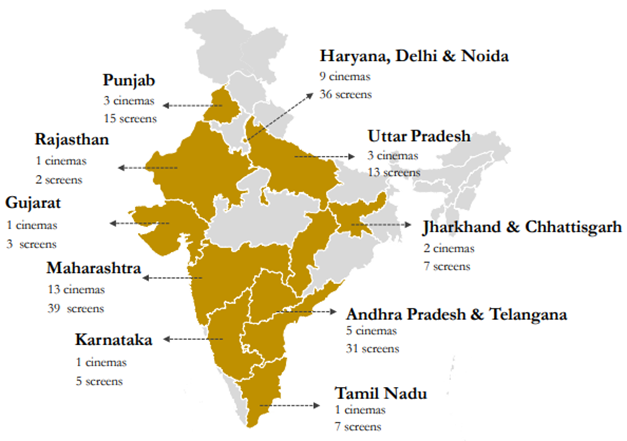

Operations as of date:

• 4th largest cinema chain in India in terms of box office collections

• Operates 39 cinemas (Currently operational: 18 and Under fit out and tied up: 21)

• 158 Screens (Currently operational: 64 and Under fit out and tied up: 94)

• Seating capacity of 36,000+ across 26 cities

Key triggers:

Strong promoter pedigree:

• Mr Rasesh Kanakia was one of the earliest entrants into the multiplex business. Created a brand – Cinemax with 130+ screens

• The promoters are also engaged in the business of real estate having developed commercial and residential projects across Mumbai (LinkLink)

• Promoters have infused money a couple of times since making a re-entry in the film exhibition business. In 2021, did a preferential allotment to promoters at INR 71.5 to raise for further expansion and further issued warrants at INR 130 per share, a part of which recently got converted in October 2023 taking their stake to almost 68%

Expansion plans:

• Managed to open 61 screens and garner 35 lakhs+ admits within an year of coming into business

• Following a low capex expansion plan with acquiring developers’ fully fitted, plug and play screens and entering into a revenue share model for majority of tied up properties

• Undertaken renovation of existing screens

• Roll out plan till March 2025

Debt reduction by way of sale of non core assets:

• Currently has debt of 380Cr+ including lease liabilities of around 110Cr+

• Looking to monetise Hyatt Centric Hotel in Goa with is valued at roughly 300-350Cr

Recent performance (1H FY24)

• Recorded revenue of 104Cr from Cinema business, up 180% from 1HFY23 with total admits for 1HFY24 crossing 35 lakhs+

• Average Ticket Price (ATP) at INR 234, up 38% YoY with Spend Per Head (SPH) at INR 85, up 31% YoY

• Hospitality business also clocked 11Cr+ in revenue with an occupancy rate of 83% for 1HFY24

• Reported operating margin at 30% and turned profitable in Q2 FY24

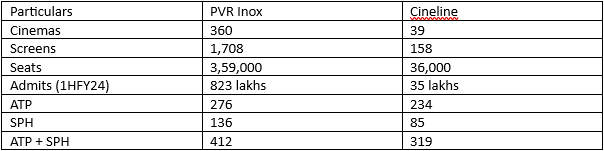

Peer comparison as of 2QFY24

• PVR currently trades at a market cap of 17,000Cr. Cineline currently trades at a market cap of 400Cr

• Cineline being roughly 1/10th in size in terms of no of cinemas, screens and seating capacity would be valued at roughly 1600Cr. Discounting this further for premium ATP+SPH for PVR with a better brand image, the valuation for Cineline should be much more than it is today. Plus when the screens under fit outs come on stream, the revenues could easily double (90+ screens under fit outs) from current levels

Key risk:

High interest cost

• Given the company is in a phase of expansion with around 380Cr of debt (including 110Cr+ of lease liabilities), the interest burden is currently eating up on the margins. Going forward, if the sale of the non core asset (Hotel in Goa) gets delayed, bottomline would be stretched

Disclosure: Invested around levels of 120-122

1 post - 1 participant