Came across a small ~60cr Gujarat-based company in the Gourmet Retail sector. Found the business economics quite interesting so documenting my thesis here.

Disc: This is a purely educational thread trying to document my learnings and insights into the company and is strictly NOT a recommendation in any way. In addition to the business risks, microcaps are also illiquid and volatile. Please do your own due diligence. I have positions in the stocks I discuss.

About the business: Magson is engaged in the retail and Distribution business of gourmet, frozen food, and specialty foods and currently has 26 stores selling 3000+ SKUs across 30,000 sq ft of store space.

Financials

The high gross margins of the gourmet retail segment (~30%) compared to ~15% levels of regular retail, allow for much better business economics. The firm also runs relatively small (1000-1200 sq ft stores extremely efficiently and is able to generate north of ~20K/sq ft operating out of Gujarat - something that even much larger Mumbai-focused gourmet retail chains struggle with ( Nature’s basket is at ~16K/ sq ft) - more on this later. The combination of the good utilization and high gross margins is that the business is able to clock ~7-8% EBITDA margins, which are extremely strong numbers for the retail sector.

Store growth - Management guidance of 10 stores in 18 months, capital and actions indicate more ambitious goals

Currently has 26 stores of which 16 are owned and 7 are franchised. The RHP mentions that they plan to open 10 new stores in the next 18 months, but actual plans could be a bit more ambitious.

The franchise enquiry form on their website indicates there are 15 new cities they plan to expand to.

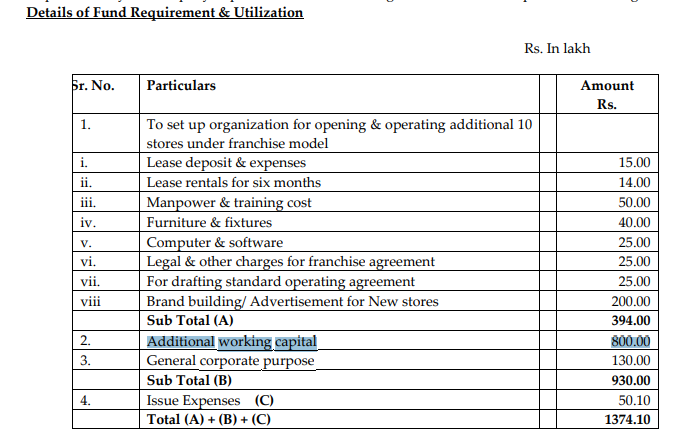

They have also allocated ~8cr from the IPO proceeds for store inventory financing, but an individual stores requires just around 40L of inventory, thereby giving them a longer rope to grow in my view.

The franchise model allows them to grow much faster than they did in initial years, and the business has demonstrated intent to pivot strongly towards the franchise model going forward

(red-own,grey-jv, blue-franchise)

Store economics - ₹20000+ sales/sq ft; ~30% gross margins; 7%+ EBITDA margins; 3x+ Asset turns

Magson runs some of the most profitable retail stores in the country, aided by its best in class gross margins, and strong asset turns. It is interesting to note that the business fares better than busineses of much larger scale operating in strong geographies (Metros). The business has developed a much smaller standard store size (1000-1200 sq ft) vs the ~3000 sq ft of an average Nature’s basket store and appear to be placed somewhere between a 7/11 and a Nature’s basket in terms of store size as they cement their presence in West and Central India.

Franchise economics

-

Legacy franchise model

- Franchisee sets up store as per design provided by Magson

- Magson supplies 80% of the goods to franchise stores, earn distribution margin; 20% procured from local market

- All franchise stores monitored by Magson for QC

-

New franchise model

- Also includes a brand charge as a % of revenue

- At a 2.5cr sales/store, and a 1% charge, and 10 new franchise stores, that’s 0.25cr of straight PBT increment every year

While it remains to be seen if the new franchise partners agree to the proposed brand commission fee, it would be a good source of recurring revenue if implemented.

Even if this inflow from these brand commissions are put into a dedicated

Optionalities

The business also has key optionalities in the form of “RF Gourmet”, which is the firm’s private label brand and “My Chocolate World” which is the firm’s chocolate store piloted in Udaipur. Private labels are a growing theme across Retail stores in India and the world, and aid margins as these products manufactured by a contract manufacturer typically get higher margins. The firm currently has French Fries, Fiery Fries, Chilli Garlic Potato Shots, Delhi Aloo Tikki, Veggie Burger Tikki, Chunky

Fries, Eggs and a range of Chicken Seekh Kababs under the RF Gourmet brand and is venturing into roasted makhana and healthy seeds based on their recent disclosure. Luxury and imported chocolates are also an interesting area of growth in an increasingly affluent India, which offers another (albiet untested) optionality for the business.

The business had also experimented going the B2B route briefly, supplying to DMart and Reliance Retail, but have since discontinued that, likely due to additional working capital stress that doing businesses with such larger players would entail. Given that capital will be a constraint for the business atleast until it gets more broader access to the debt markets, this looks unlikely as an optionality in the short to medium term.

Valuation

The business trades at ~60cr (~24x TTM P/E). Given the quality of the business and the growth prospects ahead, this doesn’t appear too demanding.

That being said, this is an extremely competitive space, and the competitive pressures will be felt more strongly as the business grows into newer markets. Maintaining business discipline (margins, balance sheet discipline, asset turns) as it ventures into the franchise model full throttle and the ability to raise incremental growth capital at fair terms will be key monitorables for me.

Final fun tid-bit

This is not a part of the thesis but just a fun tid-bit! DMart, now one of the largest retail chains in India had opened its first store in Powai, just a few kms away from premier engineering institute in the country - IIT Bombay. Magson had opened its first store in Vastrapur, just a few kms away from one of the premiuer management colleges in the country - IIM Ahmedabad!

Happy weekend, please do share your views on the firm if you’ve gone through it!

I’m active on Twitter and focussed on Indian Equity Investing actively if you would be interested in following - https://twitter.com/bharatbetpf

2 posts - 2 participants